Philipp Otto

European University Viadrina, Medizinische Hochschule Brandenburg, Universität Bamberg

Academic Profile

Statistics

Similar Authors

Papers on arXiv

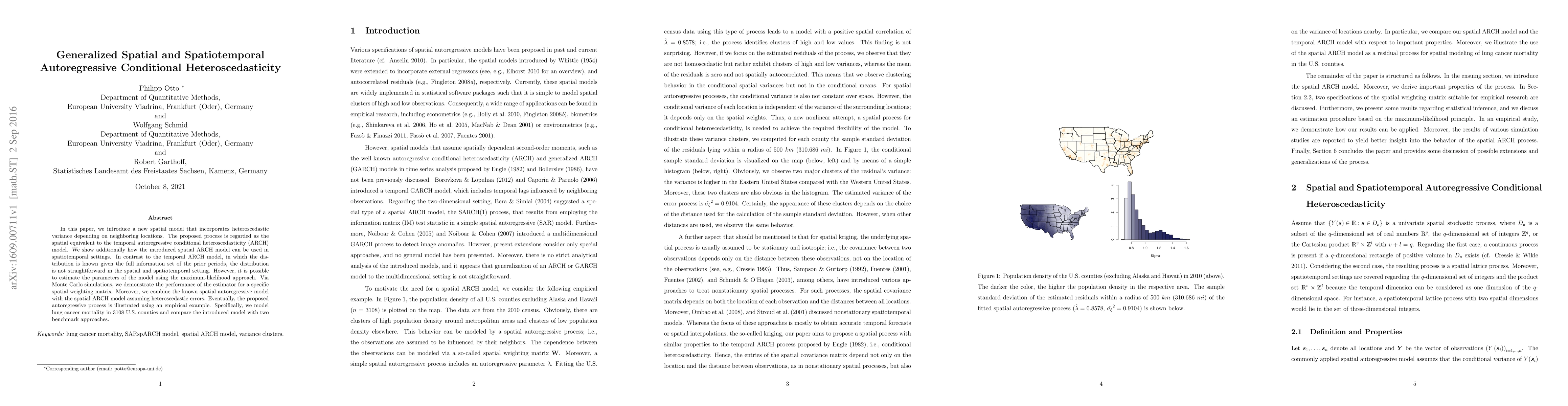

In this paper, we introduce a new spatial model that incorporates heteroscedastic variance depending on neighboring locations. The proposed process is regarded as the spatial equivalent to the tempo...

The assessment of corporate sustainability performance is extremely relevant in facilitating the transition to a green and low-carbon intensity economy. However, companies located in different areas...

