Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper uses topological data analysis (TDA) tools and introduces a data-driven clustering-based stock selection strategy tailored for sparse portfolio construction. Our asset selection strategy ...

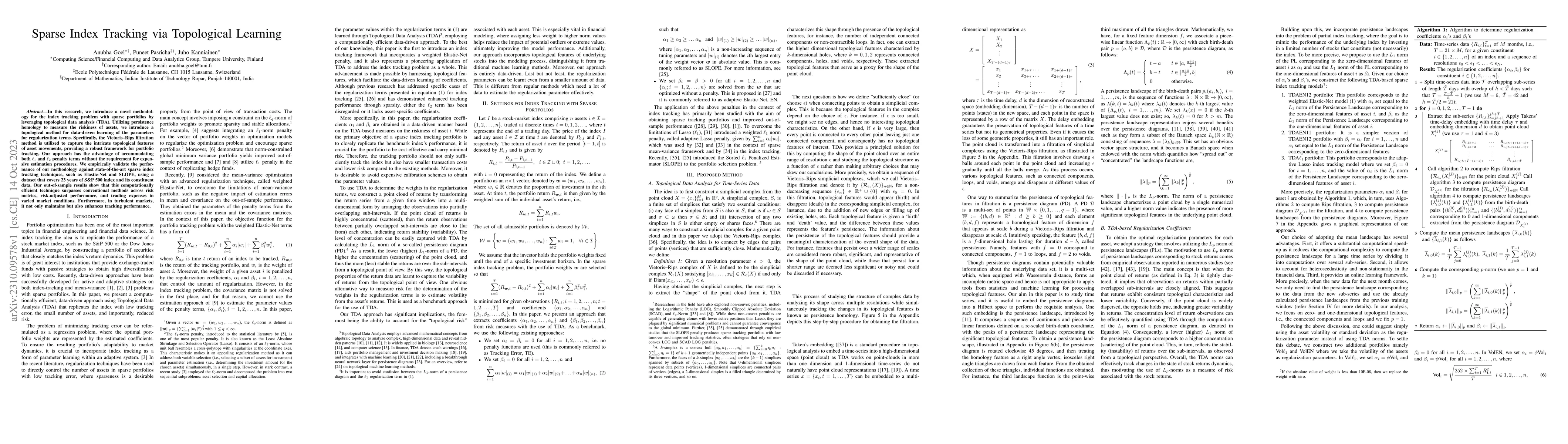

In this research, we introduce a novel methodology for the index tracking problem with sparse portfolios by leveraging topological data analysis (TDA). Utilizing persistence homology to measure the ...

We introduce an ensemble learning method based on Gaussian Process Regression (GPR) for predicting conditional expected stock returns given stock-level and macro-economic information. Our ensemble l...

The modeling of the probability of joint default or total number of defaults among the firms is one of the crucial problems to mitigate the credit risk since the default correlations significantly a...

This study is the first to explore the application of a time-series foundation model for VaR estimation. Foundation models, pre-trained on vast and varied datasets, can be used in a zero-shot setting ...

In this article, we employ physics-informed residual learning (PIRL) and propose a pricing method for European options under a regime-switching framework, where closed-form solutions are not available...

Time series foundation models (FMs) have emerged as a popular paradigm for zero-shot multi-domain forecasting. These models are trained on numerous diverse datasets and claim to be effective forecaste...