Academic Profile

Statistics

Similar Authors

Papers on arXiv

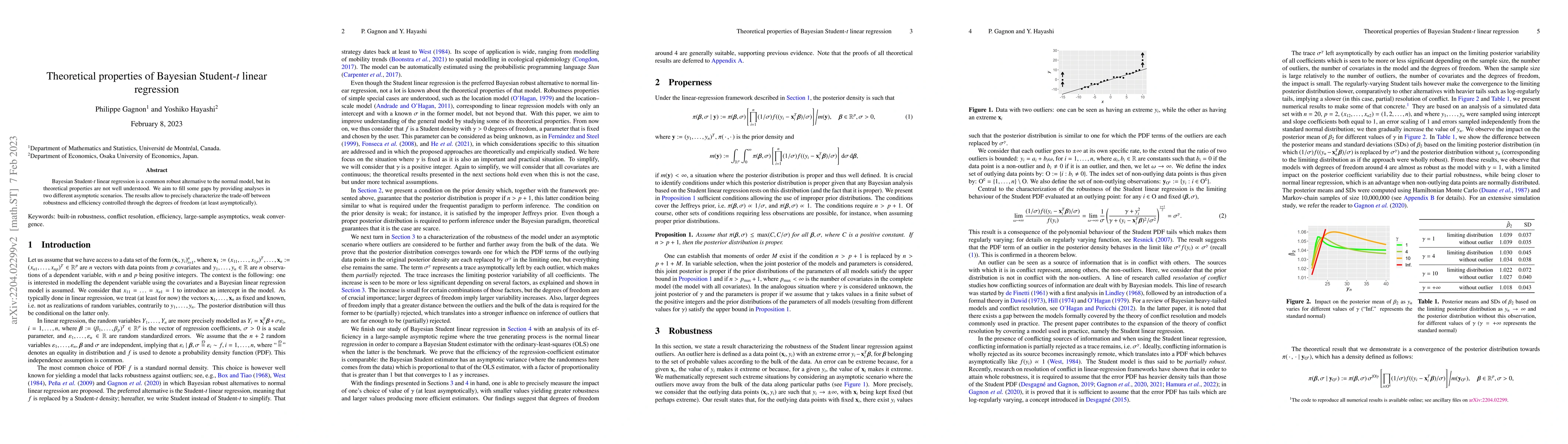

Lifted samplers form a class of Markov chain Monte Carlo methods which has drawn a lot attention in recent years due to superior performance in challenging Bayesian applications. A canonical example...

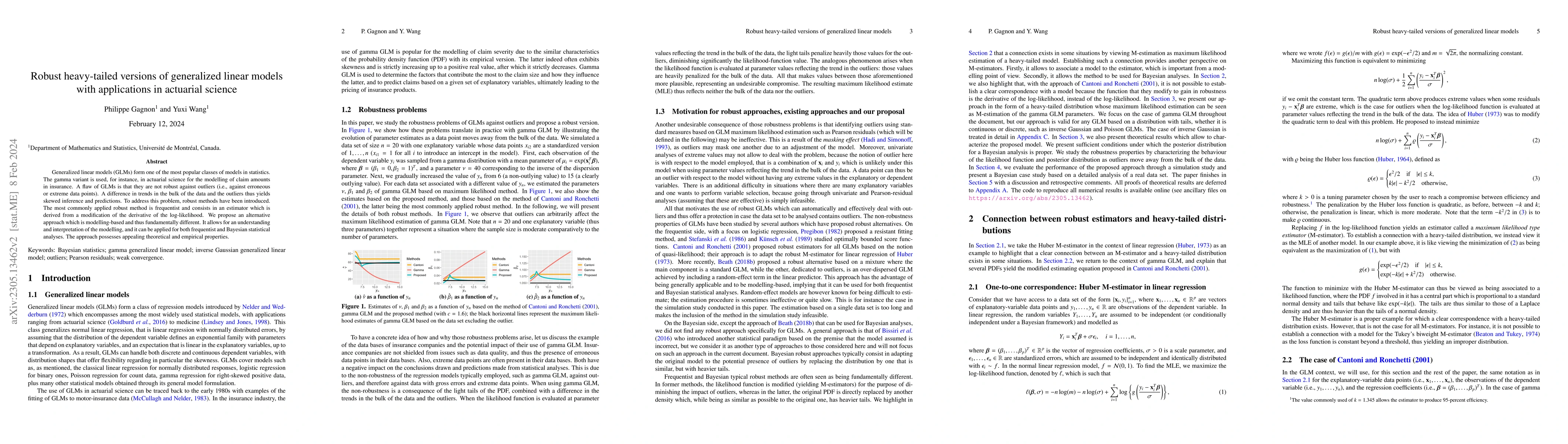

Generalized linear models (GLMs) form one of the most popular classes of models in statistics. The gamma variant is used, for instance, in actuarial science for the modelling of claim amounts in ins...