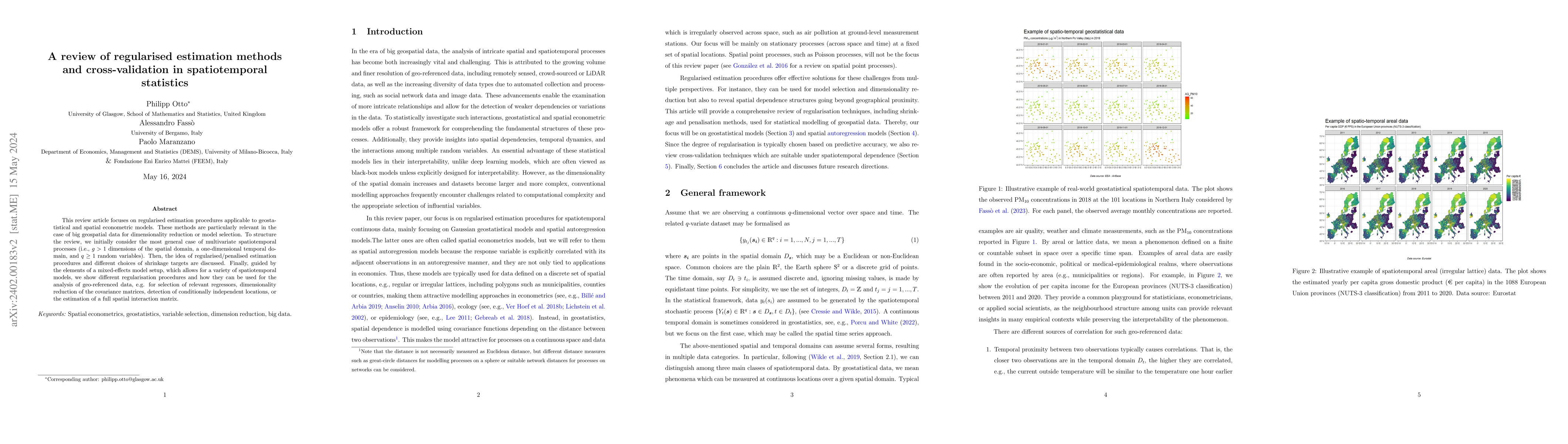

This review article focuses on regularised estimation procedures applicable to geostatistical and spatial econometric models. These methods are particularly relevant in the case of big geospatial da...

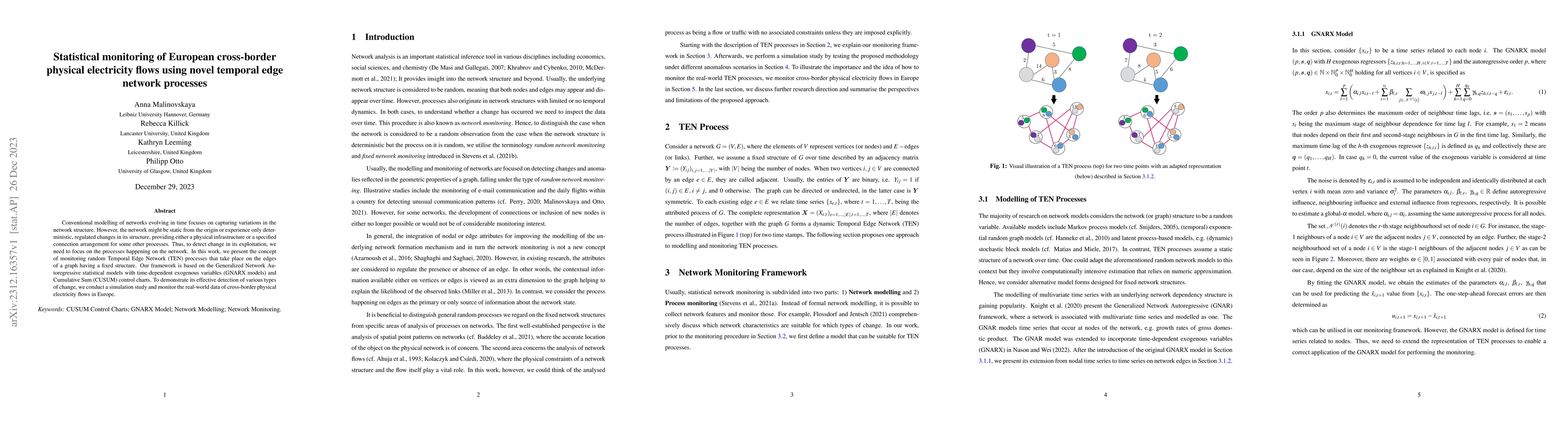

Conventional modelling of networks evolving in time focuses on capturing variations in the network structure. However, the network might be static from the origin or experience only deterministic, r...

