Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study a theoretical and algorithmic framework for structured prediction in the online learning setting. The problem of structured prediction, i.e. estimating function where the output space lacks a...

We explore online learning in episodic loop-free Markov decision processes on non-stationary environments (changing losses and probability transitions). Our focus is on the Concave Utility Reinforce...

We address the problem of active online assortment optimization problem with preference feedback, which is a framework for modeling user choices and subsetwise utility maximization. The framework is...

We address the problem of stochastic combinatorial semi-bandits, where a player selects among $P$ actions from the power set of a set containing $d$ base items. Adaptivity to the problem's structure...

We introduce an online mathematical framework for survival analysis, allowing real time adaptation to dynamic environments and censored data. This framework enables the estimation of event time dist...

Many machine learning tasks can be solved by minimizing a convex function of an occupancy measure over the policies that generate them. These include reinforcement learning, imitation learning, amon...

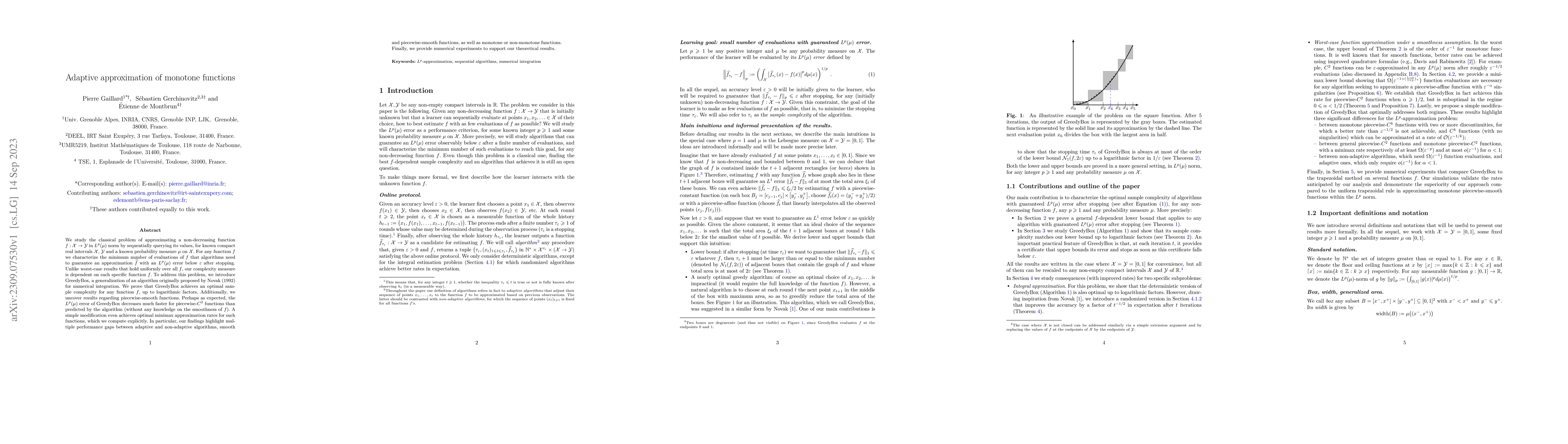

We study the classical problem of approximating a non-decreasing function $f: \mathcal{X} \to \mathcal{Y}$ in $L^p(\mu)$ norm by sequentially querying its values, for known compact real intervals $\...

