1

arXiv Papers

6

Total Publications

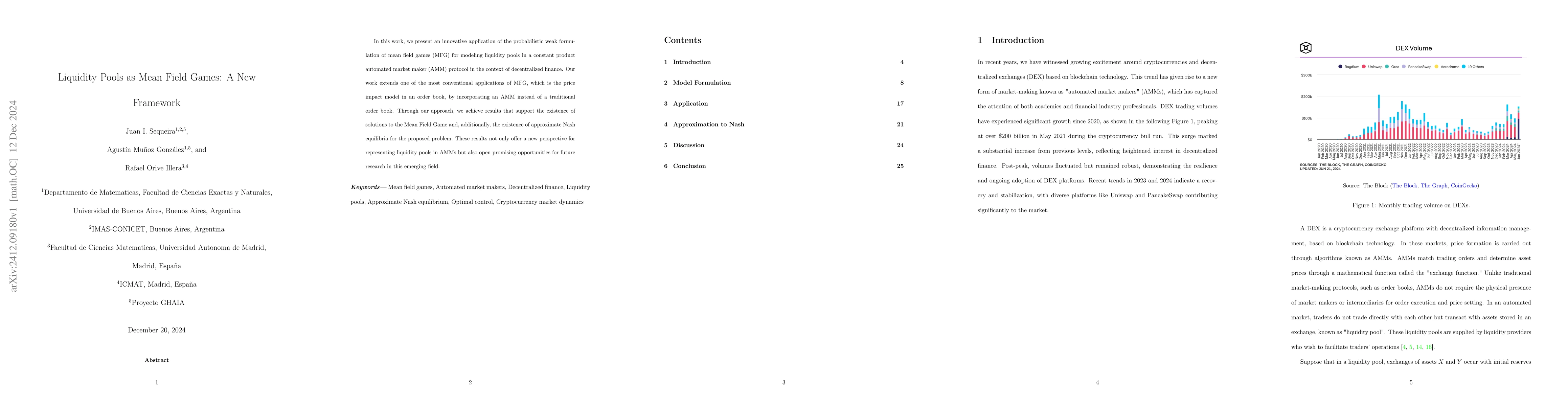

Profile

Academic Profile

Metrics

Statistics

1

arXiv Papers

6

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Liquidity Pools as Mean Field Games: A New Framework

In this work, we present an innovative application of the probabilistic weak formulation of mean field games (MFG) for modeling liquidity pools in a constant product automated market maker (AMM) proto...