Academic Profile

Statistics

Similar Authors

Papers on arXiv

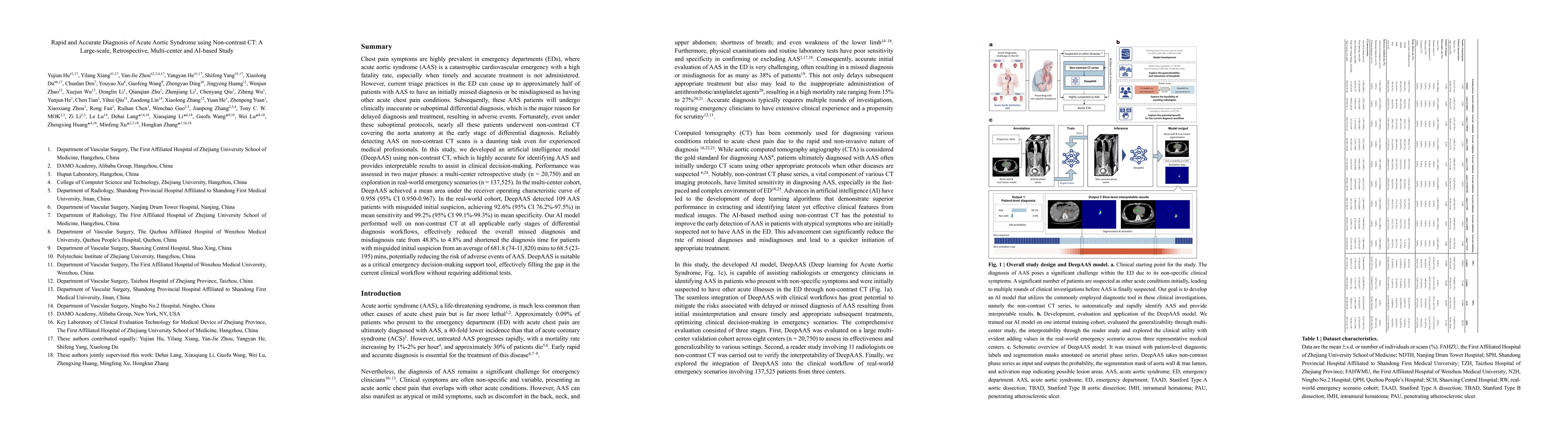

Chest pain symptoms are highly prevalent in emergency departments (EDs), where acute aortic syndrome (AAS) is a catastrophic cardiovascular emergency with a high fatality rate, especially when timely ...

This paper considers both the least squares and quasi-maximum likelihood estimation for the recently proposed scalable ARMA model, a parametric infinite-order vector AR model, and their asymptotic n...

This paper develops a flexible and computationally efficient multivariate volatility model, which allows for dynamic conditional correlations and volatility spillover effects among financial assets....

