Academic Profile

Statistics

Similar Authors

Papers on arXiv

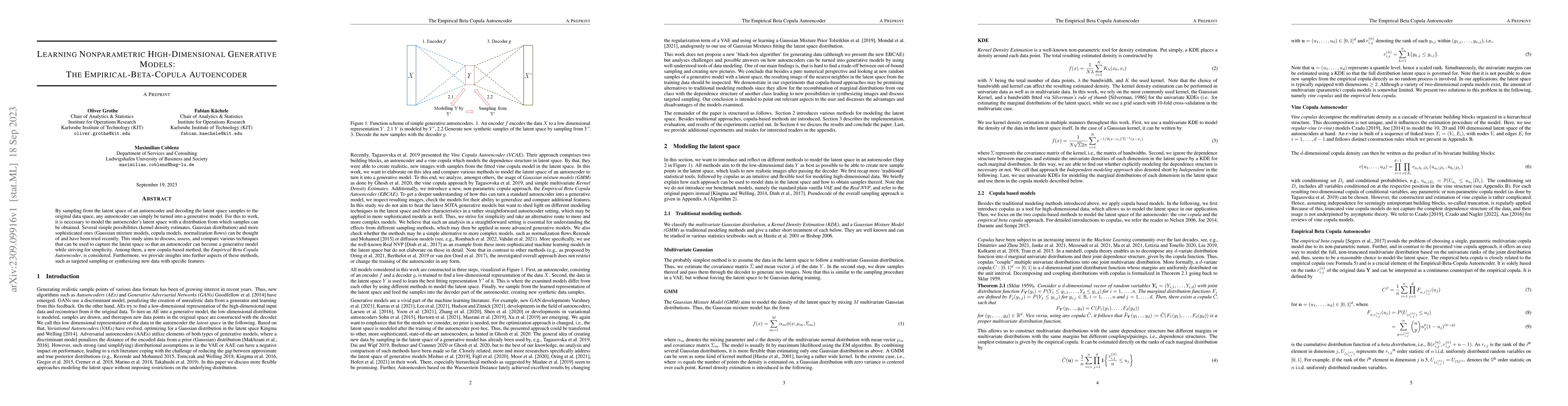

By sampling from the latent space of an autoencoder and decoding the latent space samples to the original data space, any autoencoder can simply be turned into a generative model. For this to work, ...

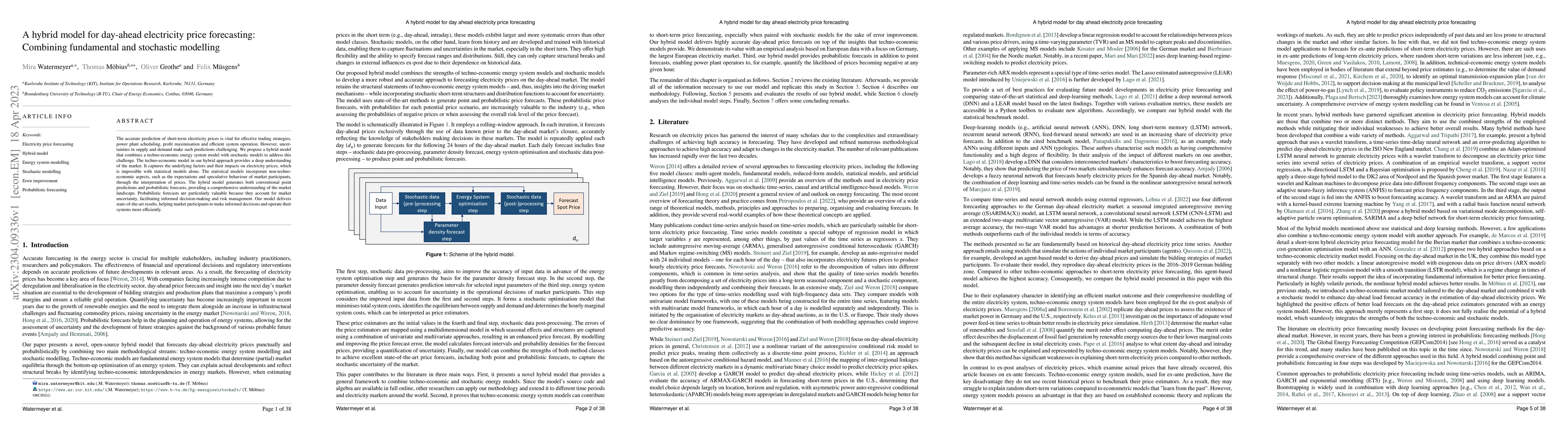

The accurate prediction of short-term electricity prices is vital for effective trading strategies, power plant scheduling, profit maximisation and efficient system operation. However, uncertainties...

Energy system models require a large amount of technical and economic data, the quality of which significantly influences the reliability of the results. Some of the variables on the important data ...

Modeling price risks is crucial for economic decision making in energy markets. Besides the risk of a single price, the dependence structure of multiple prices is often relevant. We therefore propos...

