Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper introduces the $\sigma$-Cell, a novel Recurrent Neural Network (RNN) architecture for financial volatility modeling. Bridging traditional econometric approaches like GARCH with deep learn...

Differential equations are a ubiquitous tool to study dynamics, ranging from physical systems to complex systems, where a large number of agents interact through a graph with non-trivial topological...

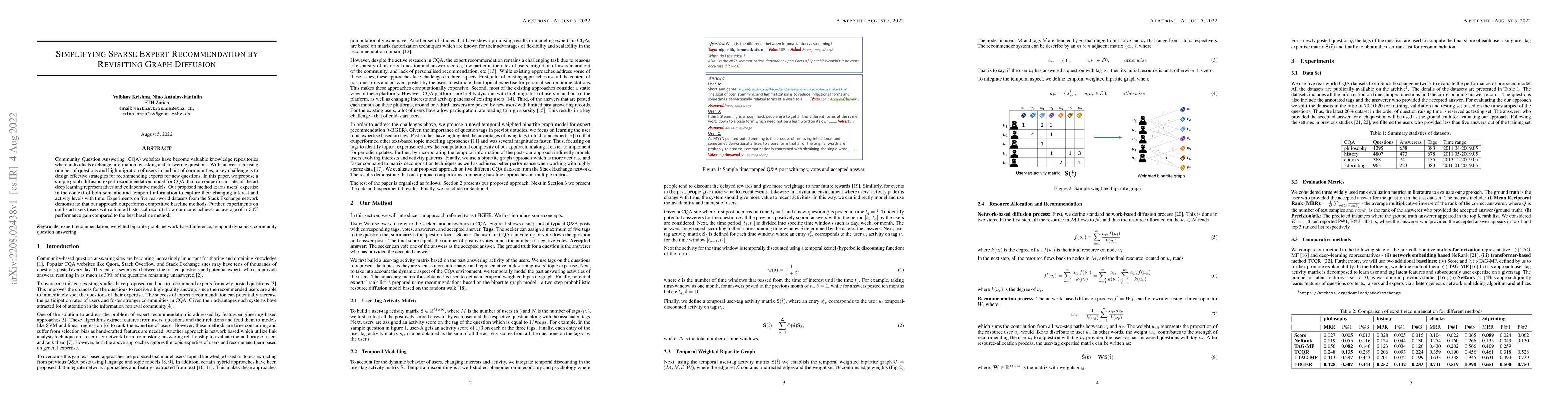

Community Question Answering (CQA) websites have become valuable knowledge repositories where individuals exchange information by asking and answering questions. With an ever-increasing number of qu...

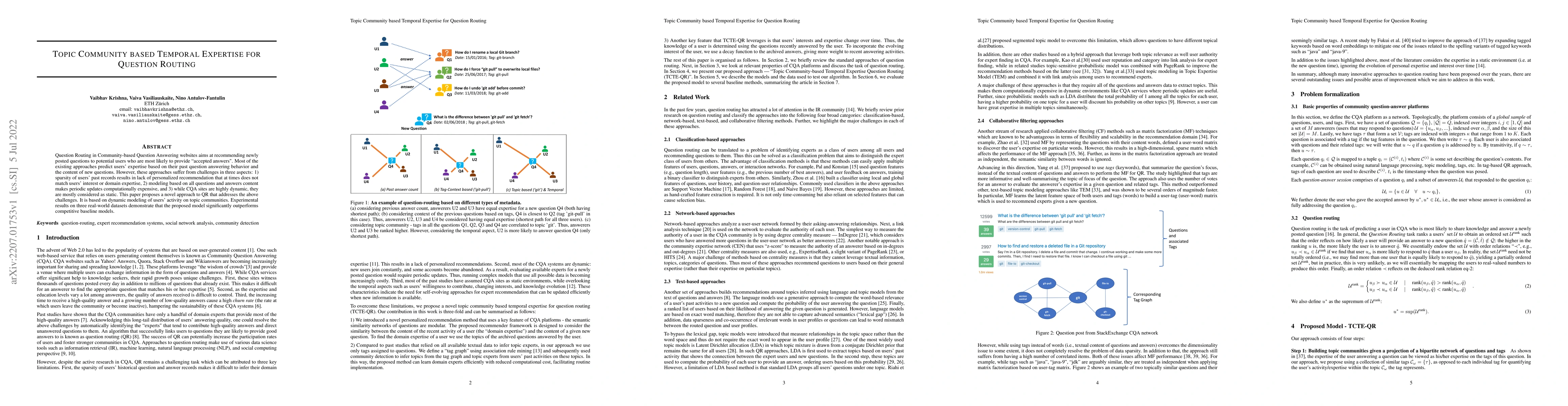

Question Routing in Community-based Question Answering websites aims at recommending newly posted questions to potential users who are most likely to provide "accepted answers". Most of the existing...