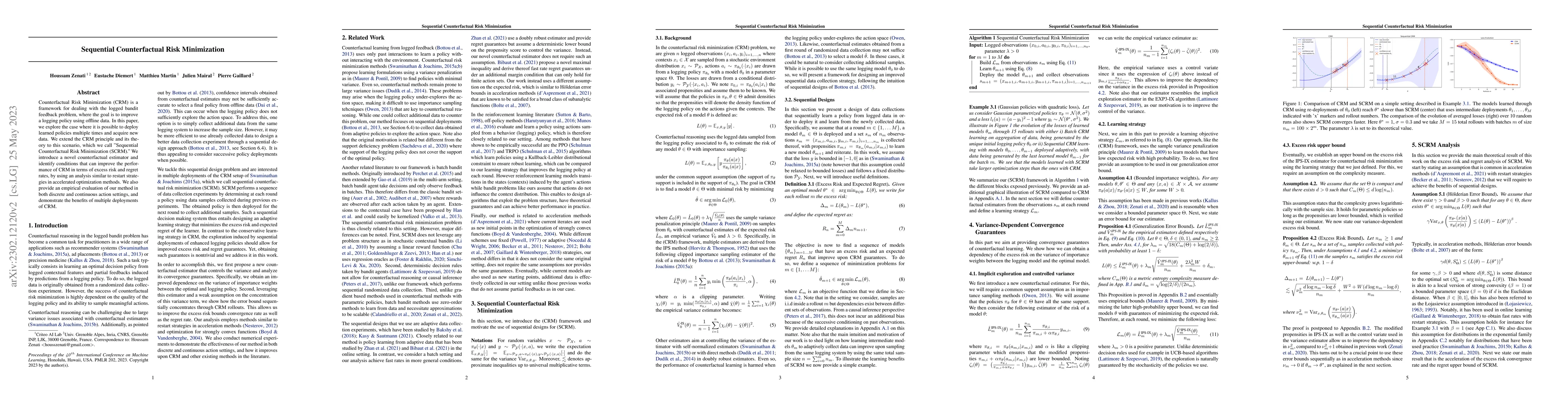

Counterfactual Risk Minimization (CRM) is a framework for dealing with the logged bandit feedback problem, where the goal is to improve a logging policy using offline data. In this paper, we explore...

Integrating renewable energy into the power grid while balancing supply and demand is a complex issue, given its intermittent nature. Demand side management (DSM) offers solutions to this challenge....

We address the problem of \emph{`Internal Regret'} in \emph{Sleeping Bandits} in the fully adversarial setup, as well as draw connections between different existing notions of sleeping regrets in th...

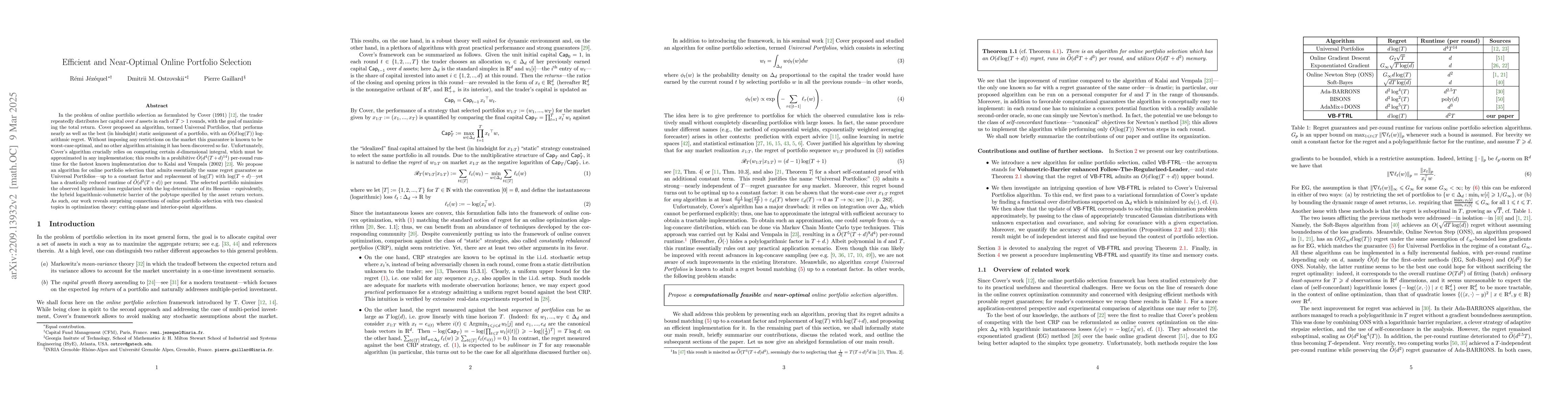

In the problem of online portfolio selection as formulated by Cover (1991), the trader repeatedly distributes her capital over $ d $ assets in each of $ T > 1 $ rounds, with the goal of maximizing t...

