Academic Profile

Statistics

Similar Authors

Papers on arXiv

We demonstrate that the problem of amplitude estimation, a core subroutine used in many quantum algorithms, can be mapped directly to a problem in signal processing called direction of arrival (DOA)...

We introduce two quantum algorithms to compute the Value at Risk (VaR) and Conditional Value at Risk (CVaR) of financial derivatives using quantum computers: the first by applying existing ideas fro...

Pricing financial derivatives on quantum computers typically includes quantum arithmetic components which contribute heavily to the quantum resources required by the corresponding circuits. In this ...

We study quantum interior point methods (QIPMs) for second-order cone programming (SOCP), guided by the example use case of portfolio optimization (PO). We provide a complete quantum circuit-level d...

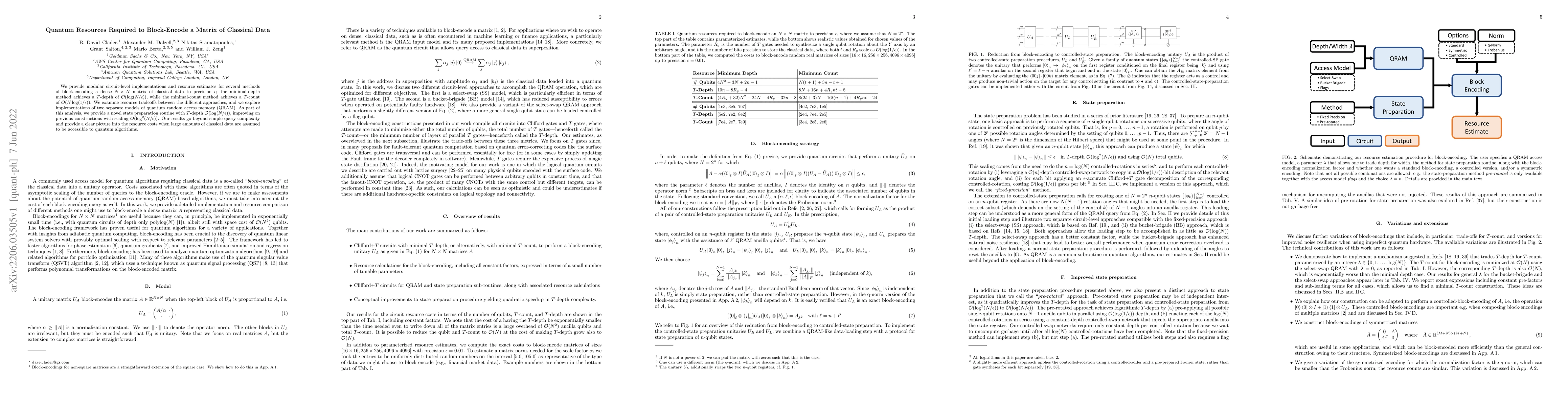

We provide modular circuit-level implementations and resource estimates for several methods of block-encoding a dense $N\times N$ matrix of classical data to precision $\epsilon$; the minimal-depth ...

We introduce a quantum algorithm to compute the market risk of financial derivatives. Previous work has shown that quantum amplitude estimation can accelerate derivative pricing quadratically in the...