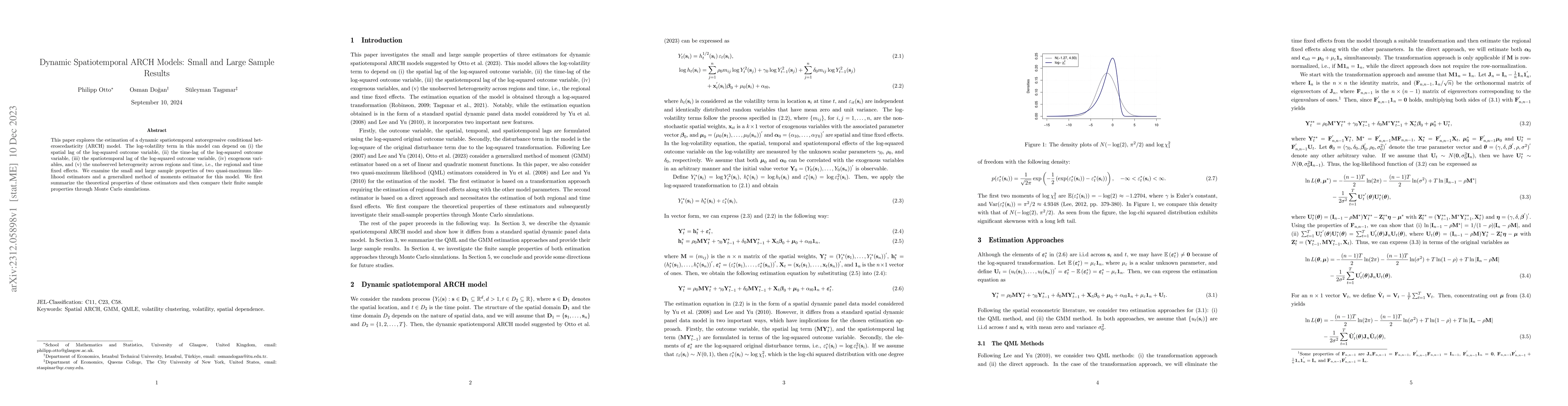

This paper explores the estimation of a dynamic spatiotemporal autoregressive conditional heteroscedasticity (ARCH) model. The log-volatility term in this model can depend on (i) the spatial lag of ...

Stock market indices are volatile by nature, and sudden shocks are known to affect volatility patterns. The autoregressive conditional heteroskedasticity (ARCH) and generalized ARCH (GARCH) models n...

This study presents a comparative analysis of three predictive models with an increasing degree of flexibility: hidden dynamic geostatistical models (HDGM), generalised additive mixed models (GAMM),...

In this paper, we introduce the concept of fractional integration for spatial autoregressive models. We show that the range of the dependence can be spatially extended or diminished by introducing a...

Spatial and spatiotemporal volatility models are a class of models designed to capture spatial dependence in the volatility of spatial and spatiotemporal data. Spatial dependence in the volatility m...

This paper presents a novel dynamic network autoregressive conditional heteroscedasticity (ARCH) model based on spatiotemporal ARCH models to forecast volatility in the US stock market. To improve t...

This article introduces a dynamic spatiotemporal stochastic volatility (SV) model with explicit terms for the spatial, temporal, and spatiotemporal spillover effects. Moreover, the model includes ti...