We study the problem of $K$-armed dueling bandit for both stochastic and adversarial environments, where the goal of the learner is to aggregate information through relative preferences of pair of d...

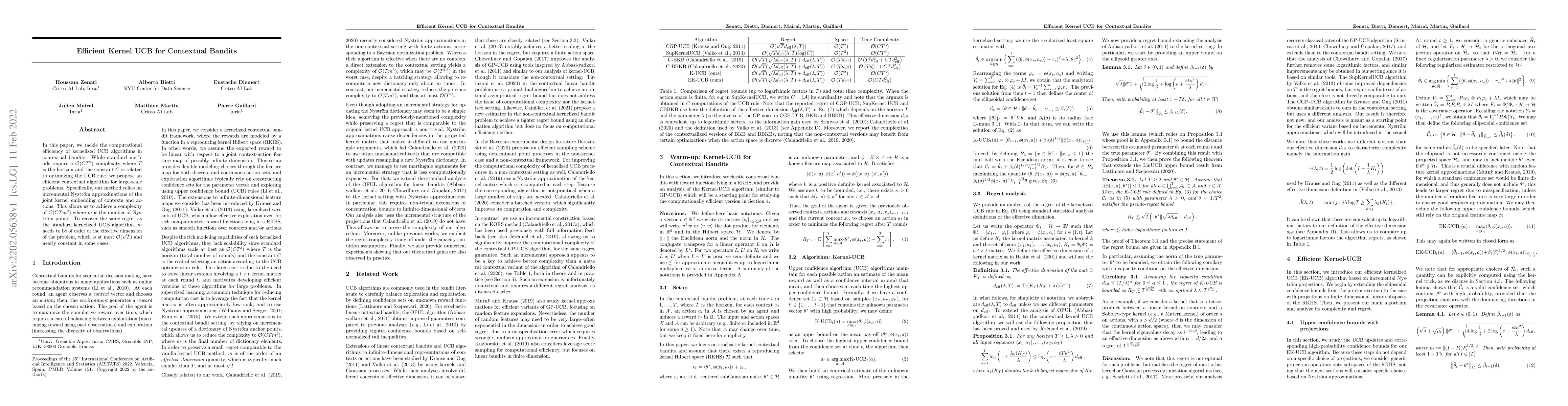

In this paper, we tackle the computational efficiency of kernelized UCB algorithms in contextual bandits. While standard methods require a O(CT^3) complexity where T is the horizon and the constant ...

In the fixed budget thresholding bandit problem, an algorithm sequentially allocates a budgeted number of samples to different distributions. It then predicts whether the mean of each distribution i...