Volatility models of price fluctuations are well studied in the econometrics literature, with more than 50 years of theoretical and empirical findings. The recent advancements in neural networks (NN...

Volatility prediction for financial assets is one of the essential questions for understanding financial risks and quadratic price variation. However, although many novel deep learning models were r...

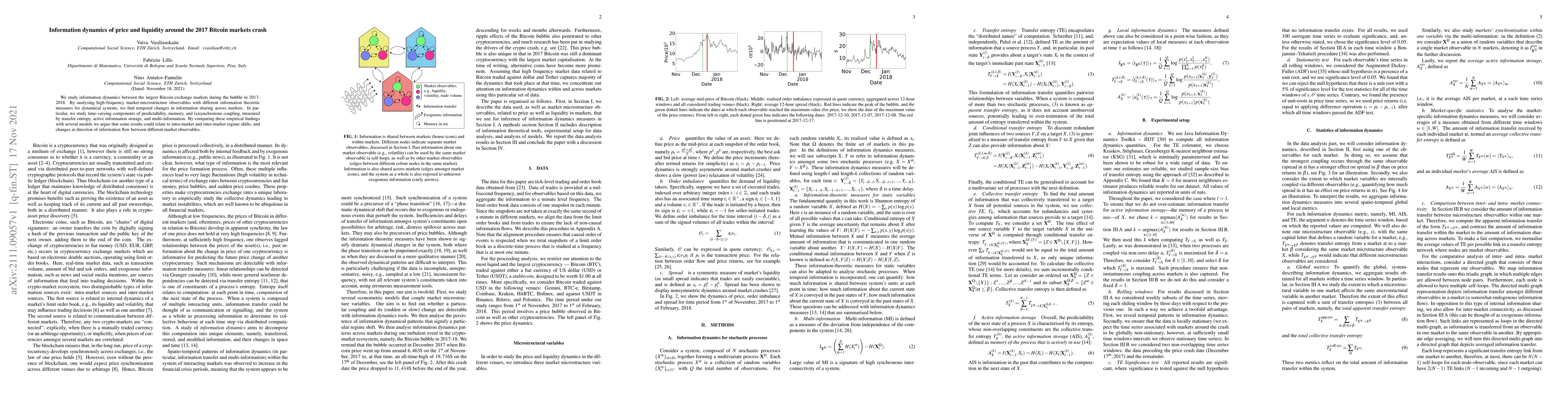

We study the information dynamics between the largest Bitcoin exchange markets during the bubble in 2017-2018. By analysing high-frequency market-microstructure observables with different informatio...

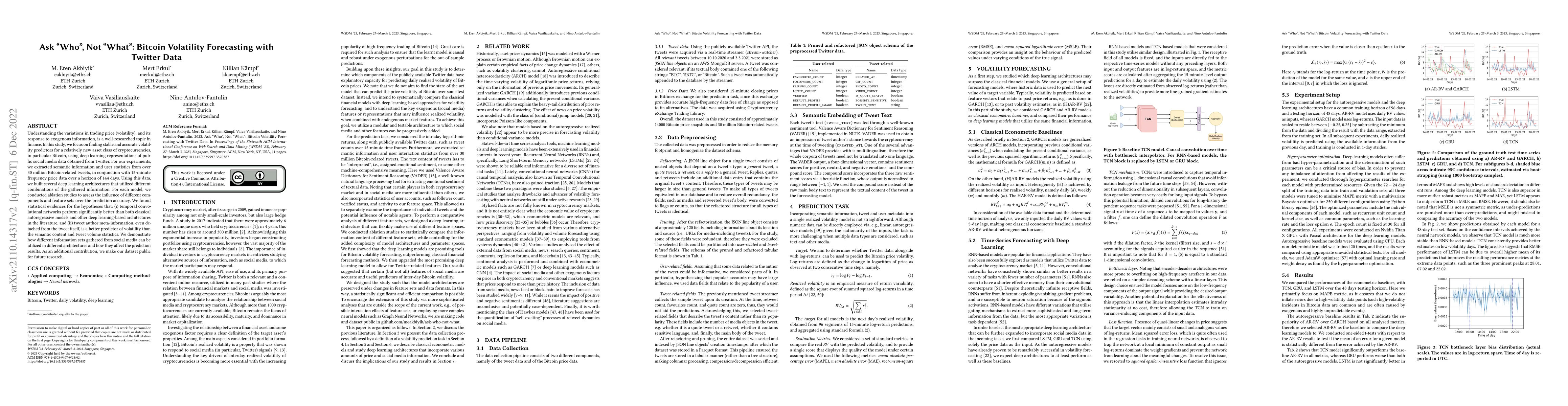

Understanding the variations in trading price (volatility), and its response to exogenous information, is a well-researched topic in finance. In this study, we focus on finding stable and accurate v...