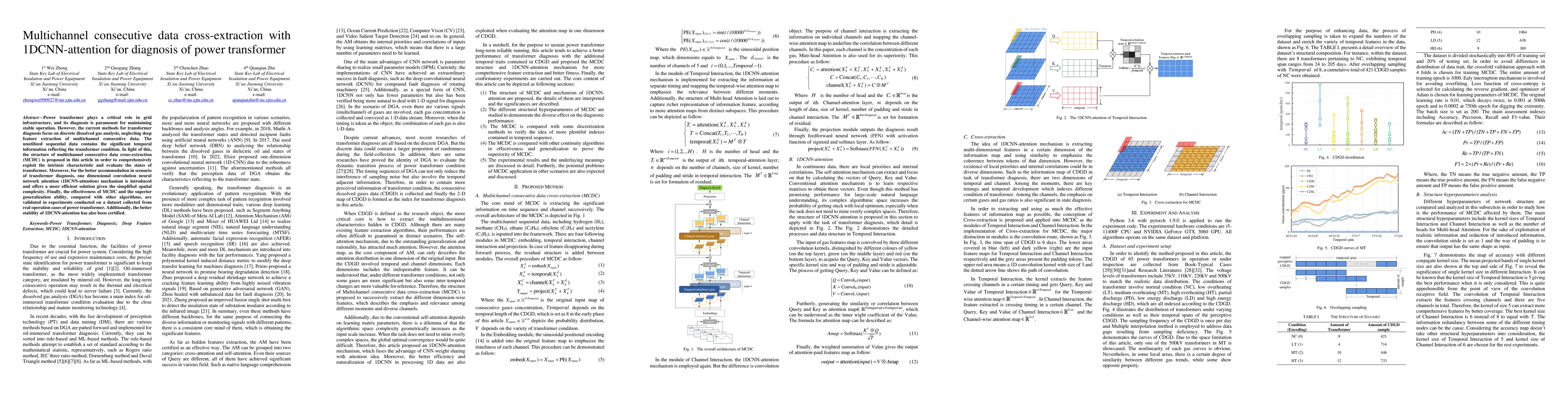

Power transformer plays a critical role in grid infrastructure, and its diagnosis is paramount for maintaining stable operation. However, the current methods for transformer diagnosis focus on discr...

This paper proposes a novel conditional heteroscedastic time series model by applying the framework of quantile regression processes to the ARCH(\infty) form of the GARCH model. This model can provi...

This paper investigates the quasi-maximum likelihood inference including estimation, model selection and diagnostic checking for linear double autoregressive (DAR) models, where all asymptotic prope...

This paper proposes the asymmetric linear double autoregression, which jointly models the conditional mean and conditional heteroscedasticity characterized by asymmetric effects. A sufficient condit...

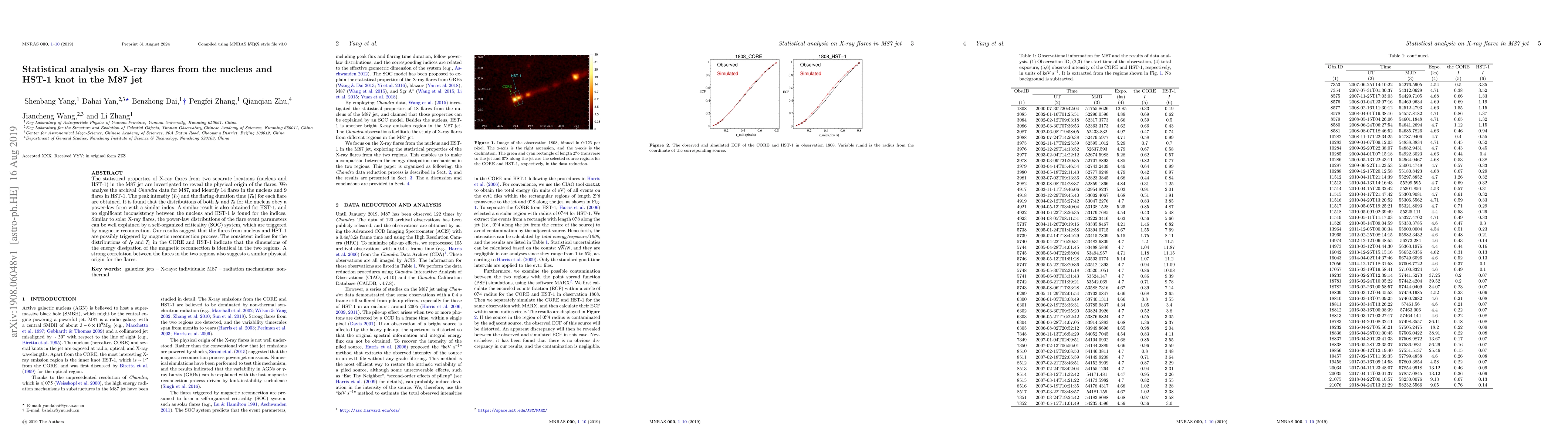

The statistical properties of X-ray flares from two separate locations (nucleus and HST-1) in the M87 jet are investigated to reveal the physical origin of the flares. We analyse the archival \texti...

Many financial time series have varying structures at different quantile levels, and also exhibit the phenomenon of conditional heteroscedasticity at the same time. In the meanwhile, it is still lac...

