Academic Profile

Statistics

Similar Authors

Papers on arXiv

The current international landscape is turbulent and unstable, with frequent outbreaks of geopolitical conflicts worldwide. Geopolitical risk has emerged as a significant threat to regional and glob...

Agricultural products play a critical role in human development. With economic globalization and the financialization of agricultural products continuing to advance, the interconnections between dif...

The ongoing Russia-Ukraine conflict between two major agricultural powers has posed significant threats and challenges to the global food system and world food security. Focusing on the impact of th...

This paper combines the Copula-CoVaR approach with the ARMA-GARCH-skewed Student-t model to investigate the tail dependence structure and extreme risk spillover effects between the international agr...

This study investigates the impact of the COVID-19 pandemic on the stock market crash risk in China. For this purpose, we first estimated the conditional skewness of the return distribution from a G...

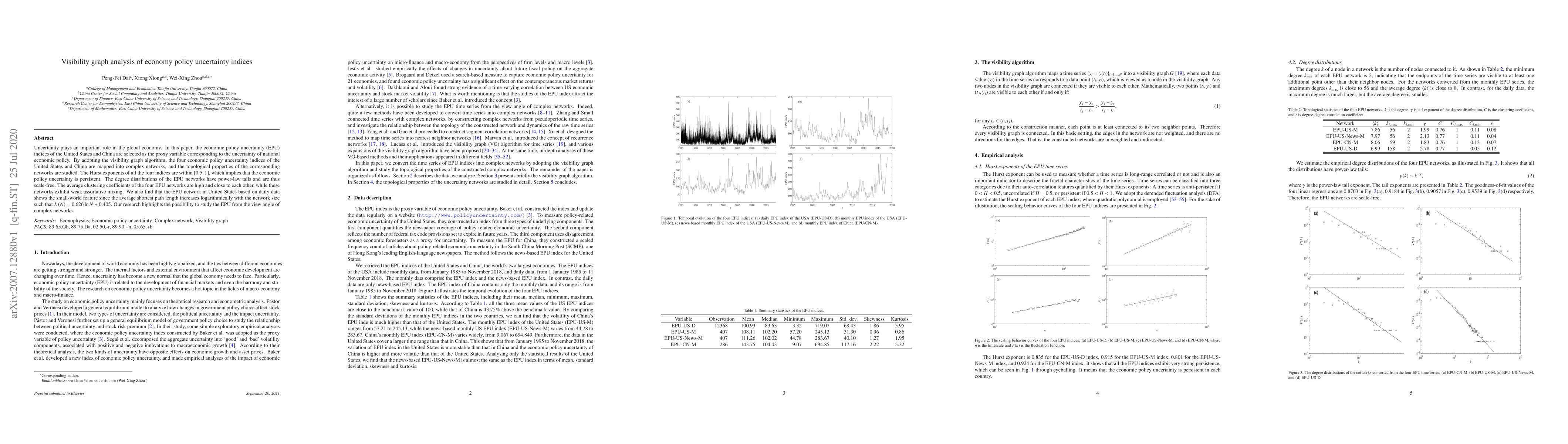

Uncertainty plays an important role in the global economy. In this paper, the economic policy uncertainty (EPU) indices of the United States and China are selected as the proxy variable correspondin...

