Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper proposes a novel approach to hedging portfolios of risky assets when financial markets are affected by financial turmoils. We introduce a completely novel approach to diversification acti...

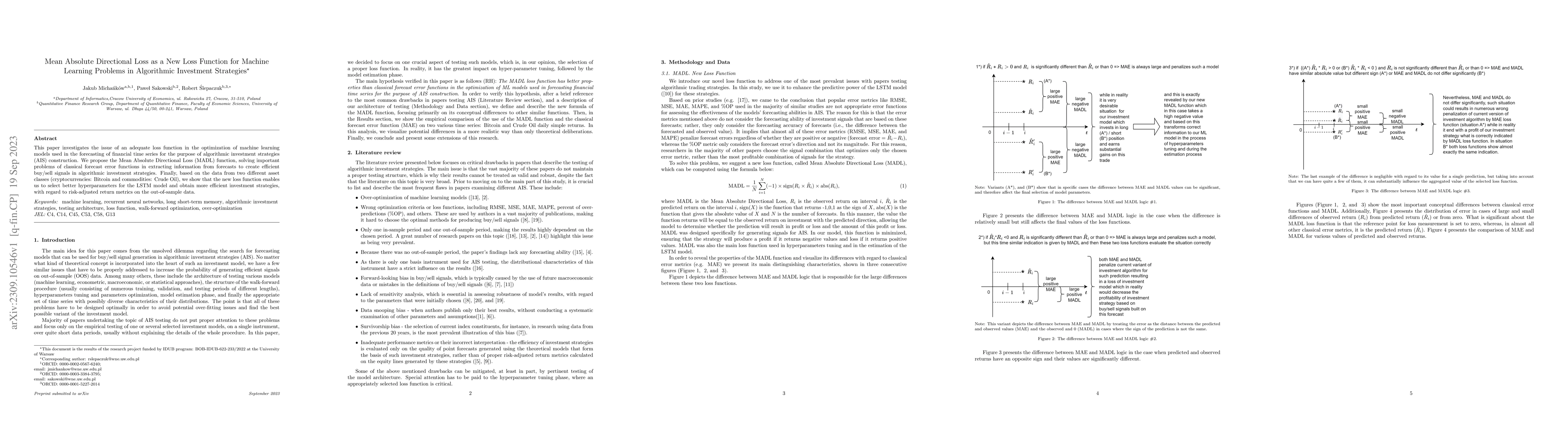

This paper investigates the issue of an adequate loss function in the optimization of machine learning models used in the forecasting of financial time series for the purpose of algorithmic investme...

We propose a new measure of systemic risk to analyze the impact of the major financial market turmoils in the stock markets from 2000 to 2023 in the USA, Europe, Brazil, and Japan. Our Implied Volat...

Regardless of the selected asset class and the level of model complexity (Transformer versus LSTM versus Perceptron/RNN), the GMADL loss function produces superior results than standard MSE-type loss ...

The paper explores the use of Deep Reinforcement Learning (DRL) in stock market trading, focusing on two algorithms: Double Deep Q-Network (DDQN) and Proximal Policy Optimization (PPO) and compares th...

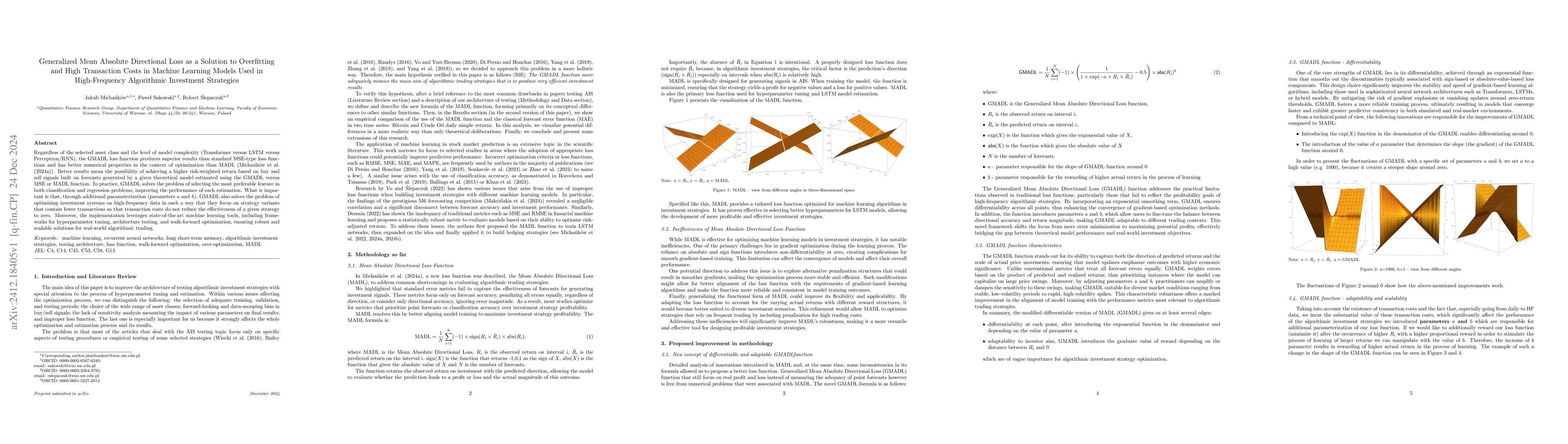

The proper design and architecture of testing of machine learning models, especially in their application to quantitative finance problems, is crucial. The most important in this process is selecting ...

This paper investigates an important problem of an appropriate variance-covariance matrix estimation in the Modern Portfolio Theory. We propose a novel framework for variancecovariance matrix estimati...

This paper explores the application of deep Q-learning to hedging at-the-money options on the S\&P~500 index. We develop an agent based on the Twin Delayed Deep Deterministic Policy Gradient (TD3) alg...

This paper investigates whether short-term market overreactions can be systematically predicted and monetized as momentum signals using high-frequency emotional information and modern machine learning...

This thesis studies the use of randomized neural networks for the estimation of exposure profiles and unilateral CVA of American options within a Monte Carlo framework. The analysis is carried out sep...