Academic Profile

Statistics

Similar Authors

Papers on arXiv

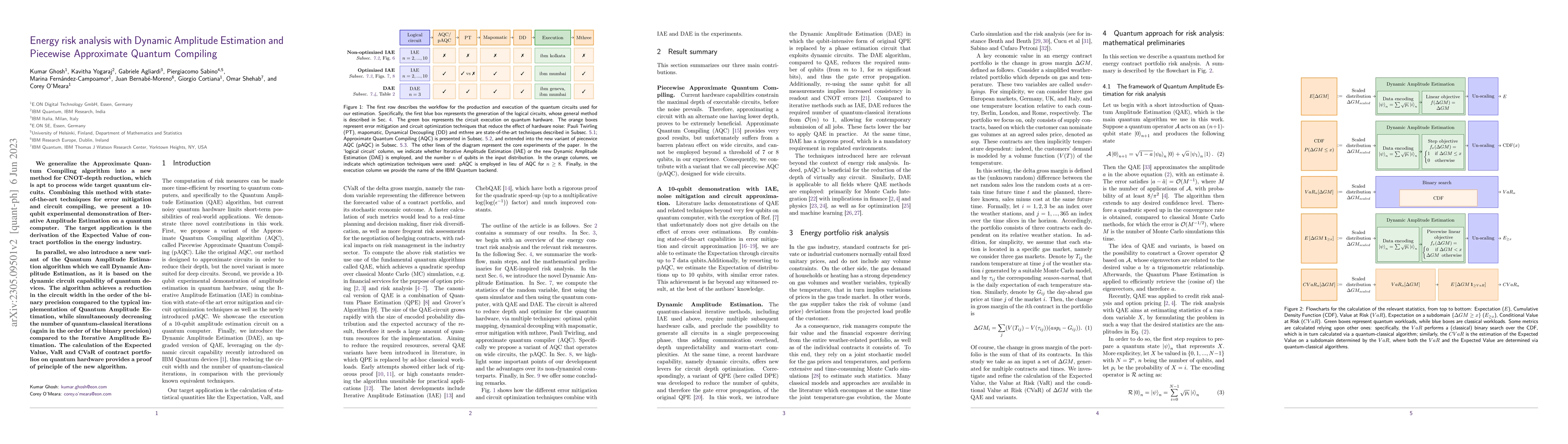

We generalize the Approximate Quantum Compiling algorithm into a new method for CNOT-depth reduction, which is apt to process wide target quantum circuits. Combining this method with state-of-the-ar...

In this article we focus on the pricing of exchange options when the dynamic of logprices follows either the well-known variance gamma or the recent variance gamma++ process introduced in Gardini et...

We develop efficient methods for simulating processes of Ornstein-Uhlenbeck type related to the class of $p$-tempered $\alpha$-stable ($\ts$) distributions. Our results hold for both the univariate ...

In this study we consider the pricing of energy derivatives when the evolution of spot prices is modeled with a normal tempered stable driven Ornstein-Uhlenbeck process. Such processes are the gener...

In this study we consider the pricing of energy derivatives when the evolution of spot prices follows a tempered stable or a CGMY driven Ornstein- Uhlenbeck process. To this end, we first calculate ...

Constructing \Levy-driven Ornstein-Uhlenbeck processes is a task closely related to the notion of self-decomposability. In particular, their transition laws are linked to the properties of what will...

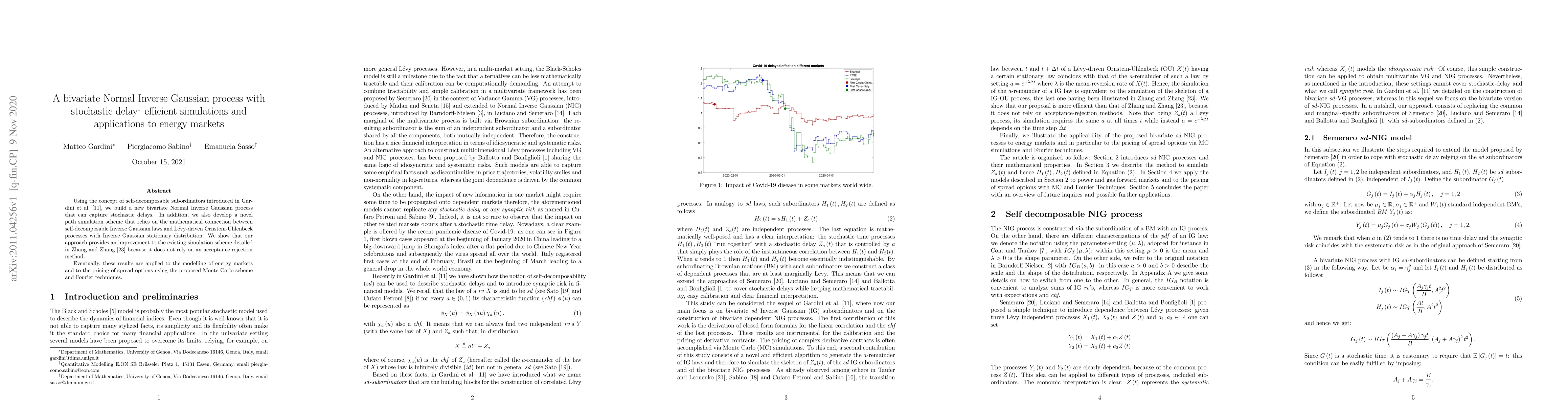

Using the concept of self-decomposable subordinators introduced in Gardini et al. [11], we build a new bivariate Normal Inverse Gaussian process that can capture stochastic delays. In addition, we a...

In this study we define a three-step procedure to relate the self-decomposability of the stationary law of a generalized Ornstein-Uhlenbeck process to the law of the increments of such processes. Ba...

We investigate the distributional properties of two generalized Ornstein-Uhlenbeck (OU) processes whose stationary distributions are the gamma law and the bilateral gamma law, respectively. The said...