Academic Profile

Statistics

Similar Authors

Papers on arXiv

The paper Zhao et al. (2015) shows that mean-CVaR-skewness portfolio optimization problems based on asymetric Laplace (AL) distributions can be transformed into quadratic optimization problems under...

In the papers Carmona and Durrleman [7] and Bjerksund and Stensland [1], closed form approximations for spread call option prices were studied under the log normal models. In this paper, we give an ...

Portfolio selection problems that optimize expected utility are usually difficult to solve. If the number of assets in the portfolio is large, such expected utility maximization problems become even h...

Portfolio optimization in non-stationary markets is challenging due to regime shifts, dynamic correlations, and the limited interpretability of deep reinforcement learning (DRL) policies. We propose a...

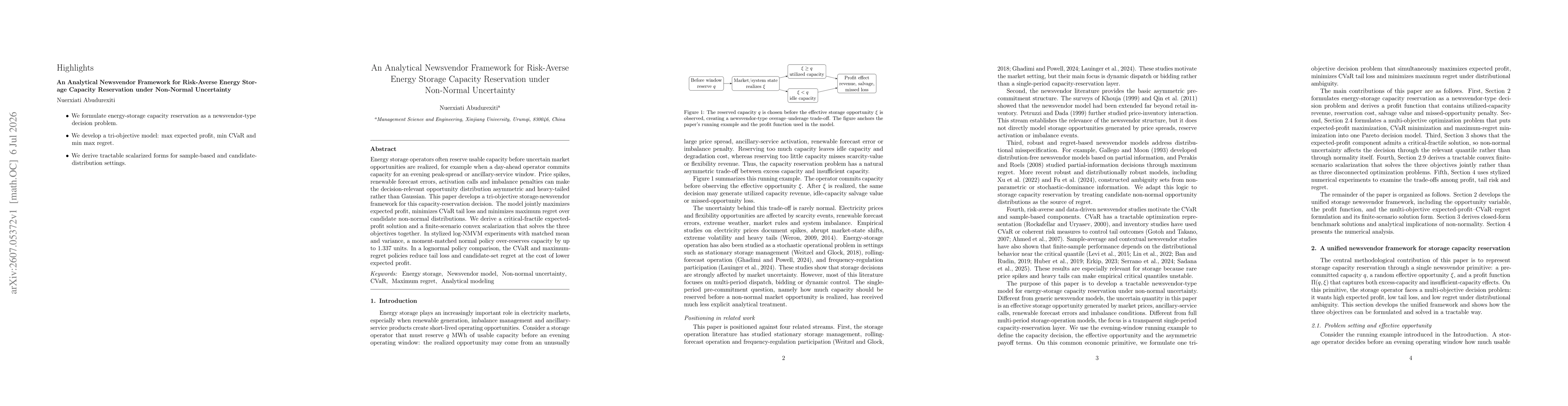

Energy storage operators often reserve usable capacity before uncertain market opportunities are realized, for example when a day-ahead operator commits capacity for an evening peak-spread or ancillar...