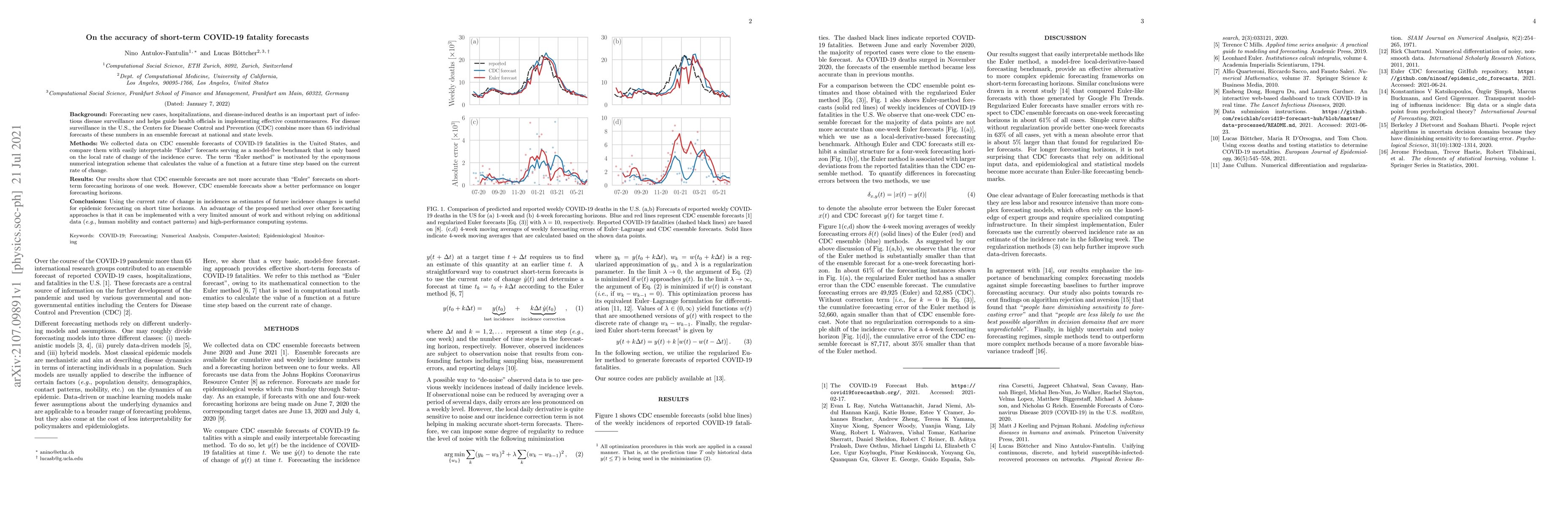

Forecasting new cases, hospitalizations, and disease-induced deaths is an important part of infectious disease surveillance and helps guide health officials in implementing effective countermeasures...

Epidemic models often reflect characteristic features of infectious spreading processes by coupled non-linear differential equations considering different states of health (such as Susceptible, Infe...