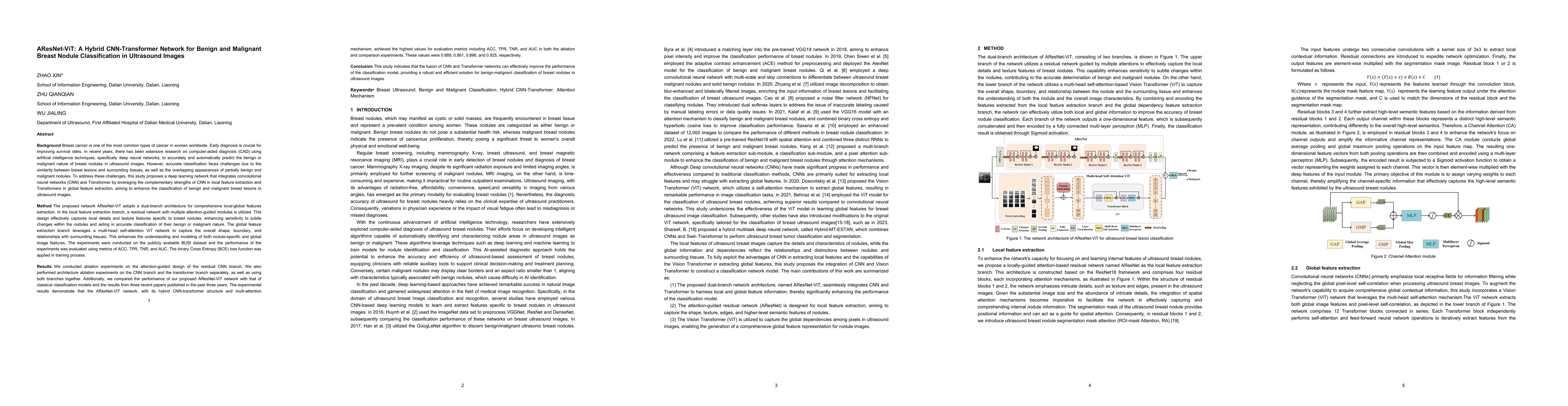

To address the challenges of similarity between lesions and surrounding tissues, overlapping appearances of partially benign and malignant nodules, and difficulty in classification, a deep learning ne...

This paper introduces a robust and computationally efficient estimation framework for high-dimensional volatility models in the BEKK-ARCH class. The proposed approach employs data truncation to ensure...

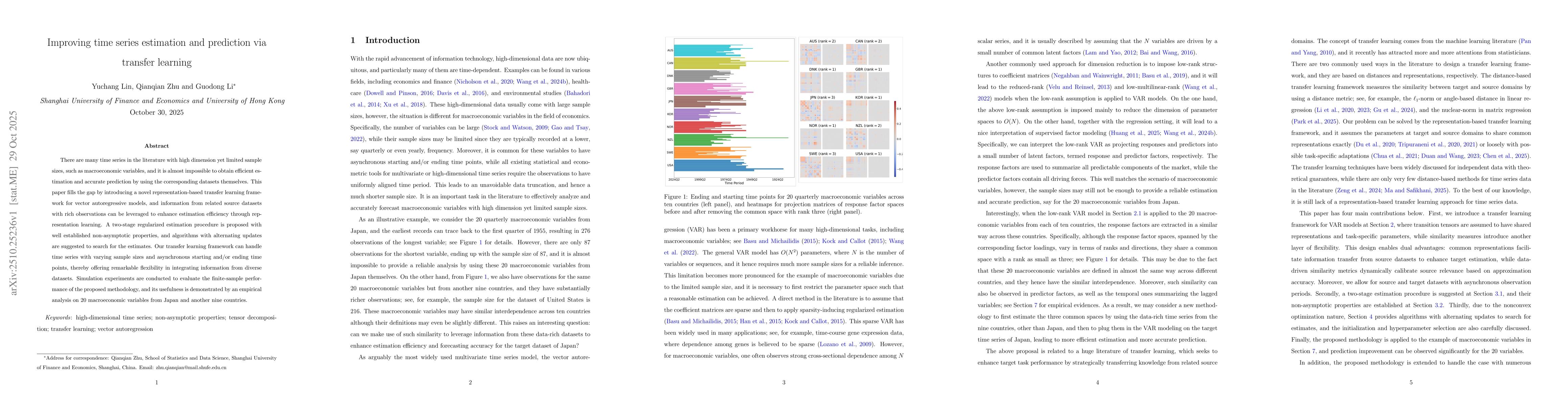

There are many time series in the literature with high dimension yet limited sample sizes, such as macroeconomic variables, and it is almost impossible to obtain efficient estimation and accurate pred...

In the era of big data, leveraging information from multiple clients while preserving data privacy has emerged as a critical challenge in modern statistical modeling and forecasting. This paper introd...