Academic Profile

Statistics

Papers on arXiv

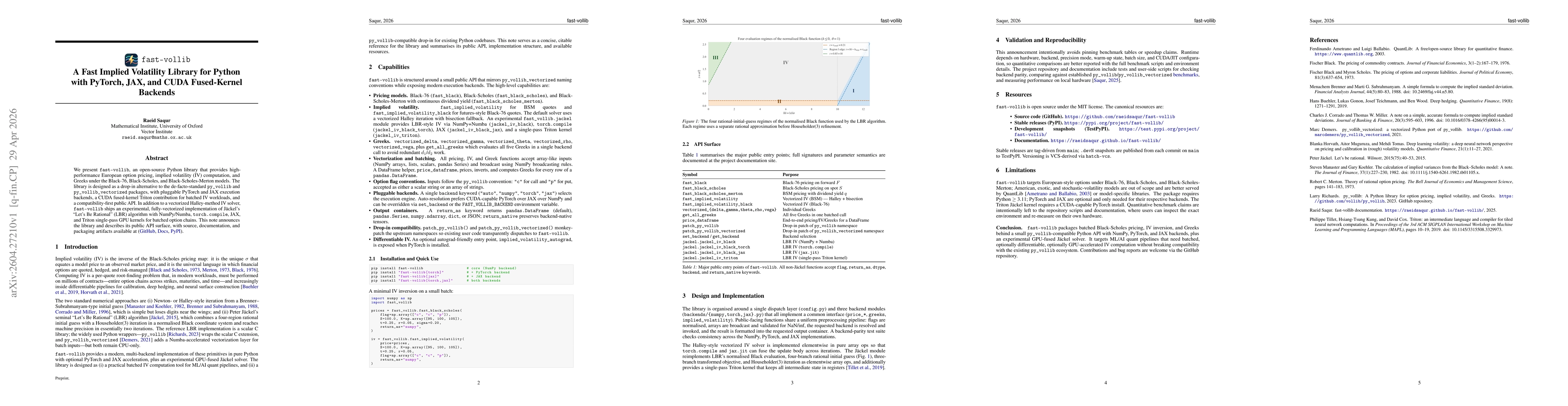

Machine learning techniques applied to the problem of financial market forecasting struggle with dynamic regime switching, or underlying correlation and covariance shifts in true (hidden) market varia...

We propose MoE-F -- a formalised mechanism for combining $N$ pre-trained expert Large Language Models (LLMs) in online time-series prediction tasks by adaptively forecasting the best weighting of LL...

One of the inherent challenges in deploying transformers on time series is that \emph{reality only happens once}; namely, one typically only has access to a single trajectory of the data-generating ...

We introduce and make publicly available the NIFTY Financial News Headlines dataset, designed to facilitate and advance research in financial market forecasting using large language models (LLMs). T...

The quantitative analysis of political ideological positions is a difficult task. In the past, various literature focused on parliamentary voting data of politicians, party manifestos and parliament...

The quest for human imitative AI has been an enduring topic in AI research since its inception. The technical evolution and emerging capabilities of the latest cohort of large language models (LLMs)...

The Inverse Reinforcement Learning (\textit{IRL}) problem has seen rapid evolution in the past few years, with important applications in domains like robotics, cognition, and health. In this work, w...

Here we discuss the four key principles of bio-medical ethics from surgical context. We elaborate on the definition of 'fairness' and its implications in AI system design, with taxonomy of algorithm...

