Academic Profile

Statistics

Similar Authors

Papers on arXiv

Financial market risk forecasting involves applying mathematical models, historical data analysis and statistical methods to estimate the impact of future market movements on investments. This proce...

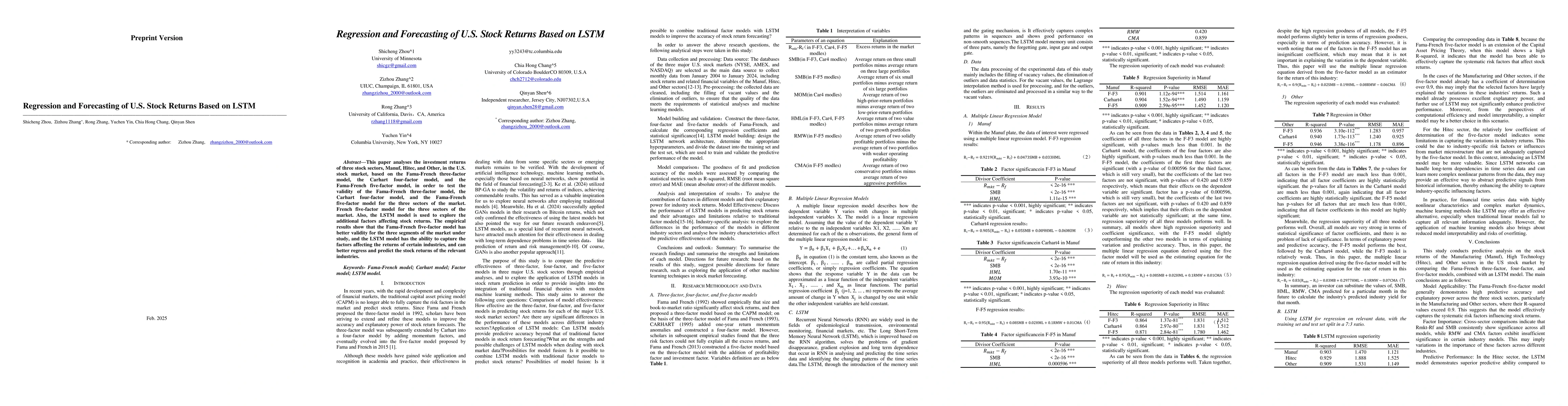

This paper analyses the investment returns of three stock sectors, Manuf, Hitec, and Other, in the U.S. stock market, based on the Fama-French three-factor model, the Carhart four-factor model, and th...

We develop methodology for valid inference after variable selection in logistic regression when the responses are partially observed, that is, when one observes a set of error-prone testing outcomes i...

Small and Medium-sized Enterprises (SMEs) are vital to the modern economy, yet their credit risk analysis often struggles with scarce data, especially for online lenders lacking direct credit records....

We propose a unified framework to draw inferences for regression coefficients in a generalized linear model (GLM) following Lasso-based variable selection. We adapt to non-Gaussian GLMs a recently dev...