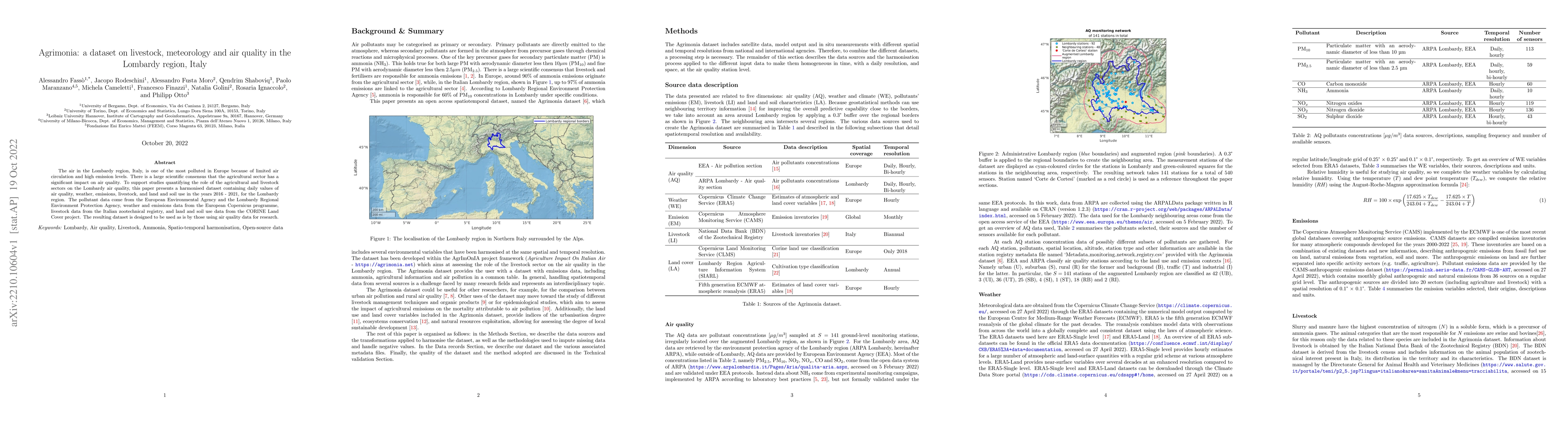

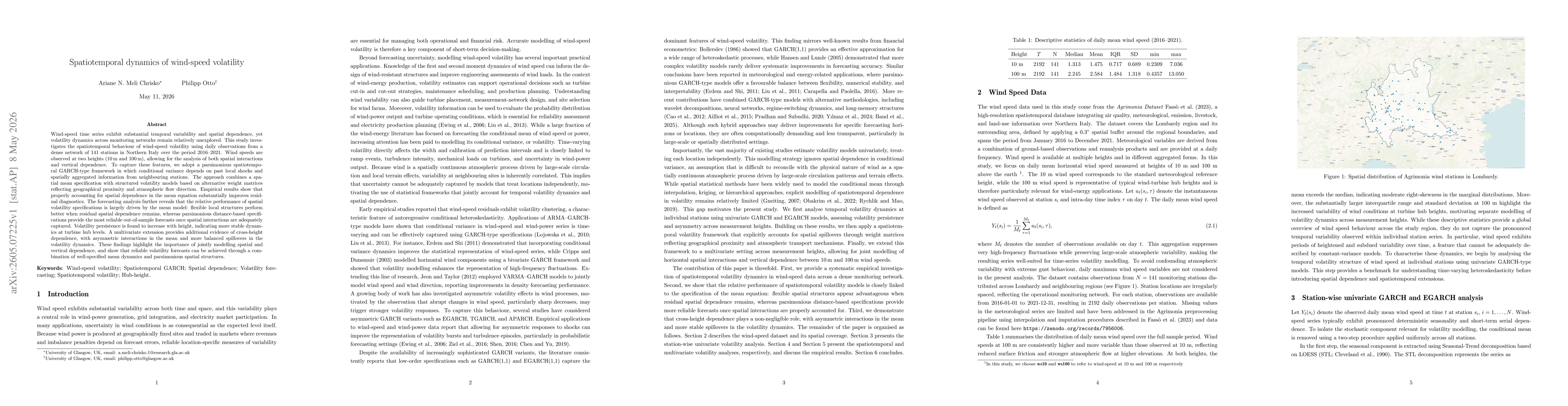

The air in the Lombardy region, Italy, is one of the most polluted in Europe because of limited air circulation and high emission levels. There is a large scientific consensus that the agricultural ...

The rapid advancement of models based on artificial intelligence demands innovative monitoring techniques which can operate in real time with low computational costs. In machine learning, especially...

We propose a novel model selection algorithm based on a penalized maximum likelihood estimator (PMLE) for functional hidden dynamic geostatistical models (f-HDGM). These models employ a classic mixe...

This paper introduces a multivariate spatiotemporal autoregressive conditional heteroscedasticity (ARCH) model based on a vec-representation. The model includes instantaneous spatial autoregressive ...