Multiple-try Metropolis (MTM) is a popular Markov chain Monte Carlo method with the appealing feature of being amenable to parallel computing. At each iteration, it samples several candidates for th...

Bayesian Student-$t$ linear regression is a common robust alternative to the normal model, but its theoretical properties are not well understood. We aim to fill some gaps by providing analyses in t...

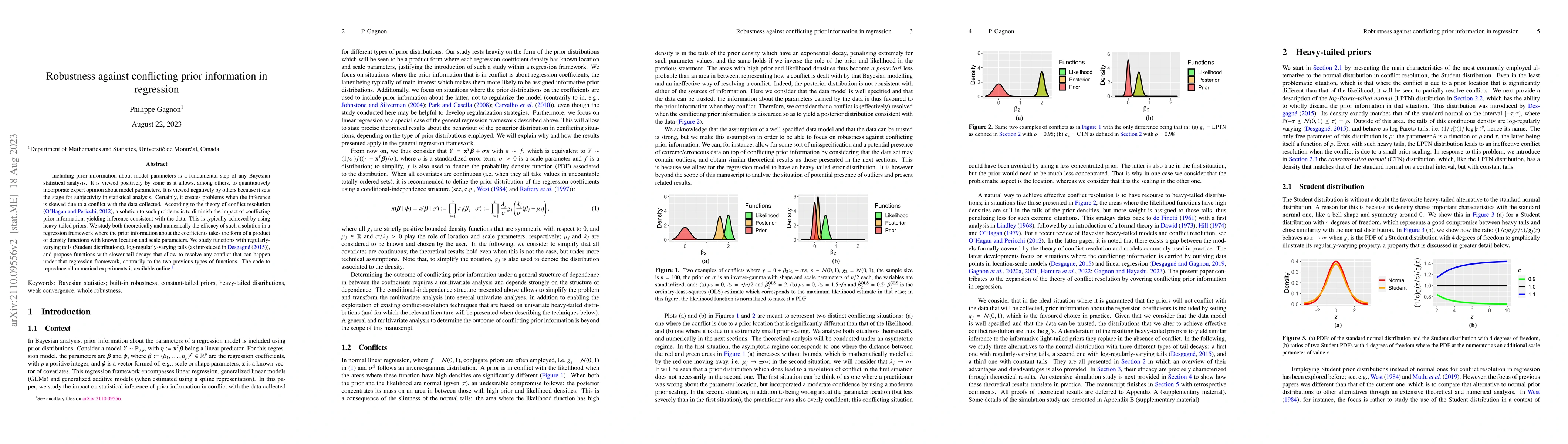

Including prior information about model parameters is a fundamental step of any Bayesian statistical analysis. It is viewed positively by some as it allows, among others, to quantitatively incorpora...

High-dimensional limit theorems have been shown useful to derive tuning rules for finding the optimal scaling in random-walk Metropolis algorithms. The assumptions under which weak convergence resul...

A Peskun ordering between two samplers, implying a dominance of one over the other, is known among the Markov chain Monte Carlo community for being a remarkably strong result. It is however also kno...

Incorporating information about the target distribution in proposal mechanisms generally produces efficient Markov chain Monte Carlo algorithms (or at least, algorithms that are more efficient than ...

Non-reversible Markov chain Monte Carlo methods often outperform their reversible counterparts in terms of asymptotic variance of ergodic averages and mixing properties. Lifting the state-space (Che...