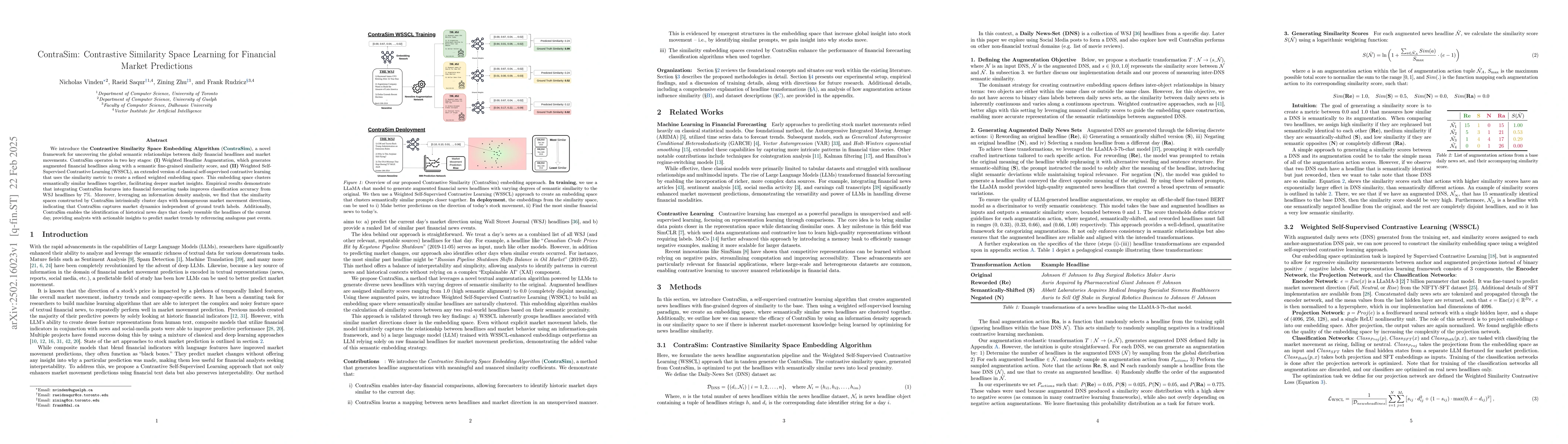

We introduce the Contrastive Similarity Space Embedding Algorithm (ContraSim), a novel framework for uncovering the global semantic relationships between daily financial headlines and market movements...

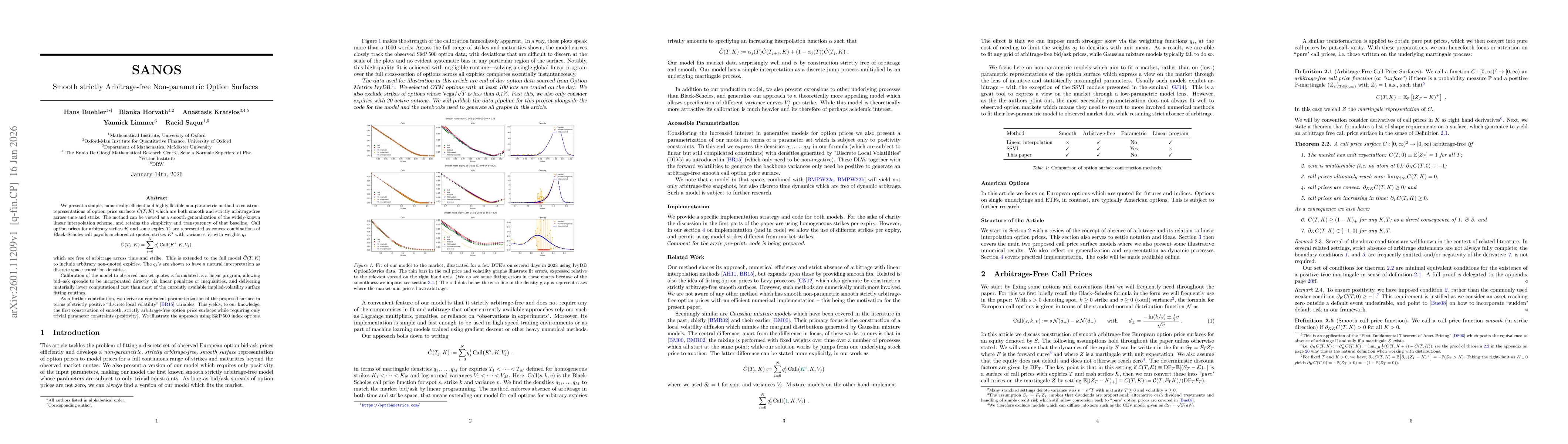

We present a simple, numerically efficient but highly flexible non-parametric method to construct representations of option price surfaces which are both smooth and strictly arbitrage-free across time...

We argue that the current practice of evaluating AI/ML time-series forecasting models, predominantly on benchmarks characterized by strong, persistent periodicities and seasonalities, obscures real pr...

We present fast-vollib, an open-source Python library that provides high-performance European option pricing, implied volatility (IV) computation, and Greeks under the Black-76, Black-Scholes, and Bla...

Recent work on the sequence universality of State Space Models (SSMs) has introduced efficient, maximally expressive continuous-time approaches for time-series modelling. While these works focus on di...

Modern option-learning systems operate in two coordinates: price space, where markets quote and no-arbitrage constraints are most naturally enforced, and implied volatility (IV) space, where volatilit...