The exponential growth in numbers of parameters of neural networks over the past years has been accompanied by an increase in performance across several fields. However, due to their sheer size, the...

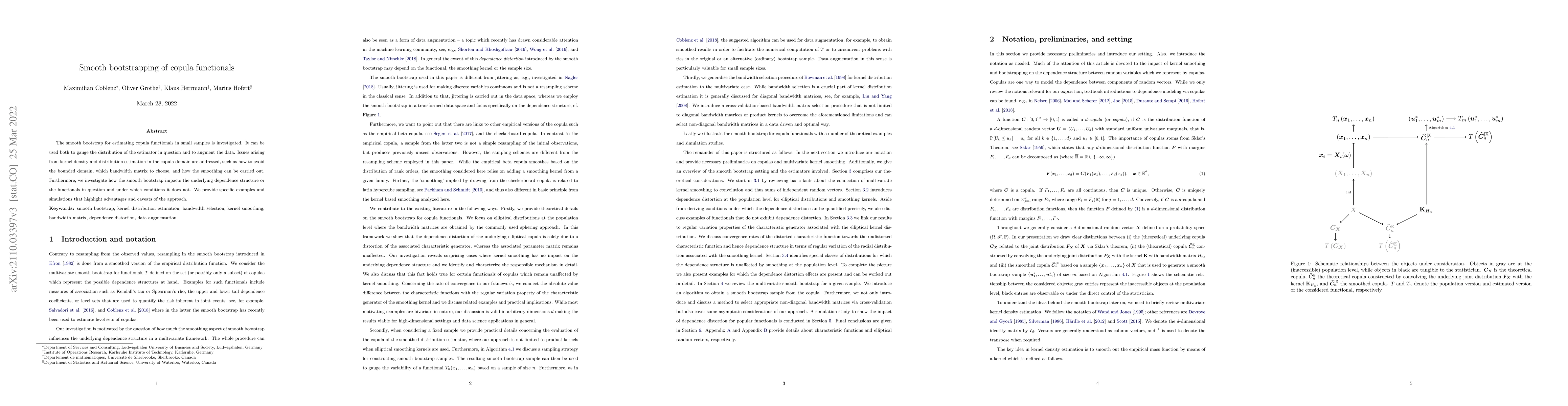

The smooth bootstrap for estimating copula functionals in small samples is investigated. It can be used both to gauge the distribution of the estimator in question and to augment the data. Issues ar...

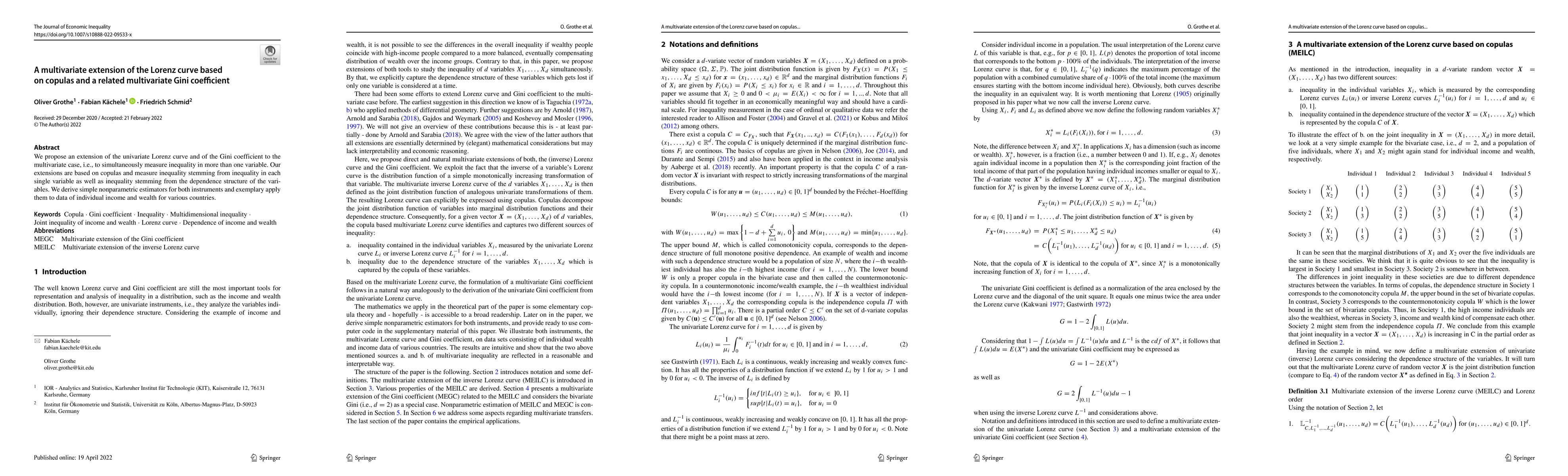

We propose an extension of the univariate Lorenz curve and of the Gini coefficient to the multivariate case, i.e., to simultaneously measure inequality in more than one variable. Our extensions are ...