Academic Profile

Statistics

Similar Authors

Papers on arXiv

The central idea of the paper is to present a general simple patchwork construction principle for multivariate copulas that create unfavourable VaR (i.e. Value at Risk) scenarios while maintaining g...

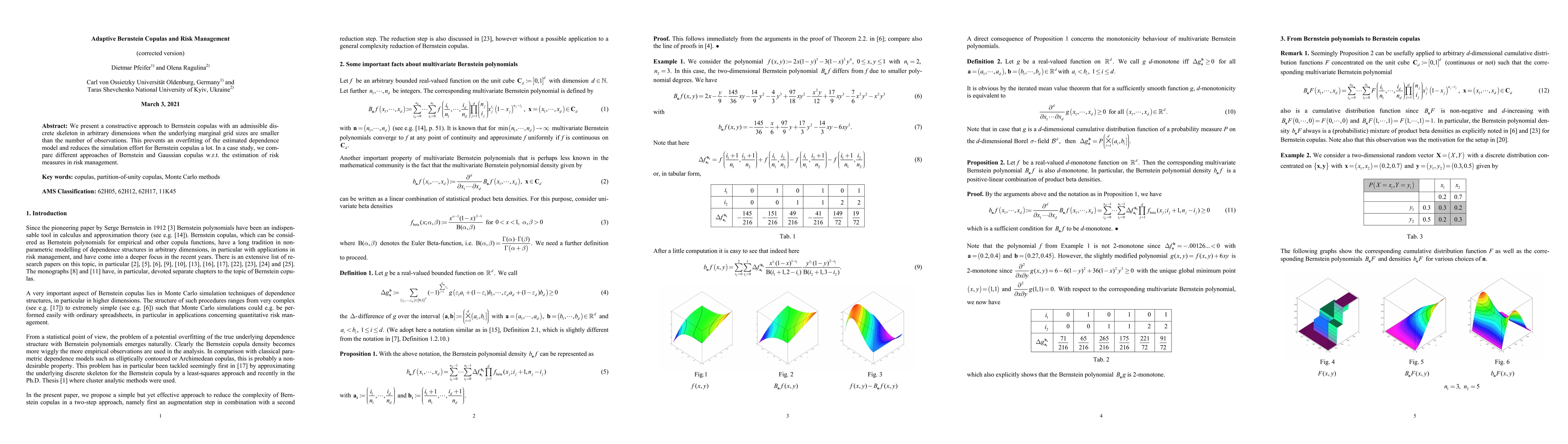

We present a constructive approach to Bernstein copulas with an admissible discrete skeleton in arbitrary dimensions when the underlying marginal grid sizes are smaller than the number of observatio...

The paper deals with a generalization of the risk model with stochastic premiums where dividends are paid according to a multi-layer dividend strategy. First of all, we derive piecewise integro-diff...

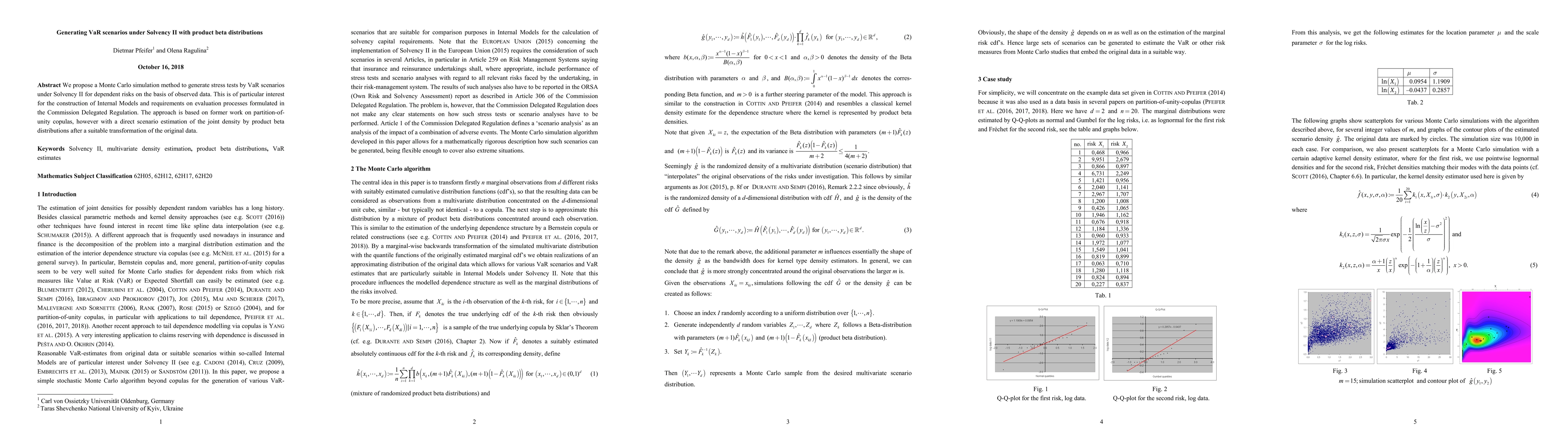

We propose a Monte Carlo simulation method to generate stress tests by VaR scenarios under Solvency II for dependent risks on the basis of observed data. This is of particular interest for the const...