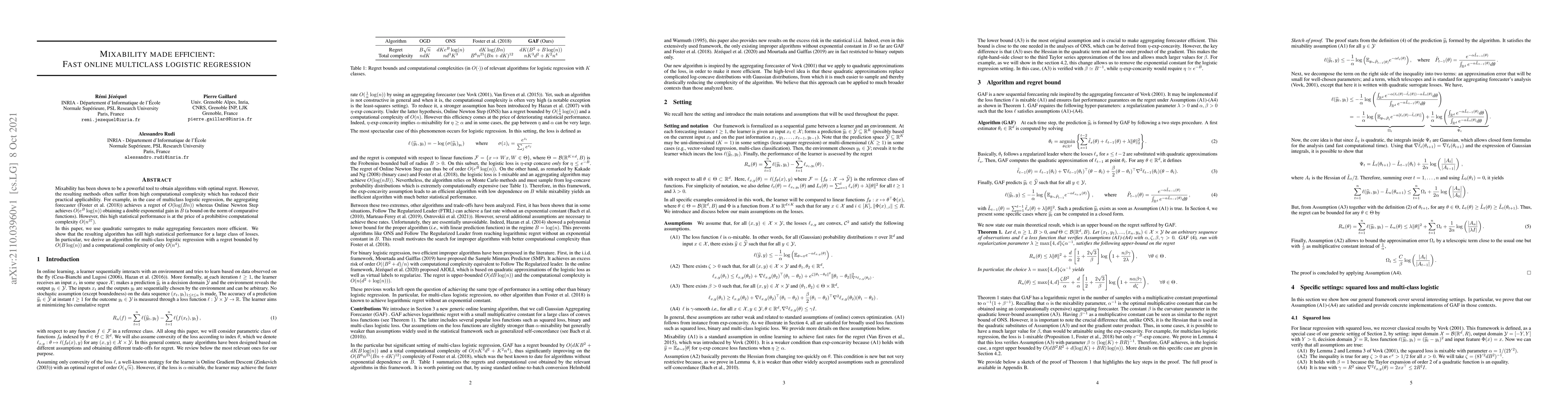

Mixability has been shown to be a powerful tool to obtain algorithms with optimal regret. However, the resulting methods often suffer from high computational complexity which has reduced their pract...

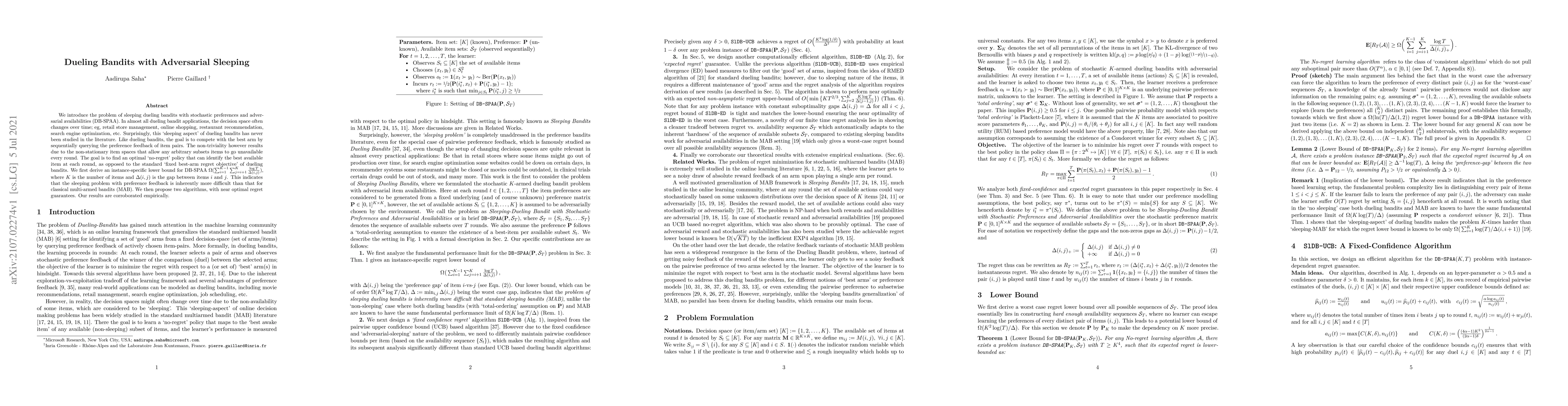

We introduce the problem of sleeping dueling bandits with stochastic preferences and adversarial availabilities (DB-SPAA). In almost all dueling bandit applications, the decision space often changes...

We introduce the continuized Nesterov acceleration, a close variant of Nesterov acceleration whose variables are indexed by a continuous time parameter. The two variables continuously mix following ...

We introduce the "continuized" Nesterov acceleration, a close variant of Nesterov acceleration whose variables are indexed by a continuous time parameter. The two variables continuously mix followin...

In this work we investigate the variation of the online kernelized ridge regression algorithm in the setting of $d-$dimensional adversarial nonparametric regression. We derive the regret upper bound...

Online forecasting under a changing environment has been a problem of increasing importance in many real-world applications. In this paper, we consider the meta-algorithm presented in \citet{zhang20...

