Publication

Metrics

AI Quick Summary

This paper introduces a probabilistic mean field game (MFG) framework to model liquidity pools in decentralized finance's constant product automated market makers (AMMs), extending conventional MFG applications from order books to AMMs, and demonstrates the existence of solutions and approximate Nash equilibria.

Paper Preview

Abstract

In this work, we present an innovative application of the probabilistic weak formulation of mean field games (MFG) for modeling liquidity pools in a constant product automated market maker (AMM) protocol in the context of decentralized finance. Our work extends one of the most conventional applications of MFG, which is the price impact model in an order book, by incorporating an AMM instead of a traditional order book. Through our approach, we achieve results that support the existence of solutions to the Mean Field Game and, additionally, the existence of approximate Nash equilibria for the proposed problem. These results not only offer a new perspective for representing liquidity pools in AMMs but also open promising opportunities for future research in this emerging field.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Paper Details

Authors

PDF Preview

Related Papers

No references found for this paper.

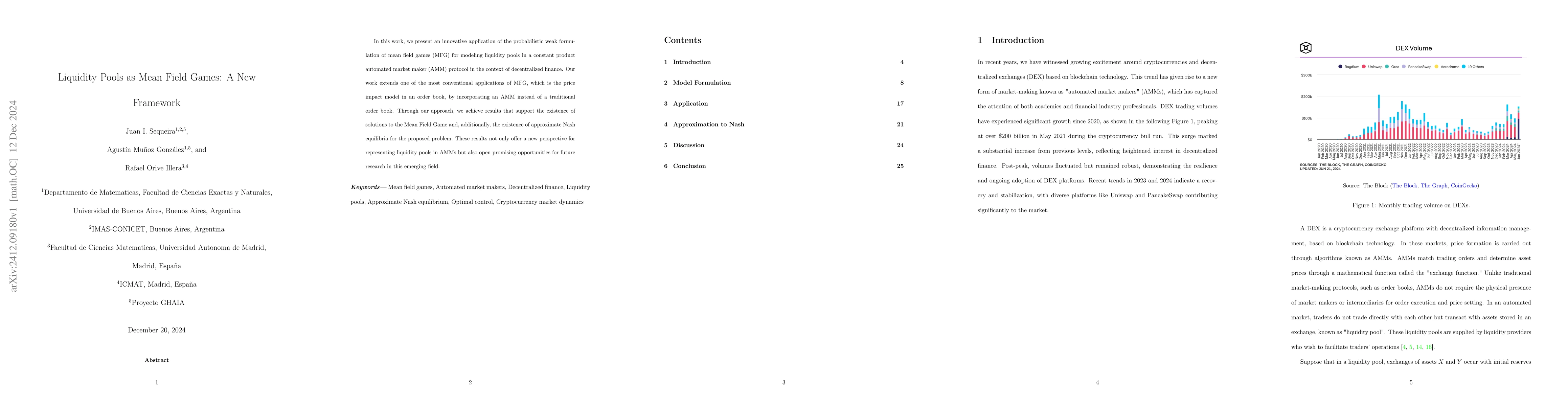

Discussion 0