Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider estimation and inference in a linear model with endogenous regressors where the parameters of interest change across two samples. If the first-stage is common, we show how to use this in...

We study the effectiveness of subagging, or subsample aggregating, on regression trees, a popular non-parametric method in machine learning. First, we give sufficient conditions for pointwise consis...

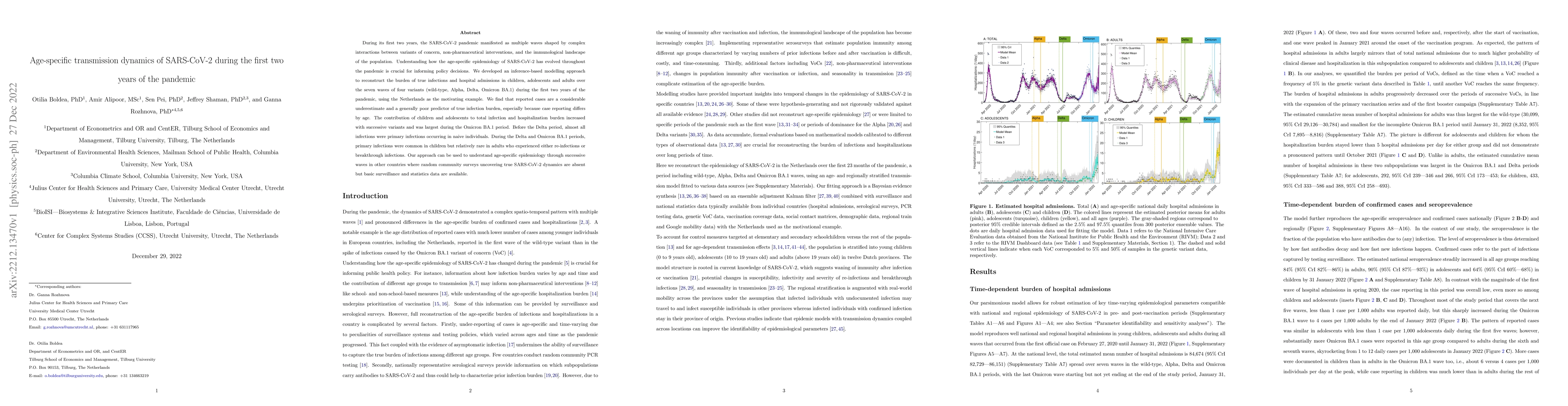

During its first two years, the SARS-CoV-2 pandemic manifested as multiple waves shaped by complex interactions between variants of concern, non-pharmaceutical interventions, and the immunological l...

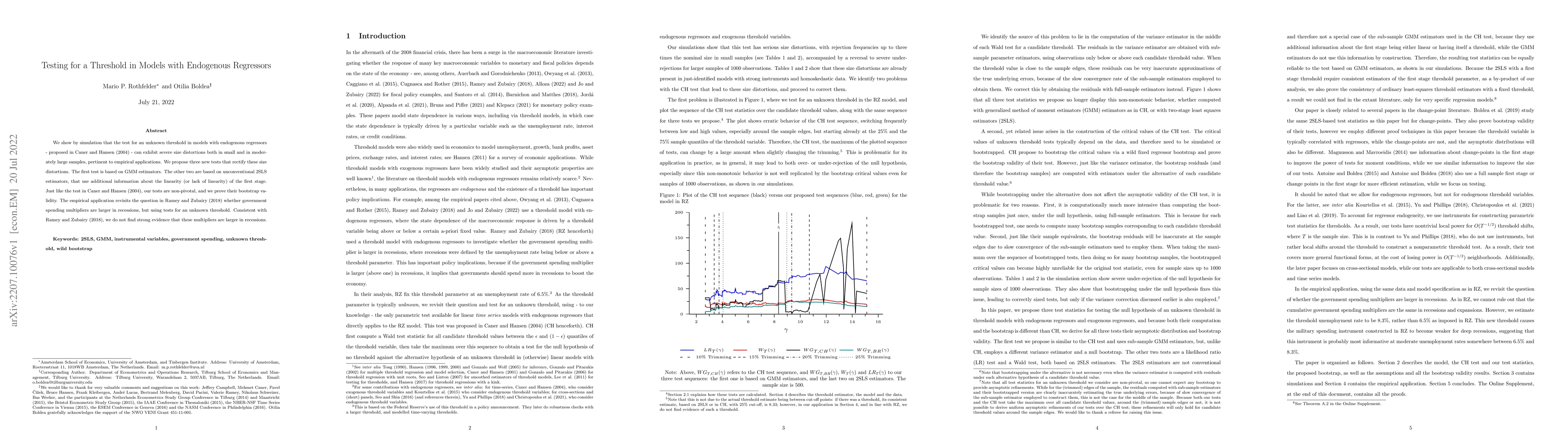

We show by simulation that the test for an unknown threshold in models with endogenous regressors - proposed in Caner and Hansen (2004) - can exhibit severe size distortions both in small and in mod...

This paper analyses the use of bootstrap methods to test for parameter change in linear models estimated via Two Stage Least Squares (2SLS). Two types of test are considered: one where the null hypo...

We review recent developments in detecting and estimating multiple change-points in time series models with exogenous and endogenous regressors, panel data models, and factor models. This review diffe...

This paper studies how insurers can chose which claims to investigate for fraud. Given a prediction model, typically only claims with the highest predicted propability of being fraudulent are investig...

Local projection (LP) and structural vector autoregression (SVAR) are commonly employed to estimate dynamic causal effects of macroeconomic policies at multiple horizons. With enough lags as controls,...