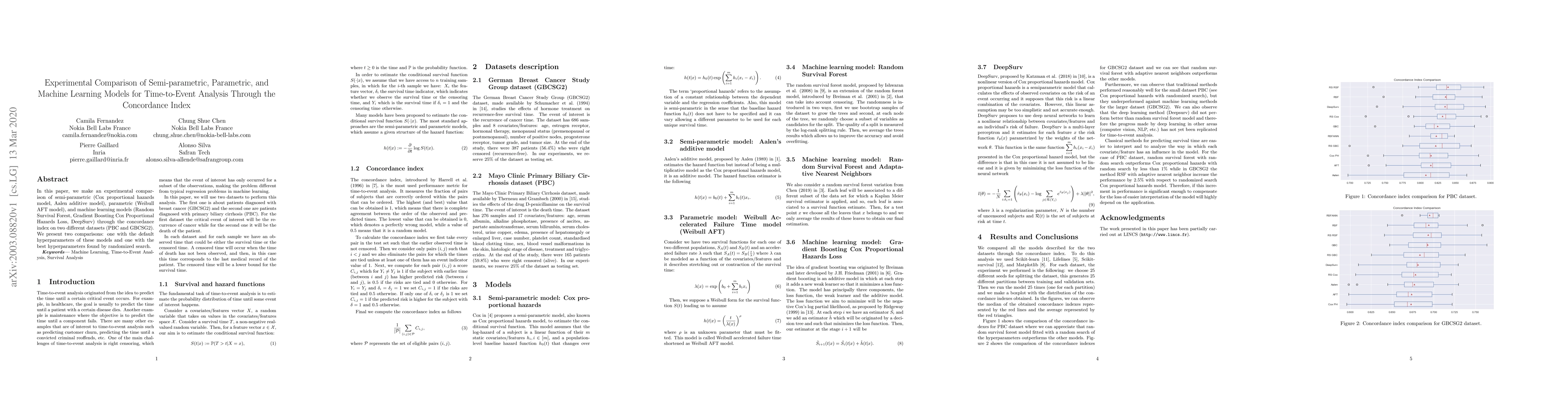

In this paper, we make an experimental comparison of semi-parametric (Cox proportional hazards model, Aalen's additive regression model), parametric (Weibull AFT model), and machine learning models ...

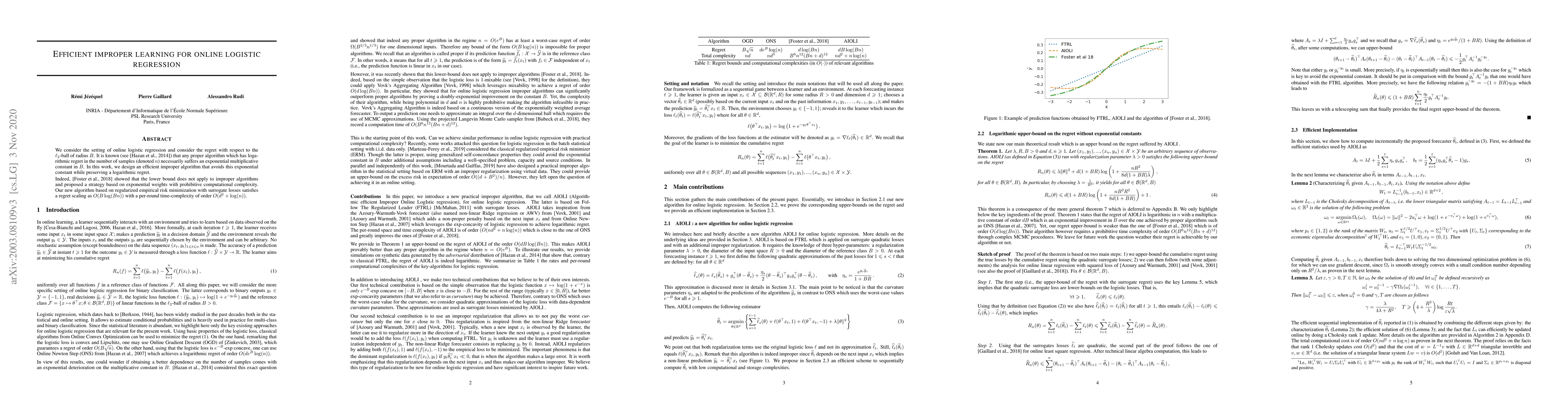

We consider the setting of online logistic regression and consider the regret with respect to the 2-ball of radius B. It is known (see [Hazan et al., 2014]) that any proper algorithm which has logar...

