Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study an efficient strategy based on finite elements to value spread options on commodities whose underlying assets follow a dynamic described by a certain class of two-dimensional Levy models by...

The shortcomings of the popular Black-Scholes-Merton (BSM) model have led to models which could more accurately model the behavior of the underlying assets in energy markets, particularly in electri...

The objective of the paper is to price weather contracts using temperature as the underlying process when the later follows a mean-reverting dynamics driven by a time-changed Brownian motion coupled...

In recent years cryptocurrency trading has captured the attention of practitioners and academics. The volume of the exchange with standard currencies has known a dramatic increasing of late. This pa...

In this paper we study the pricing of exchange options when underlying assets have stochastic volatility and stochastic correlation. An approximation using a closed-form approximation based on a Tay...

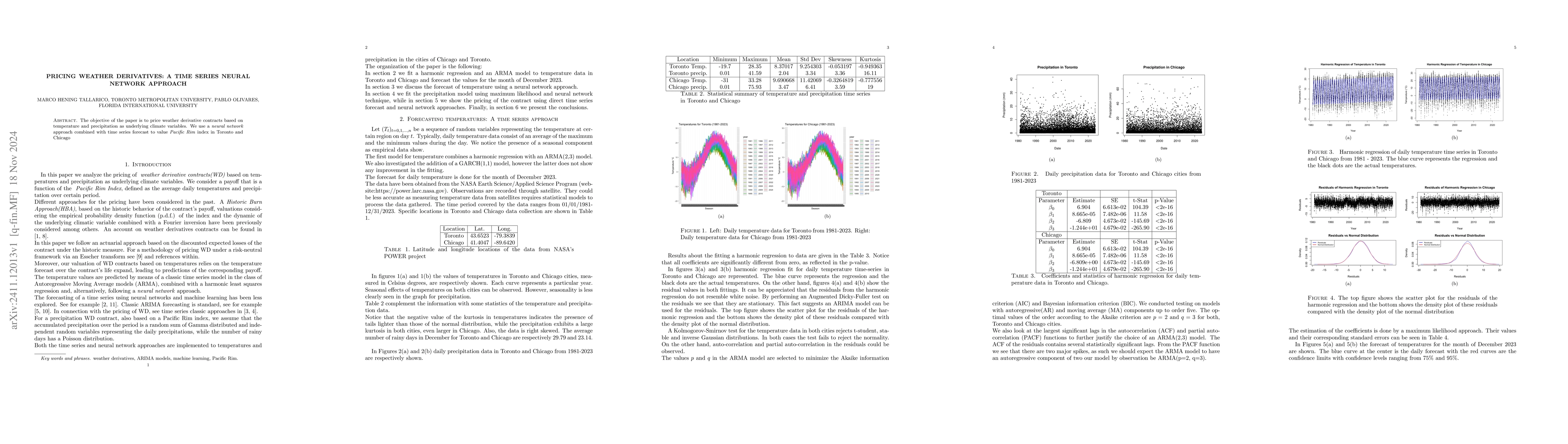

The objective of the paper is to price weather derivative contracts based on temperature and precipitation as underlying climate variables. We use a neural network approach combined with time series f...

In this paper we extend models for the dynamic of the temperatures by considering random switching between Levy noises instead of Brownian motions, with a mean-reverting movement towards a seasonal pe...