Academic Profile

Statistics

Similar Authors

Papers on arXiv

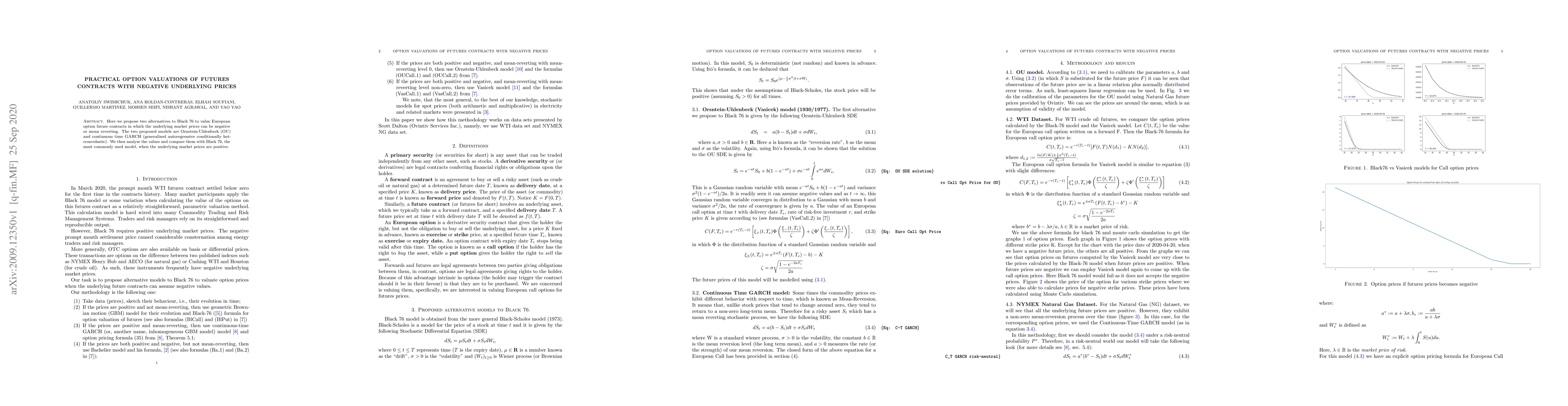

Here we propose two alternatives to Black 76 to value European option future contracts in which the underlying market prices can be negative or mean reverting. The two proposed models are Ornstein-U...

We derive a product formula for the multiple stochastic integrals with respect to Levy process. The idea is to use exponential vectors and the polarization technique which greatly simplify the argum...

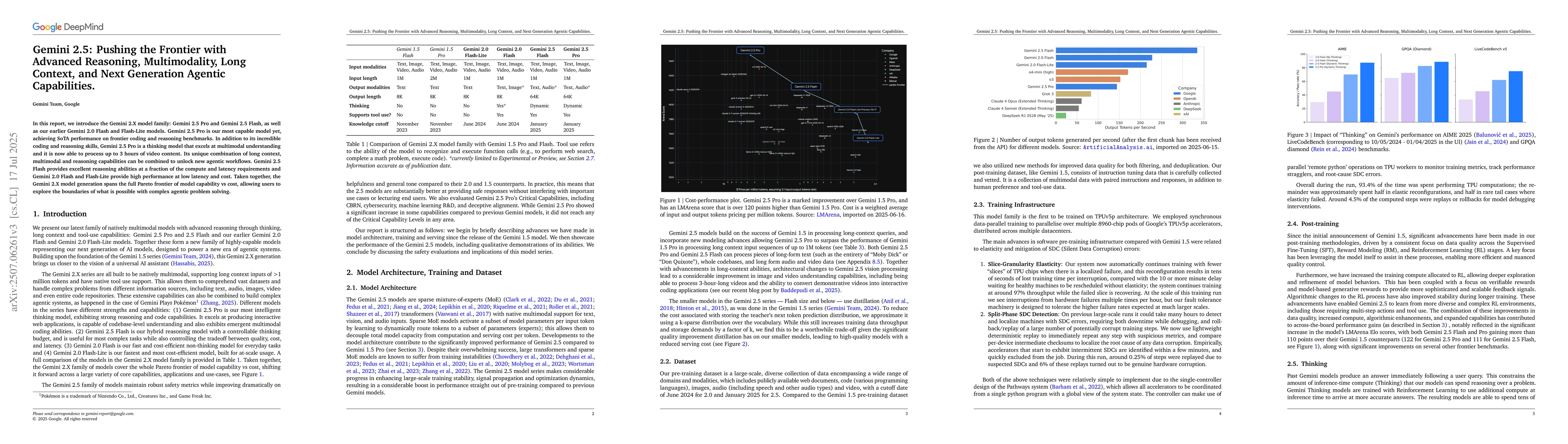

In this report, we introduce the Gemini 2.X model family: Gemini 2.5 Pro and Gemini 2.5 Flash, as well as our earlier Gemini 2.0 Flash and Flash-Lite models. Gemini 2.5 Pro is our most capable model y...

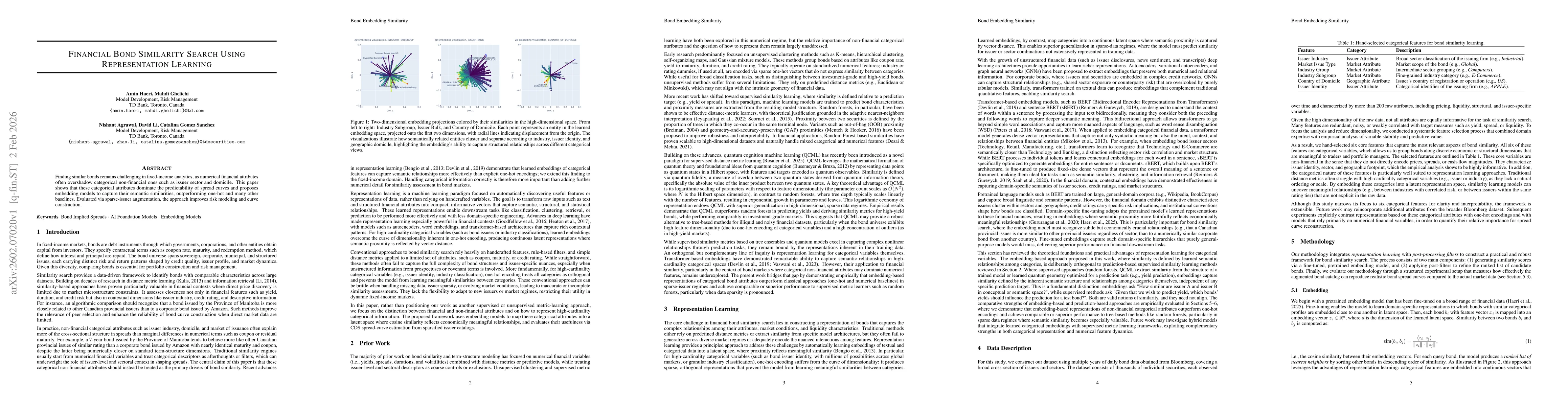

Finding similar bonds remains challenging in fixed-income analytics, as numerical financial attributes often overshadow categorical non-financial ones such as issuer sector and domicile. This paper sh...