We study boosting for adversarial online nonparametric regression with general convex losses. We first introduce a parameter-free online gradient boosting (OGB) algorithm and show that its application...

We address the online unconstrained submodular maximization problem (Online USM), in a setting with stochastic bandit feedback. In this framework, a decision-maker receives noisy rewards from a nonmon...

We study online adversarial regression with convex losses against a rich class of continuous yet highly irregular prediction rules, modeled by Besov spaces $B_{pq}^s$ with general parameters $1 \leq p...

We study online learning in episodic finite-horizon Markov decision processes (MDPs) with convex objective functions, known as the concave utility reinforcement learning (CURL) problem. This setting g...

This work studies and develop projection-free algorithms for online learning with linear optimization oracles (a.k.a. Frank-Wolfe) for handling the constraint set. More precisely, this work (i) provid...

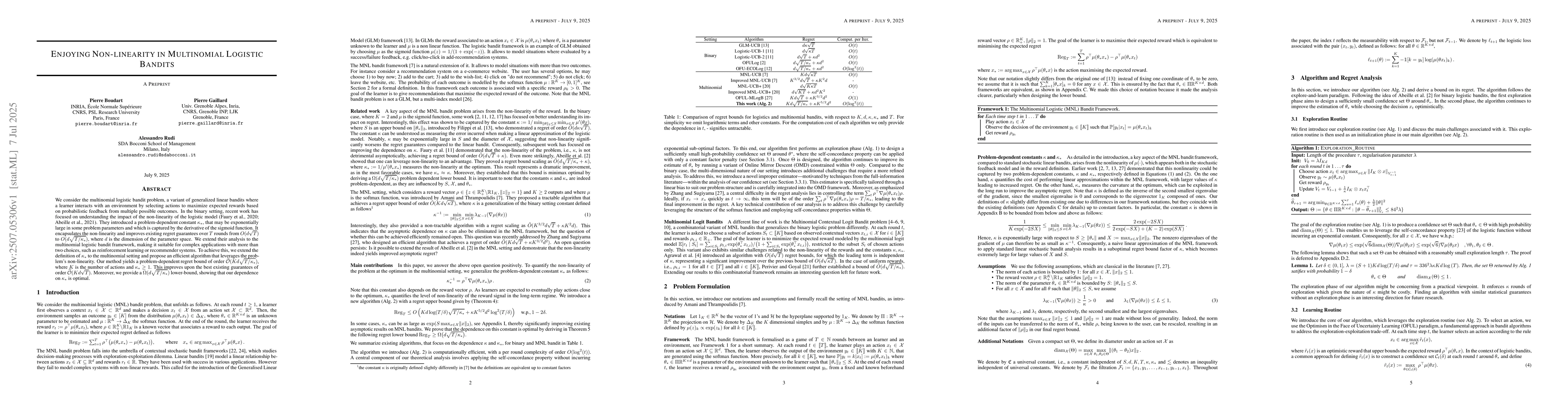

We consider the multinomial logistic bandit problem, a variant of generalized linear bandits where a learner interacts with an environment by selecting actions to maximize expected rewards based on pr...

Traditional reinforcement learning usually assumes either episodic interactions with resets or continuous operation to minimize average or cumulative loss. While episodic settings have many theoretica...

We study nonparametric regression over Besov spaces from noisy observations under sub-exponential noise, aiming to achieve minimax-optimal guarantees on the integrated squared error that hold with hig...