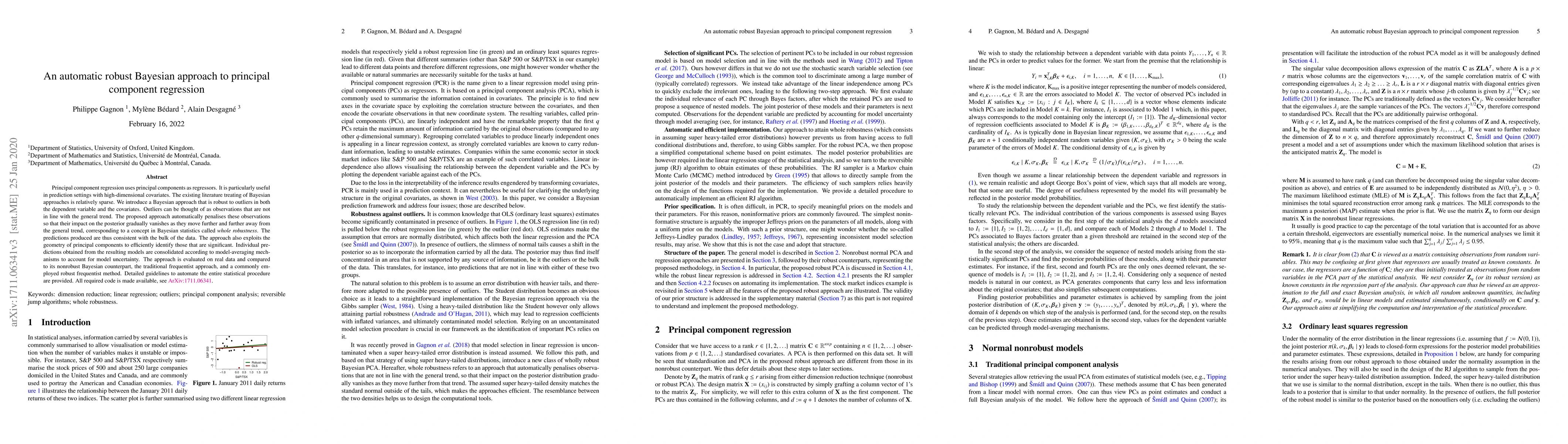

Principal component regression uses principal components as regressors. It is particularly useful in prediction settings with high-dimensional covariates. The existing literature treating of Bayesia...

Heavy-tailed models are often used as a way to gain robustness against outliers in Bayesian analyses. On the other side, in frequentist analyses, M-estimators are often employed. In this paper, the tw...

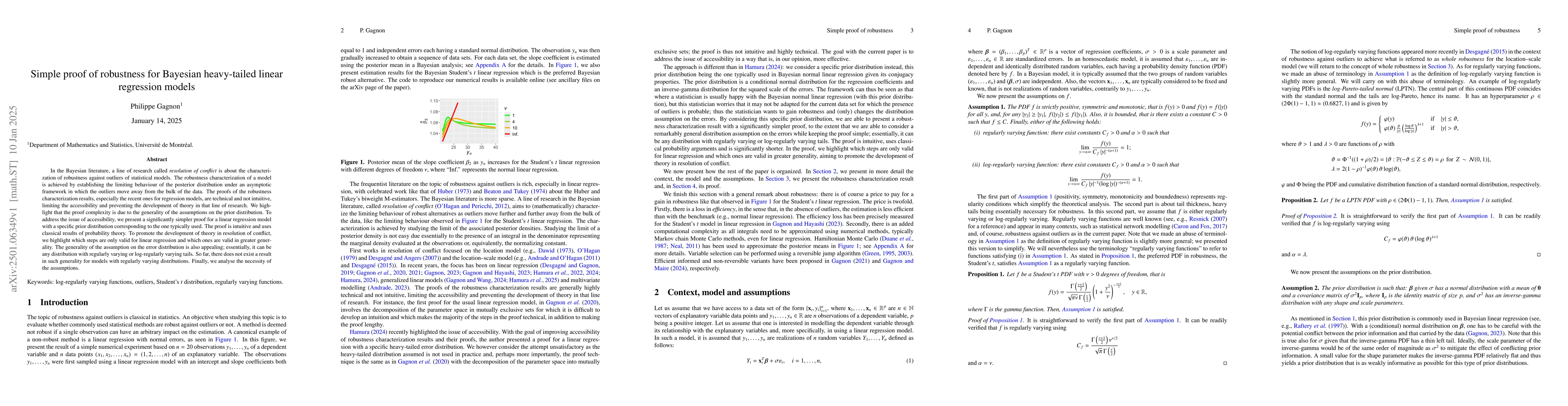

In the Bayesian literature, a line of research called resolution of conflict is about the characterization of robustness against outliers of statistical models. The robustness characterization of a mo...

Probabilistic principal component analysis (PCA) and its Bayesian variant (BPCA) are widely used for dimension reduction in machine learning and statistics. The main advantage of probabilistic PCA ove...