Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study a bivariate latent factor model for the pricing of commodity fu- tures. The two unobservable state variables representing the short and long term fac- tors are modelled as Ornstein-Uhlenbec...

The two unobservable state variables representing the short and long term factors introduced by Schwartz and Smith in [16] for risk-neutral pricing of futures contracts are modelled as two correlate...

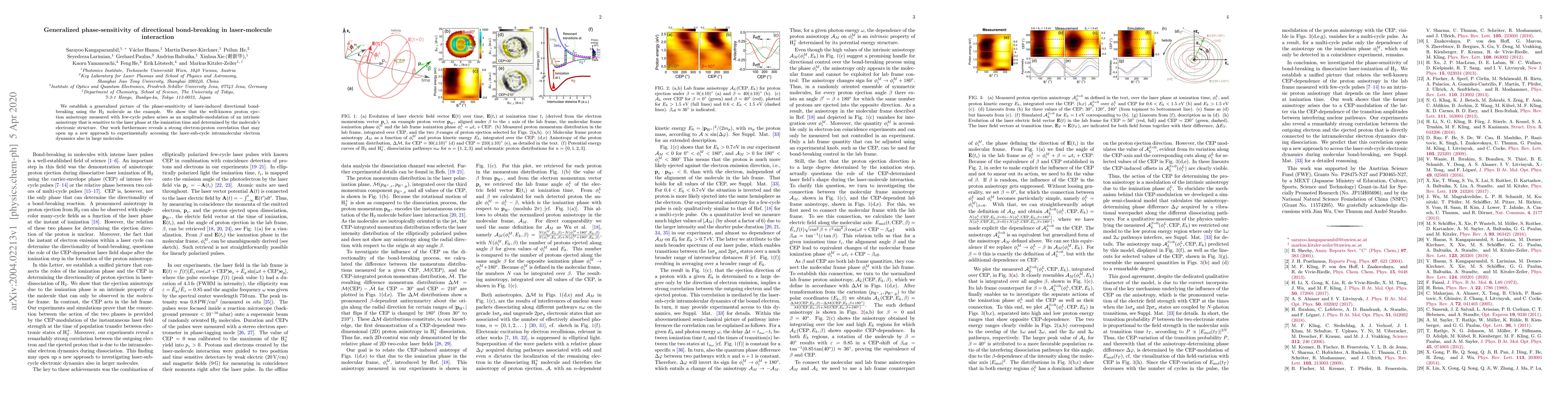

We establish a generalized picture of the phase-sensitivity of laser-induced directional bond-breaking using the H$_2$ molecule as the example. We show that the well-known proton ejection anisotropy...

In the analysis of commodity futures, it is commonly assumed that futures prices are driven by two latent factors: short-term fluctuations and long-term equilibrium price levels. In this study, we ext...

In stochastic multi-factor commodity models, it is often the case that futures prices are explained by two latent state variables which represent the short and long term stochastic factors. In this wo...

PDSim is an R package that enables users to simulate commodity futures prices using the polynomial diffusion model introduced in Filipovic and Larsson (2016) through both a Shiny web application and R...