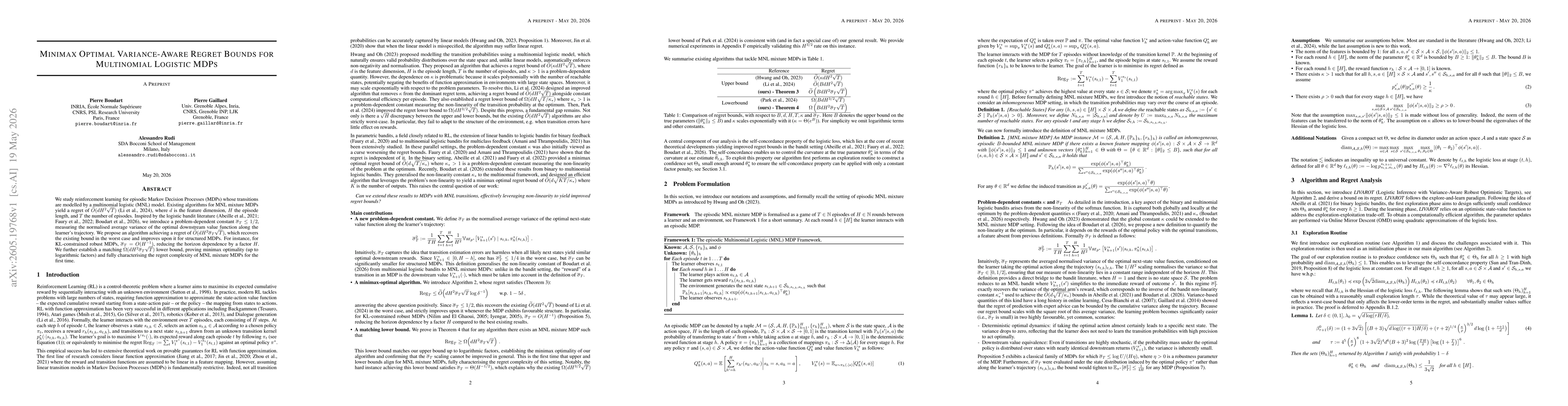

We study reinforcement learning for episodic Markov Decision Processes (MDPs) whose transitions are modelled by a multinomial logistic (MNL) model. Existing algorithms for MNL mixture MDPs yield a reg...

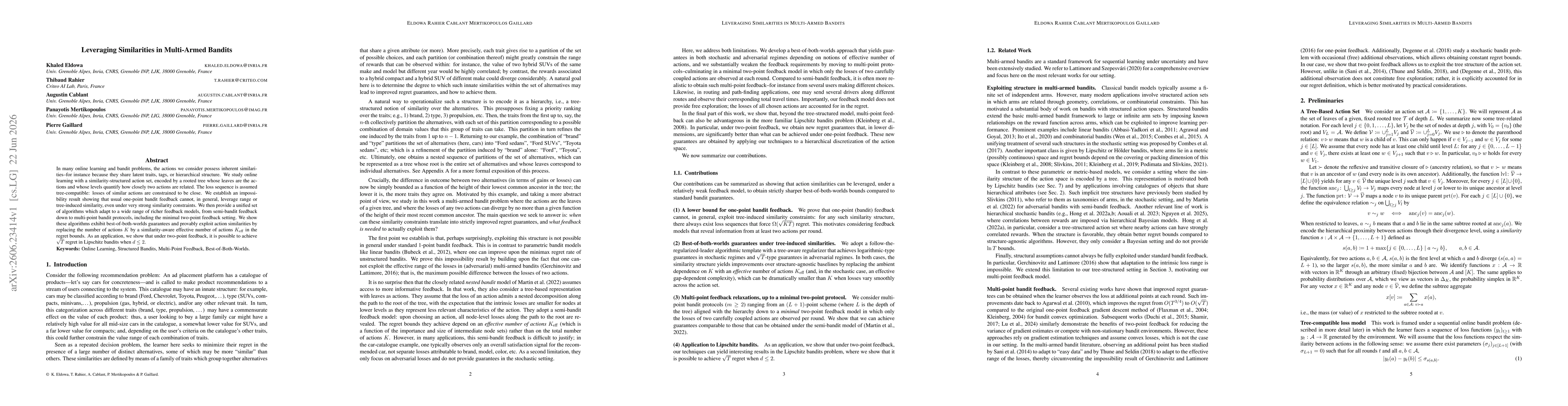

In many online learning and bandit problems, the actions we consider possess inherent similarities--for instance because they share latent traits, tags, or hierarchical structure. We study online lear...