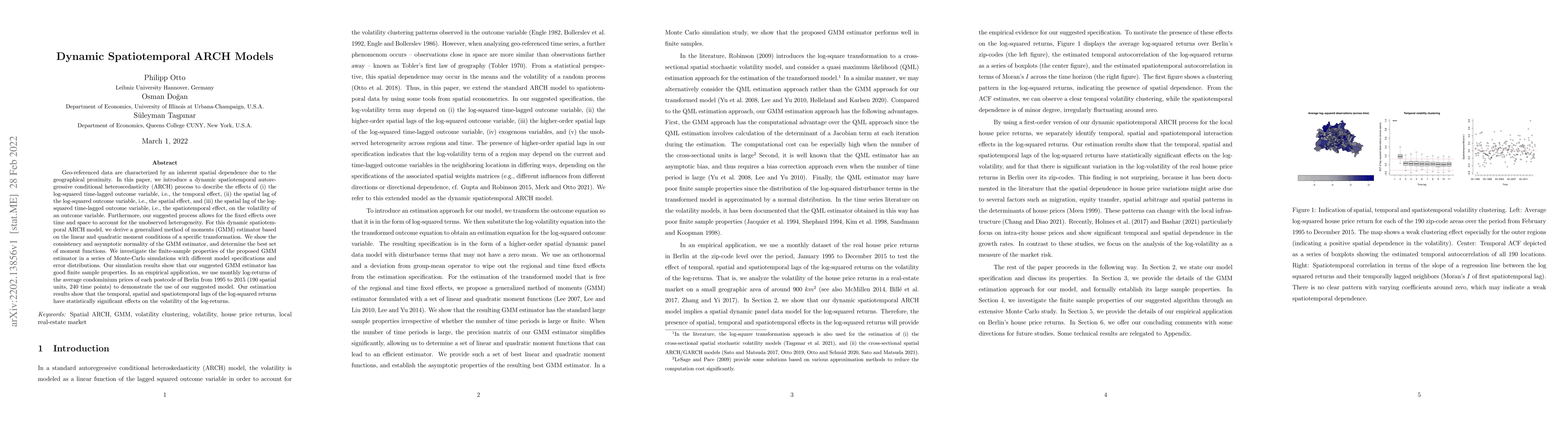

Geo-referenced data are characterized by an inherent spatial dependence due to the geographical proximity. In this paper, we introduce a dynamic spatiotemporal autoregressive conditional heterosceda...

In time-series analyses, particularly for finance, generalized autoregressive conditional heteroscedasticity (GARCH) models are widely applied statistical tools for modelling volatility clusters (i....

Understanding the usage patterns for bike-sharing systems is essential in terms of supporting and enhancing operational planning for such schemes. Studies have demonstrated how factors such as weath...

Complex systems which can be represented in the form of static and dynamic graphs arise in different fields, e.g. communication, engineering and industry. One of the interesting problems in analysin...

The application of network analysis has found great success in a wide variety of disciplines; however, the popularity of these approaches has revealed the difficulty in handling networks whose compl...

Spatial econometric research typically relies on the assumption that the spatial dependence structure is known in advance and is represented by a deterministic spatial weights matrix. Contrary to cl...

In time-series analyses, particularly for finance, generalized autoregressive conditional heteroscedasticity (GARCH) models are widely applied statistical tools for modelling volatility clusters (i....

In this paper, a general overview on spatial and spatiotemporal ARCH models is provided. In particular, we distinguish between three different spatial ARCH-type models. In addition to the original d...

In this paper, we propose a two-step lasso estimation approach to estimate the full spatial weights matrix of spatiotemporal autoregressive models. In addition, we allow for an unknown number of str...

We introduce a dynamic spatiotemporal volatility model that extends traditional approaches by incorporating spatial, temporal, and spatiotemporal spillover effects, along with volatility-specific obse...