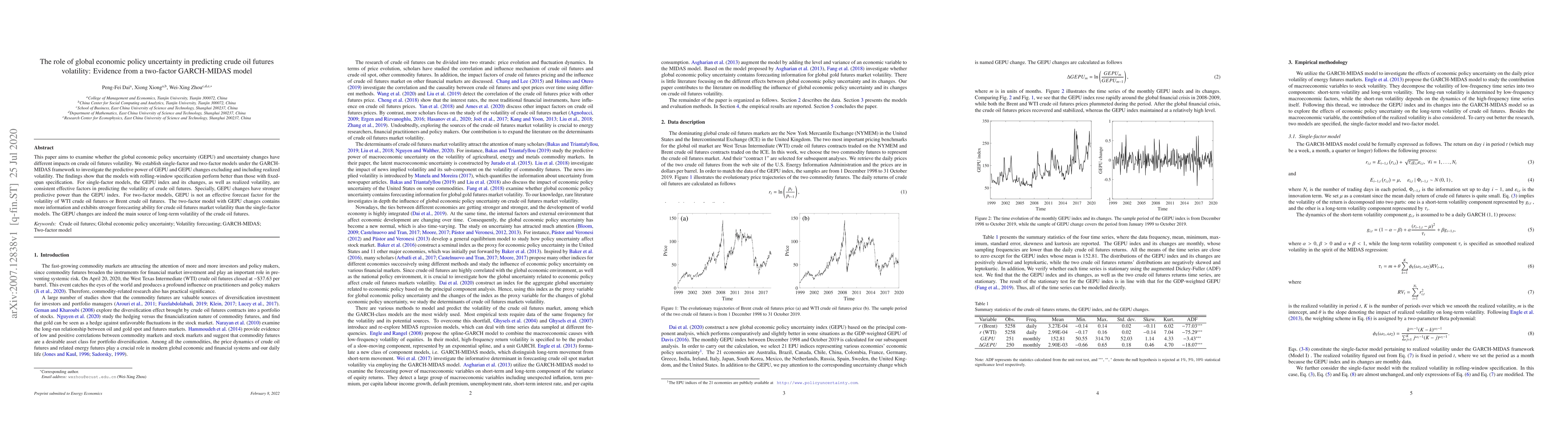

This paper aims to examine whether the global economic policy uncertainty (GEPU) and uncertainty changes have different impacts on crude oil futures volatility. We establish single-factor and two-fa...

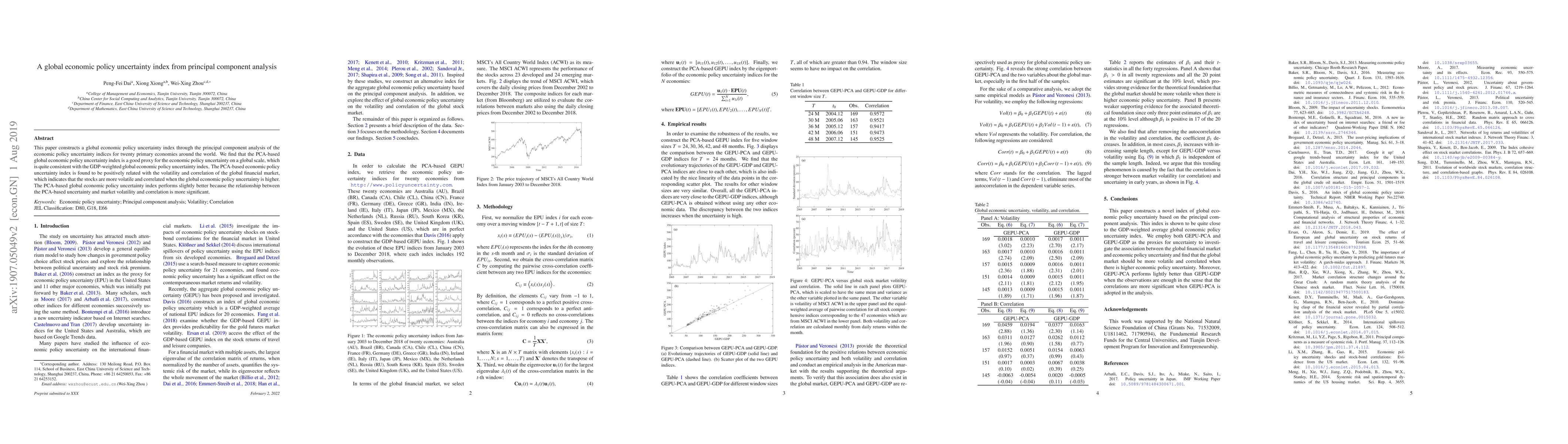

This paper constructs a global economic policy uncertainty index through the principal component analysis of the economic policy uncertainty indices for twenty primary economies around the world. We...

Stable and efficient food markets are crucial for global food security, yet international staple food markets are increasingly exposed to complex risks, including intensified risk contagion and escala...

With escalating macroeconomic uncertainty, the risk interlinkages between energy and food markets have become increasingly complex, posing serious challenges to global energy and food security. This p...