Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider the problem of minimizing a certainty equivalent of the total or discounted cost over a finite and an infinite time horizon which is generated by a Partially Observable Markov Decision P...

This paper studies a one-sector optimal growth model with i.i.d. productivity shocks that are allowed to be unbounded. The utility function is assumed to be non-negative and unbounded from above. Th...

In this paper we consider two-person zero-sum risk-sensitive stochastic dynamic games with Borel state and action spaces and bounded reward. The term risk-sensitive refers to the fact that instead o...

In this paper we consider stopping problems for continuous-time Markov chains under a general risk-sensitive optimization criterion for problems with finite and infinite time horizon. More precisely...

This paper analyzes the stability of optimal policies in the long-run stochastic control framework with an averaged risk-sensitive criterion for discrete-time MDPs on finite state-action space. In p...

The paper provides an overview of the theory and applications of risk-sensitive Markov decision processes. The term 'risk-sensitive' refers here to the use of the Optimized Certainty Equivalent as a...

We consider a finite number of $N$ statistically equal agents, each moving on a finite set of states according to a continuous-time Markov Decision Process (MDP). Transition intensities of the agent...

We consider the strategic interaction of $n$ investors who are able to influence a stock price process and at the same time measure their utilities relative to the other investors. Our main aim is t...

We consider the classical multi-asset Merton investment problem under drift uncertainty, i.e. the asset price dynamics are given by geometric Brownian motions with constant but unknown drift coeffic...

We investigate discrete-time mean-variance portfolio selection problems viewed as a Markov decision process. We transform the problems into a new model with deterministic transition function for whi...

This paper extends the utility maximization literature by combining partial information and (robust) regulatory constraints. Partial information is characterized by the fact that the stock price its...

Within a common arbitrage-free semimartingale financial market we consider the problem of determining all Nash equilibrium investment strategies for $n$ agents who try to maximize the expected utili...

We consider mean-field control problems in discrete time with discounted reward, infinite time horizon and compact state and action space. The existence of optimal policies is shown and the limiting...

Major events like natural catastrophes or the COVID-19 crisis have impact both on the financial market and on claim arrival intensities and claim sizes of insurers. Thus, when optimal investment and...

We study the minimization of a spectral risk measure of the total discounted cost generated by a Markov Decision Process (MDP) over a finite or infinite planning horizon. The MDP is assumed to have ...

In this paper, we study a Markov decision process with a non-linear discount function and with a Borel state space. We define a recursive discounted utility, which resembles non-additive utility fun...

In this paper, we consider risk-sensitive Markov Decision Processes (MDPs) with Borel state and action spaces and unbounded cost under both finite and infinite planning horizons. Our optimality crit...

We consider robust Markov Decision Processes with Borel state and action spaces, unbounded cost and finite time horizon. Our formulation leads to a Stackelberg game against nature. Under integrabili...

In this paper we consider an optimal investment and reinsurance problem with partially unknown model parameters which are allowed to be learned. The model includes multiple business lines and depend...

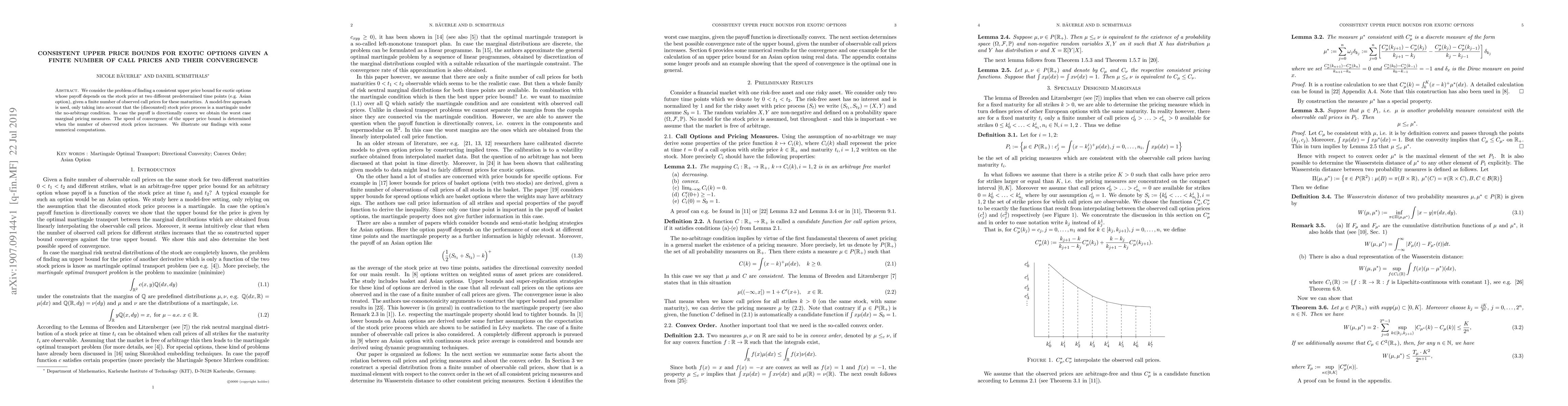

We consider the problem of finding a consistent upper price bound for exotic options whose payoff depends on the stock price at two different predetermined time points (e.g. Asian option), given a f...

We consider statistical Markov Decision Processes where the decision maker is risk averse against model ambiguity. The latter is given by an unknown parameter which influences the transition law and...

We generalize Quasi-Linear Means by restricting to the tail of the risk distribution and show that this can be a useful quantity in risk management since it comprises in its general form the Value a...

We consider the problem of finding consistent upper price bounds and super replication strategies for exotic options, given the observation of call prices in the market. This field of research is ca...

In this paper we consider reinsurance or risk sharing from a macroeconomic point of view. Our aim is to find socially optimal reinsurance treaties. In our setting we assume that there are $n$ insura...

In this paper, we consider $n$ agents who invest in a general financial market that is free of arbitrage and complete. The aim of each investor is to maximize her expected utility while ensuring, with...

We consider non-standard Markov Decision Processes (MDPs) where the target function is not only a simple expectation of the accumulated reward. Instead, we consider rather general functionals of the j...

We study discrete-time Markov Decision Processes (MDPs) on finite state-action spaces and analyze the stability of optimal policies and value functions in the long-run discounted risk-sensitive object...

The goal of this paper is to analyze distributional Markov Decision Processes as a class of control problems in which the objective is to learn policies that steer the distribution of a cumulative rew...

We consider a continuous time investment problem in a multi-asset Black-Scholes market with the following features: The assets' drifts are not known and constitute a source of model ambiguity. However...