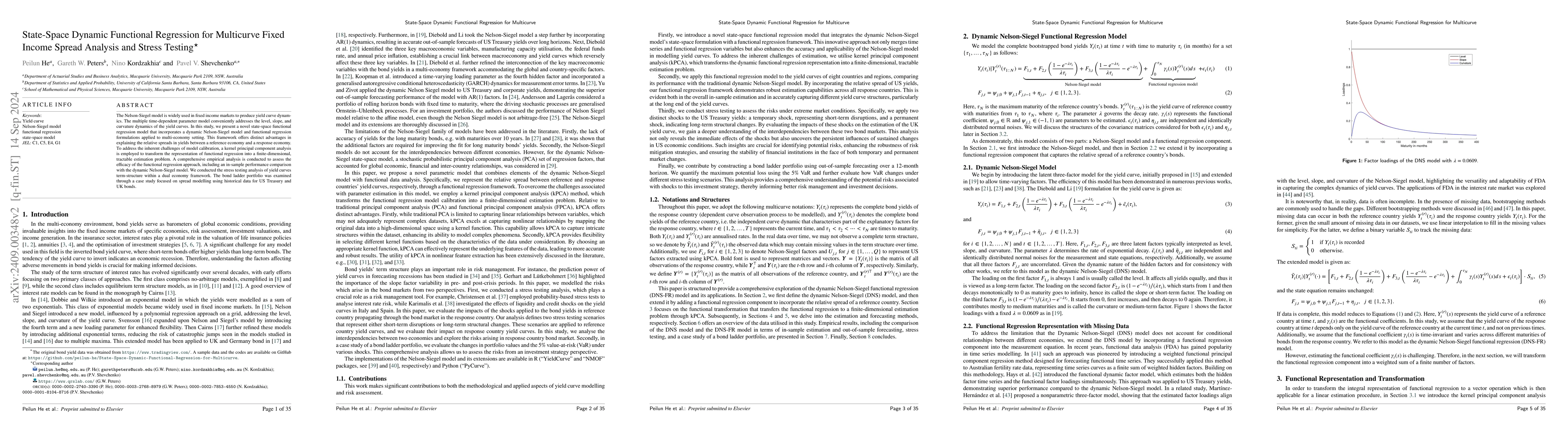

The Nelson-Siegel model is widely used in fixed income markets to produce yield curve dynamics. The multiple time-dependent parameter model conveniently addresses the level, slope, and curvature dynam...

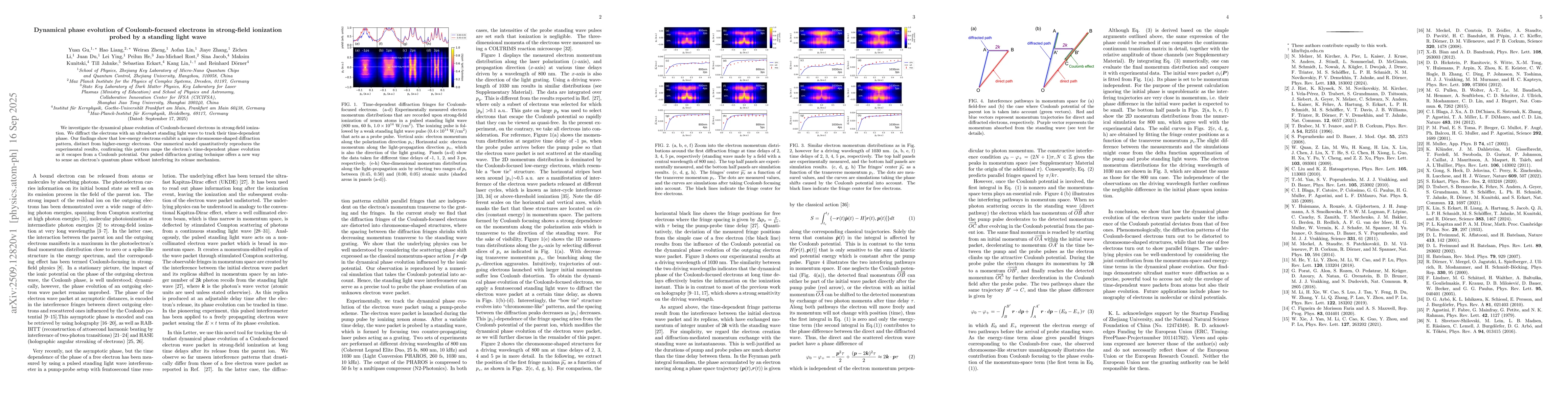

We investigate the dynamical phase evolution of Coulomb-focused electrons in strong-field ionization. We diffract the electrons with an ultrashort standing light wave to track their time-dependent pha...

This paper proposes distributed estimation procedures for three scalar-on-function regression models: the functional linear model (FLM), the functional non-parametric model (FNPM), and the functional ...