Academic Profile

Statistics

Similar Authors

Papers on arXiv

Efficiently pricing multi-asset options poses a significant challenge in quantitative finance. The Monte Carlo (MC) method remains the prevalent choice for pricing engines; however, its slow converg...

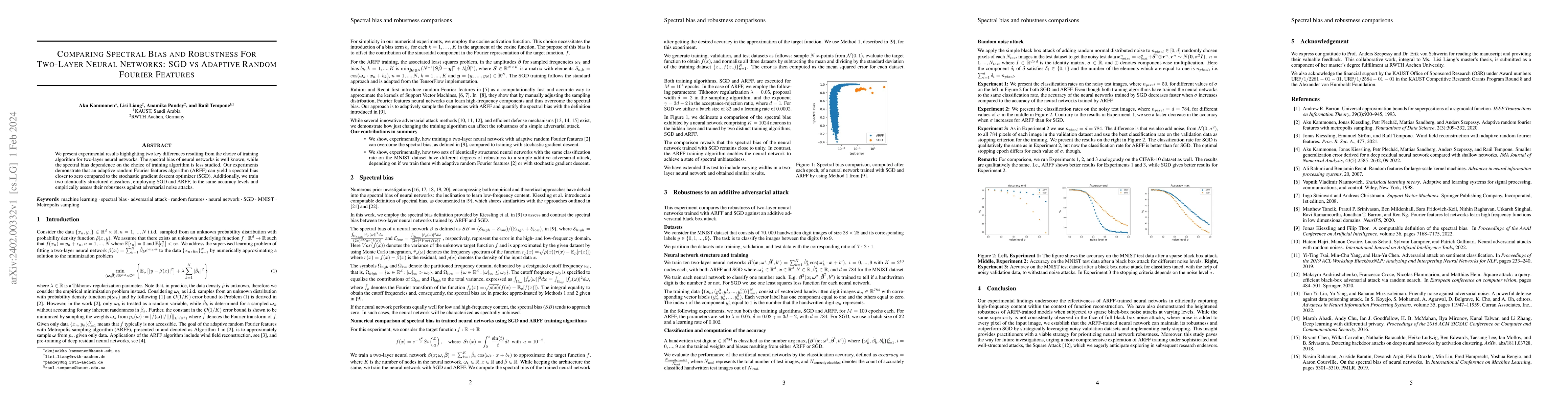

We present experimental results highlighting two key differences resulting from the choice of training algorithm for two-layer neural networks. The spectral bias of neural networks is well known, wh...

This work considers a short-term, continuous time setting characterized by a coupled power supply system controlled exclusively by a single provider and comprising a cascade of hydropower systems (d...

This study analyzes the nonasymptotic convergence behavior of the quasi-Monte Carlo (QMC) method with applications to linear elliptic partial differential equations (PDEs) with lognormal coefficient...

Finding the optimal design of experiments in the Bayesian setting typically requires estimation and optimization of the expected information gain functional. This functional consists of one outer an...

This work introduces a novel approach that combines the multi-index Monte Carlo (MC) method with importance sampling (IS) to estimate rare event quantities expressed as an expectation of a smooth ob...

We address the computational efficiency in solving the A-optimal Bayesian design of experiments problems for which the observational map is based on partial differential equations and, consequently,...

