Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this work, we present an innovative application of the probabilistic weak formulation of mean field games (MFG) for modeling liquidity pools in a constant product automated market maker (AMM) proto...

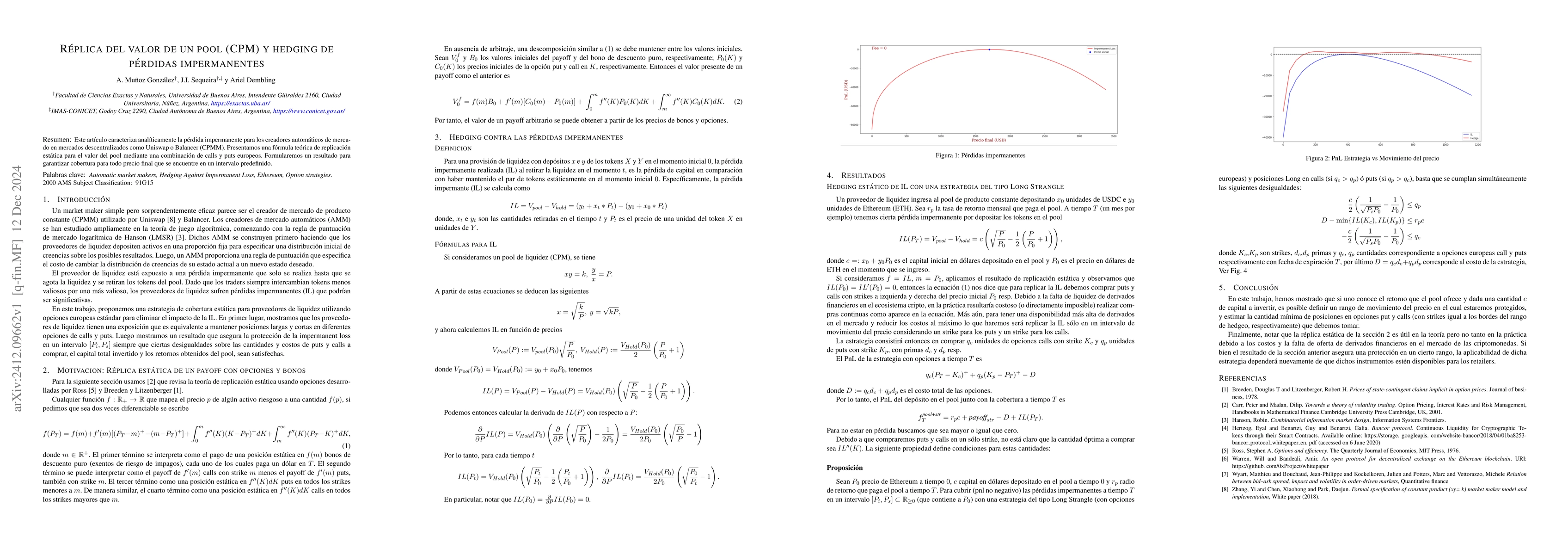

This article analytically characterizes the impermanent loss for automatic market makers in decentralized exchanges such as Uniswap or Balancer (CPMM). We present a theoretical static replication form...

This work extends the theory presented in Mean Field Games with a Dominating Player by Bensoussan, Chau and Yam on mean field games with a dominating player, to the case in which the utility and cost ...

This paper extends the theoretical framework introduced in Liquidity Pools as Mean Field Games: A New Framework, where the interactions among traders in a constant product market-making protocol were ...

This work builds on the theoretical frameworks presented in "Liquidity pools as mean field games: A new framework" and "Liquidity pools as mean field games with transaction costs" by the same author, ...