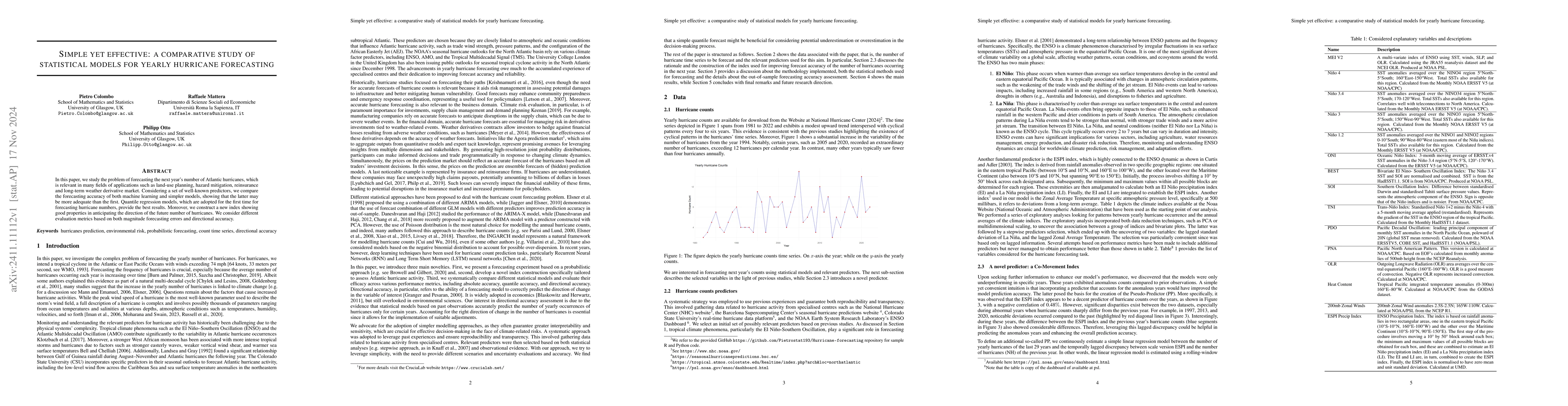

In this paper, we study the problem of forecasting the next year's number of Atlantic hurricanes, which is relevant in many fields of applications such as land-use planning, hazard mitigation, reinsur...

In this study, we propose a novel application of spatiotemporal clustering in the environmental sciences, with a particular focus on regionalised time series of greenhouse gases (GHGs) emissions from ...

In this study, we introduce a novel and comprehensive extension of a Bayesian spatio-temporal disease mapping model that explicitly accounts for gender-specific effects of meteorological exposures. Le...

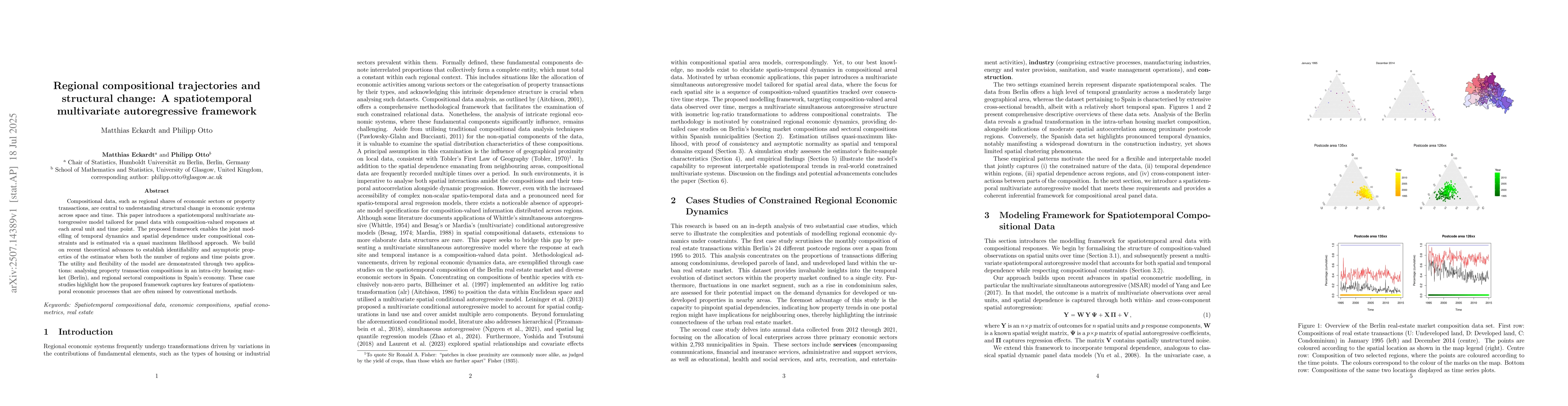

Compositional data, such as regional shares of economic sectors or property transactions, are central to understanding structural change in economic systems across space and time. This paper introduce...

