Academic Profile

Statistics

Similar Authors

Papers on arXiv

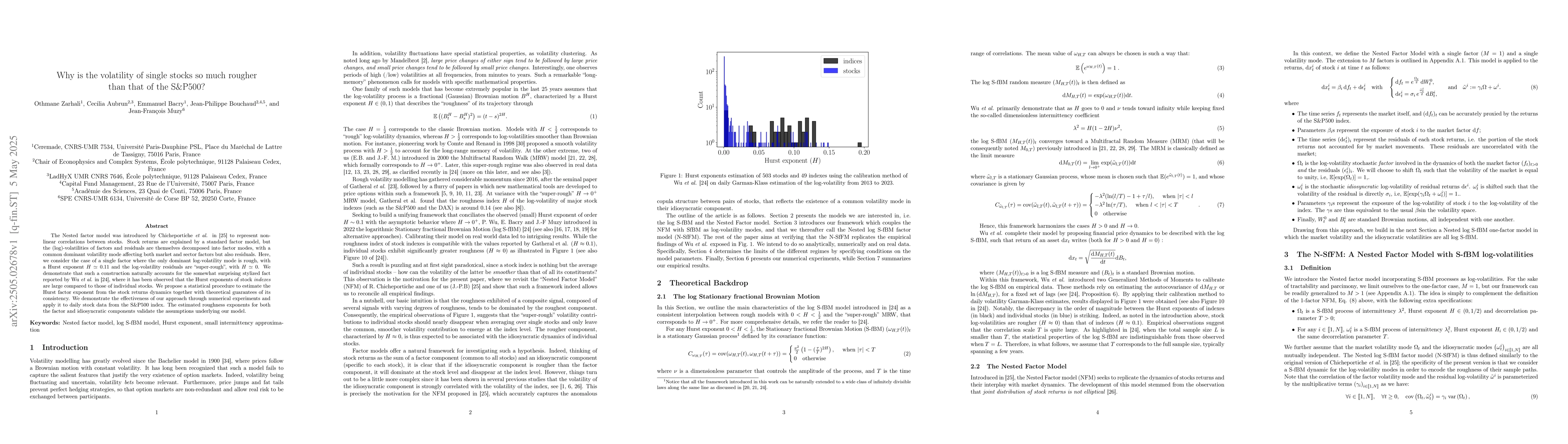

The Nested factor model was introduced by Chicheportiche et al. to represent non-linear correlations between stocks. Stock returns are explained by a standard factor model, but the (log)-volatilities ...

We introduce the multivariate Log S-fBM model (mLog S-fBM), extending the univariate framework proposed by Wu \textit{et al.} to the multidimensional setting. We define the multidimensional Stationary...

A fast simulation framework for stochastic Volterra processes based on Random Fourier Features (RFF) approximation of the kernel is developed. After recalling the main properties of Volterra processes...