Academic Profile

Statistics

Similar Authors

Papers on arXiv

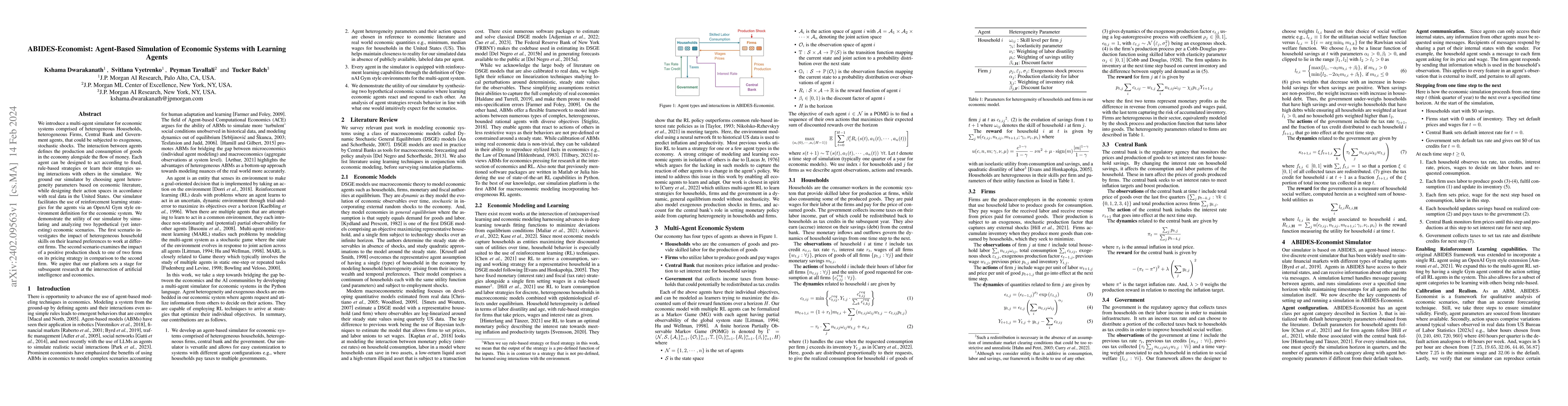

We introduce a multi-agent simulator for economic systems comprised of heterogeneous Households, heterogeneous Firms, Central Bank and Government agents, that could be subjected to exogenous, stocha...

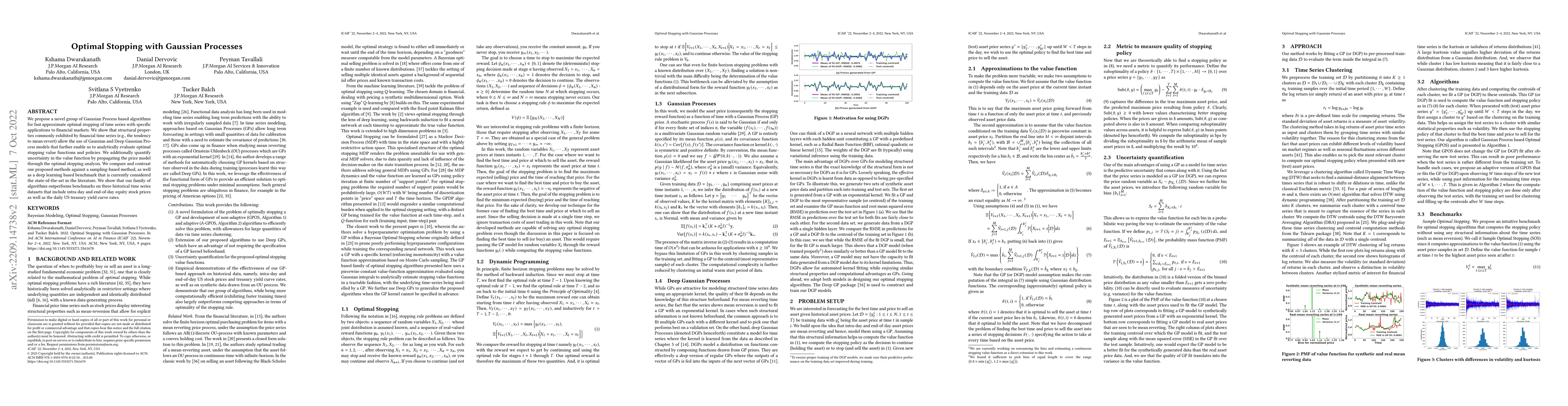

We propose a novel group of Gaussian Process based algorithms for fast approximate optimal stopping of time series with specific applications to financial markets. We show that structural properties...