This paper examines several network-based volatility models for oil prices, capturing spillovers among OPEC oil-exporting countries by embedding novel network structures into ARCH-type models. We appl...

We introduce a heterogeneous spatiotemporal GARCH model for geostatistical data or processes on networks, e.g., for modelling and predicting financial return volatility across firms in a latent spatia...

This paper proposes a novel low-rank approximation to the multivariate State-Space Model. The Stochastic Partial Differential Equation (SPDE) approach is applied component-wise to the independent-in-t...

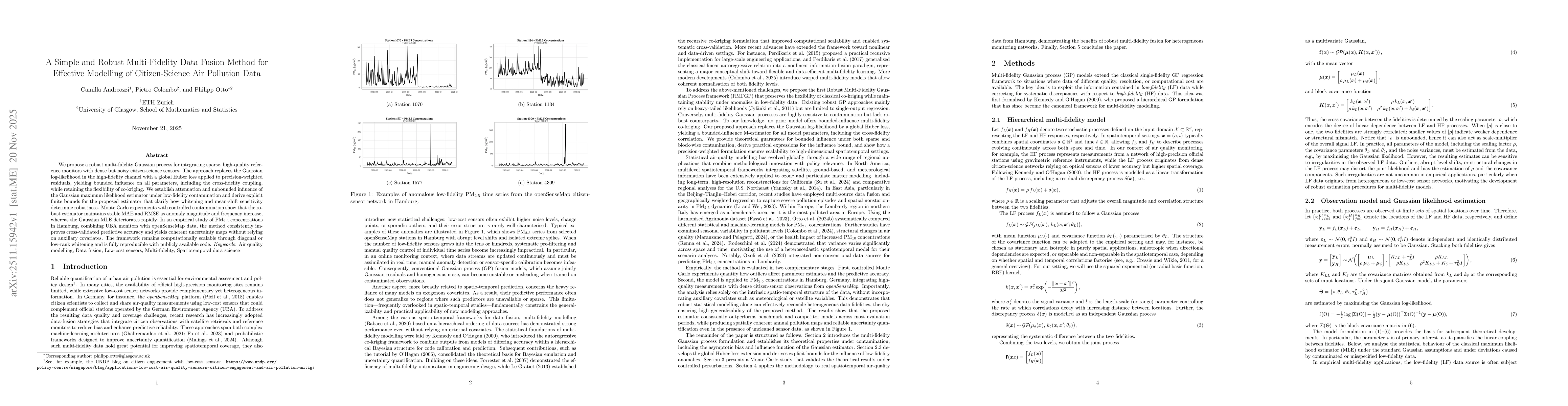

We propose a robust multi-fidelity Gaussian process for integrating sparse, high-quality reference monitors with dense but noisy citizen-science sensors. The approach replaces the Gaussian log-likelih...

We present an estimation procedure of spatial and temporal effects in spatiotemporal autoregressive panel data models using the Least Absolute Shrinkage and Selection Operator, LASSO (Tibshirani, 1996...

This paper introduces a spatiotemporal exponential generalised autoregressive conditional heteroscedasticity (spatiotemporal E-GARCH) model, extending traditional spatiotemporal GARCH models by incorp...

Various spatiotemporal and network GARCH models have recently been proposed to capture volatility interactions, such as the transmission of market risk across financial networks. These approaches rely...

Wind-speed processes exhibit substantial temporal variability and spatial dependence, yet volatility dynamics across monitoring networks remain relatively unexplored. This study investigates the spati...