Academic Profile

Statistics

Similar Authors

Papers on arXiv

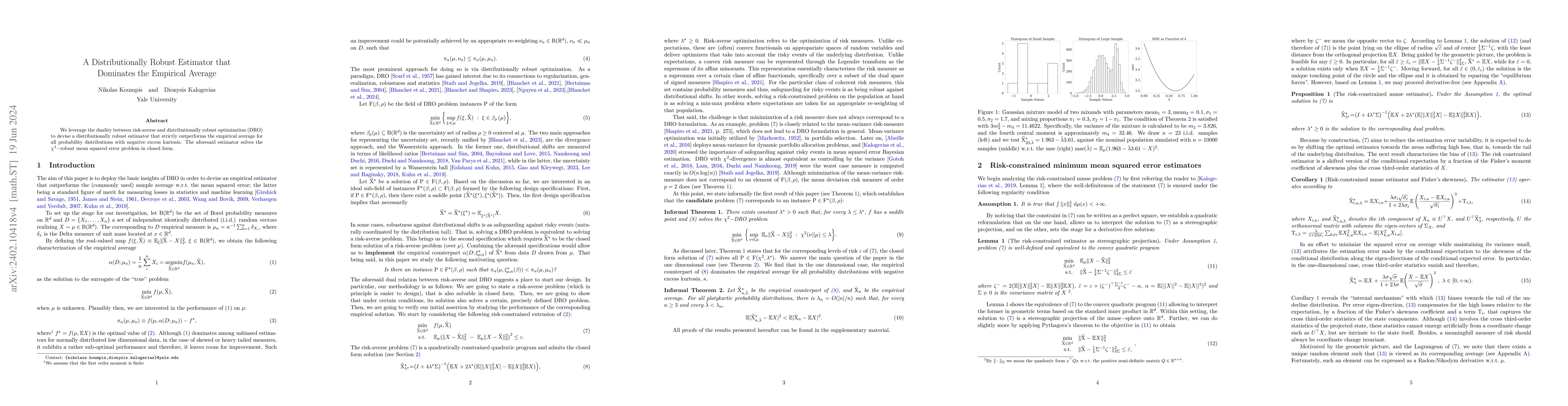

We leverage the duality between risk-averse and distributionally robust optimization (DRO) to devise a distributionally robust estimator that strictly outperforms the empirical average for all proba...

We propose a methodology for performing risk-averse quadratic regulation of partially observed Linear Time-Invariant (LTI) systems disturbed by process and output noise. To compensate against the in...

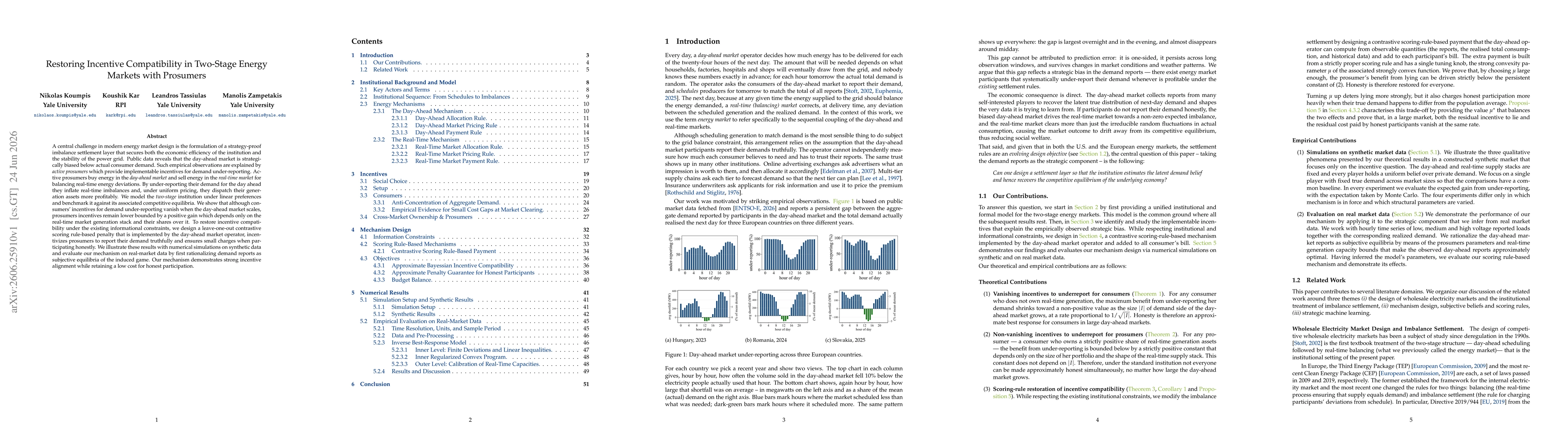

A central challenge in modern energy market design is the formulation of a strategy-proof imbalance settlement layer that secures both the economic efficiency of the institution and the stability of t...