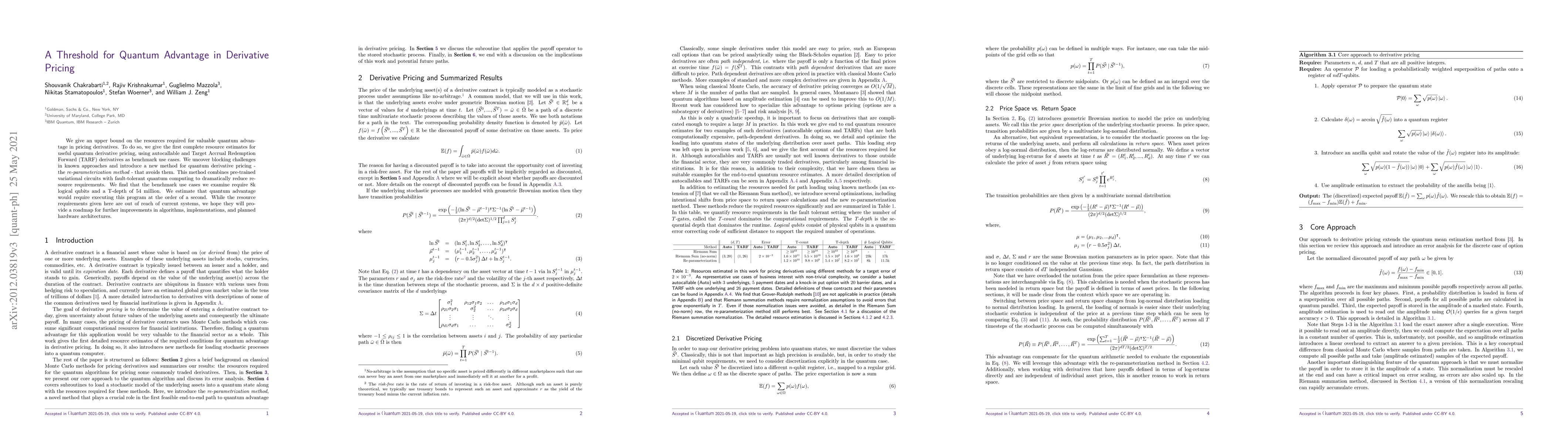

We give an upper bound on the resources required for valuable quantum advantage in pricing derivatives. To do so, we give the first complete resource estimates for useful quantum derivative pricing,...

We present a methodology to price options and portfolios of options on a gate-based quantum computer using amplitude estimation, an algorithm which provides a quadratic speedup compared to classical...

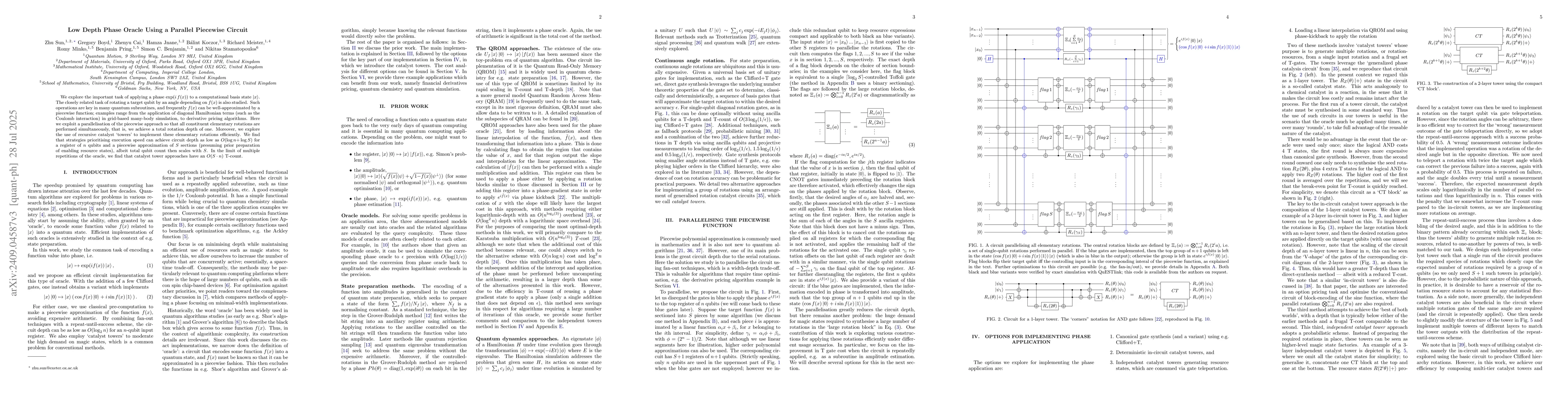

We explore the important task of applying a phase $\exp(i\,f(x))$ to a computational basis state $\left| x \right>$. The closely related task of rotating a target qubit by an angle depending on $f(x)$...