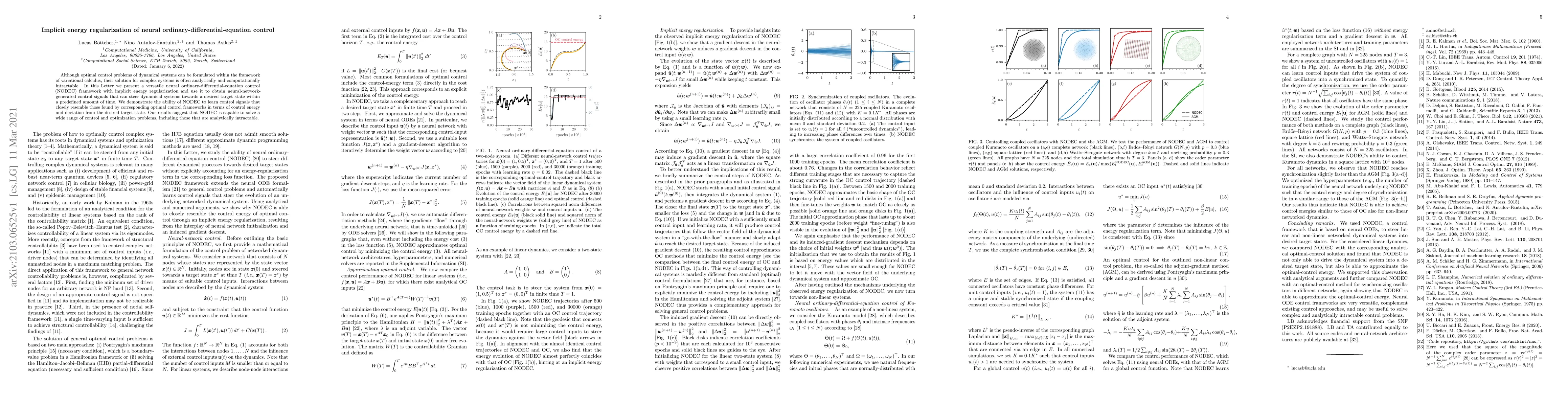

Although optimal control problems of dynamical systems can be formulated within the framework of variational calculus, their solution for complex systems is often analytically and computationally in...

We quantify the propagation and absorption of large-scale publicly available news articles from the World Wide Web to financial markets. To extract publicly available information, we use the news ar...

We study the ability of neural networks to calculate feedback control signals that steer trajectories of continuous time non-linear dynamical systems on graphs, which we represent with neural ordina...

Finding a set of nodes in a network, whose removal fragments the network below some target size at minimal cost is called network dismantling problem and it belongs to the NP-hard computational clas...

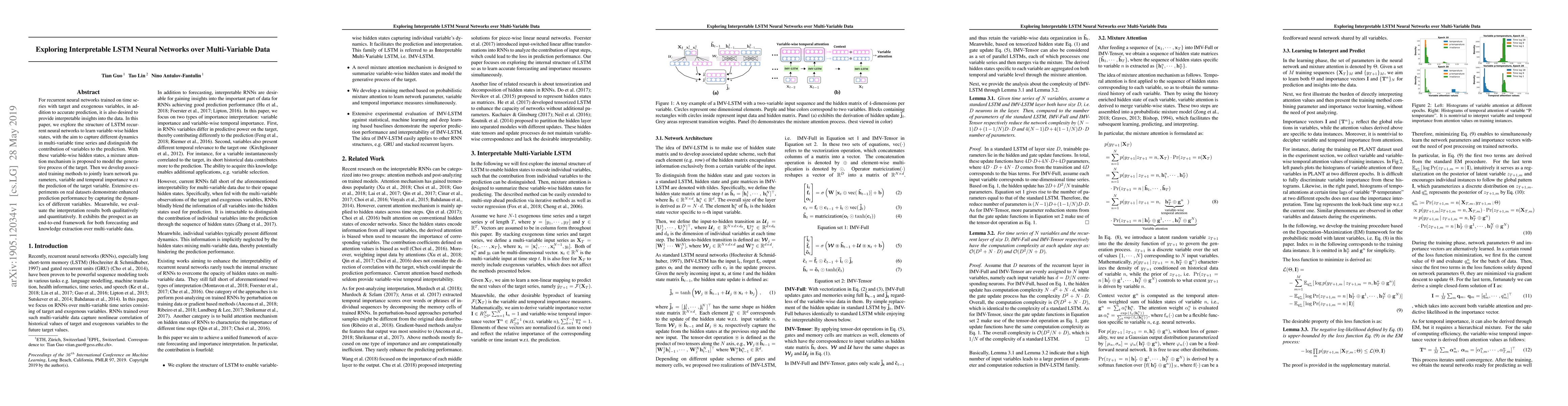

For recurrent neural networks trained on time series with target and exogenous variables, in addition to accurate prediction, it is also desired to provide interpretable insights into the data. In t...

We propose a novel node embedding of directed graphs to statistical manifolds, which is based on a global minimization of pairwise relative entropy and graph geodesics in a non-linear way. Each node...

The ability to track and monitor relevant and important news in real-time is of crucial interest in multiple industrial sectors. In this work, we focus on the set of cryptocurrency news, which recen...

In this article, we present a framework for designing neural networks that remain consistent with the underlying principles of agent-based models. We begin by highlighting the limitations of standard ...

Successful deep neural networks discover salient features of data. We show when and why they fail to learn out-of-distribution (OOD)-relevant representations from an in-distribution (ID) training wind...

This paper examines the impact of market informedness on the profitability of market makers. In contrast to the existing literature, the analysis is conducted in a complex market environment featuring...