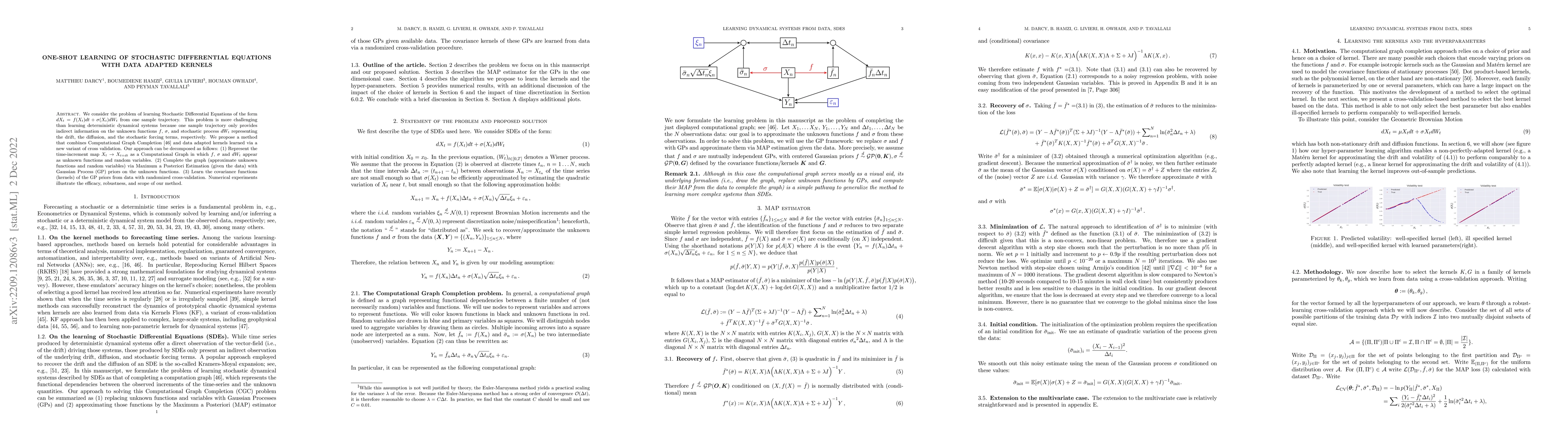

We consider the problem of learning Stochastic Differential Equations of the form $dX_t = f(X_t)dt+\sigma(X_t)dW_t $ from one sample trajectory. This problem is more challenging than learning determ...

There are essentially three kinds of approaches to Uncertainty Quantification (UQ): (A) robust optimization, (B) Bayesian, (C) decision theory. Although (A) is robust, it is unfavorable with respect...

K-Nearest Neighbors (KNN) search is a fundamental algorithm in artificial intelligence software with applications in robotics, and autonomous vehicles. These wide-ranging applications utilize KNN ei...

The design and testing of supervised machine learning models combine two fundamental distributions: (1) the training data distribution (2) the testing data distribution. Although these two distribut...

State-of-the-art machine learning models are vulnerable to data poisoning attacks whose purpose is to undermine the integrity of the model. However, the current literature on data poisoning attacks ...

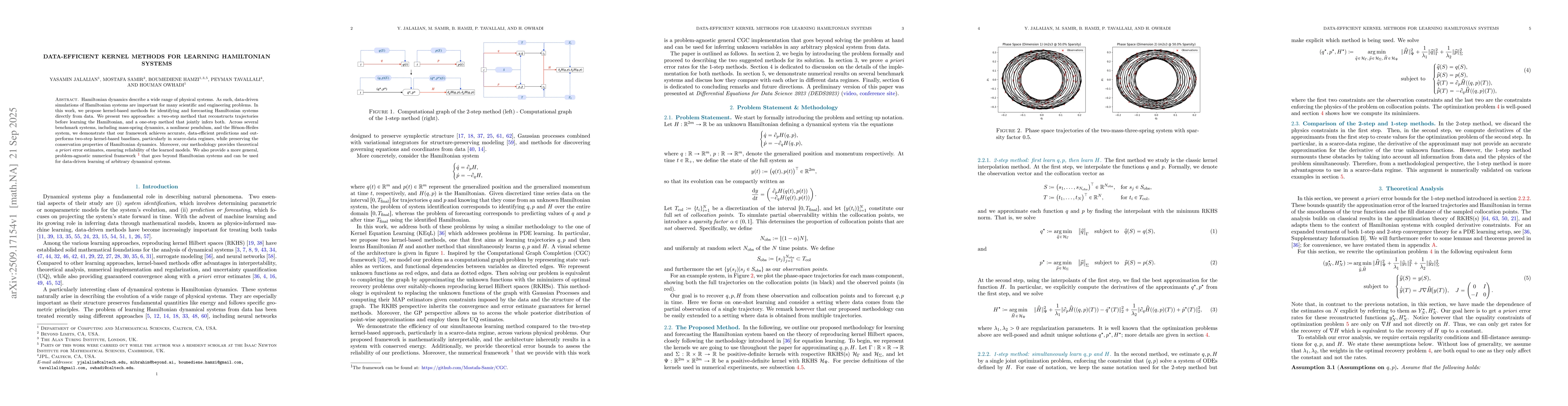

Hamiltonian dynamics describe a wide range of physical systems. As such, data-driven simulations of Hamiltonian systems are important for many scientific and engineering problems. In this work, we pro...