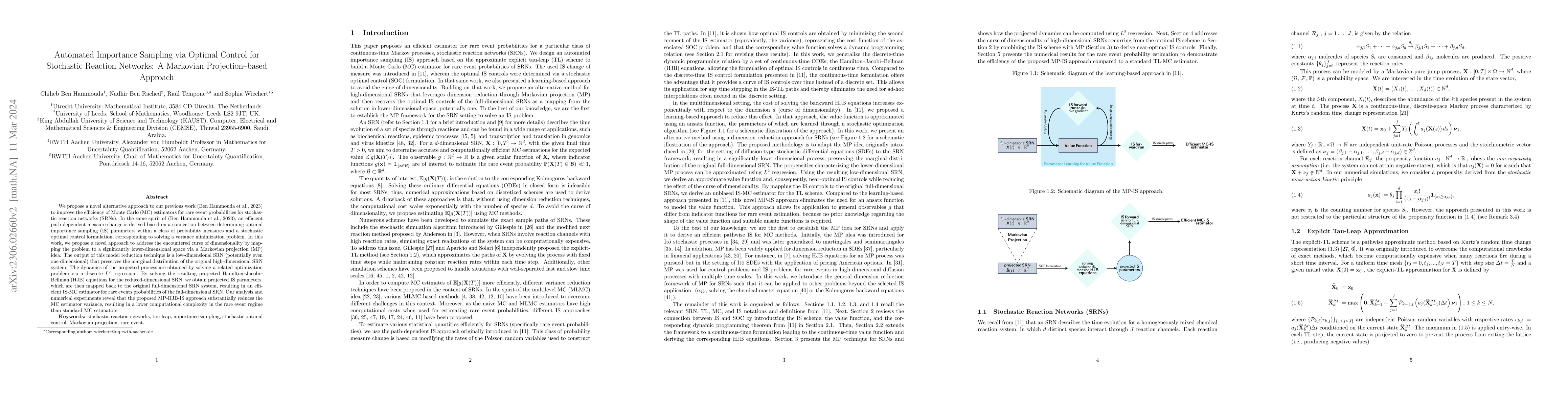

We propose a novel alternative approach to our previous work (Ben Hammouda et al., 2023) to improve the efficiency of Monte Carlo (MC) estimators for rare event probabilities for stochastic reaction...

Characterized by an outer integral connected to an inner integral through a nonlinear function, nested integration is a challenging problem in various fields, such as engineering and mathematical fi...

In this work, we extend the data-driven It\^{o} stochastic differential equation (SDE) framework for the pathwise assessment of short-term forecast errors to account for the time-dependent upper bou...

This work combines multilevel Monte Carlo (MLMC) with importance sampling to estimate rare-event quantities that can be expressed as the expectation of a Lipschitz observable of the solution to a br...

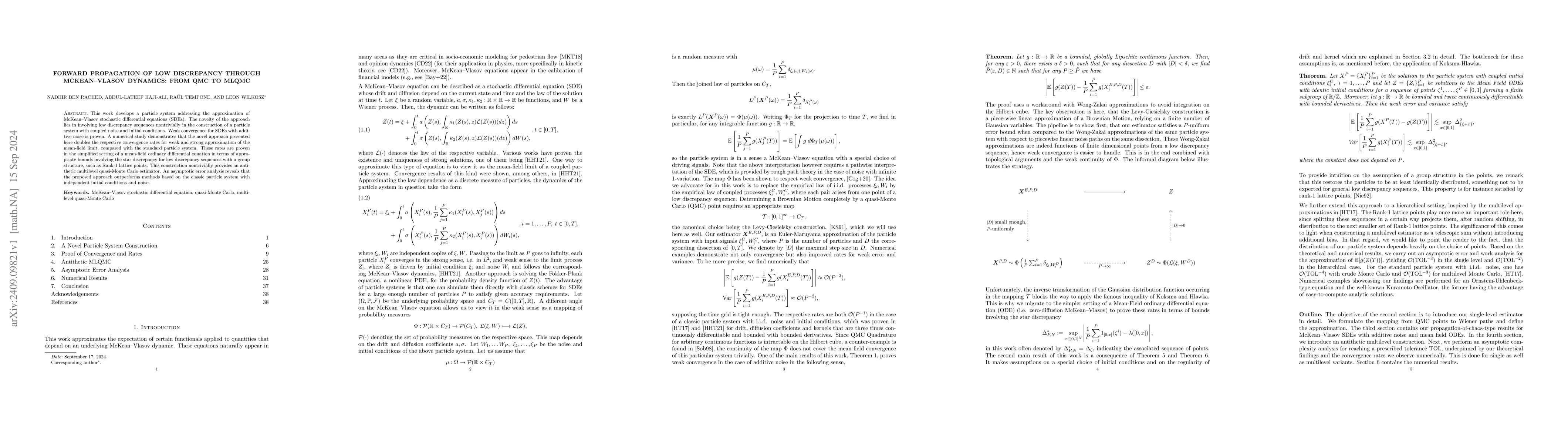

This paper investigates Monte Carlo (MC) methods to estimate probabilities of rare events associated with solutions to the $d$-dimensional McKean-Vlasov stochastic differential equation (MV-SDE). MV...

We present an adaptive multilevel Monte Carlo (AMLMC) algorithm for approximating deterministic, real-valued, bounded linear functionals that depend on the solution of a linear elliptic PDE with a l...

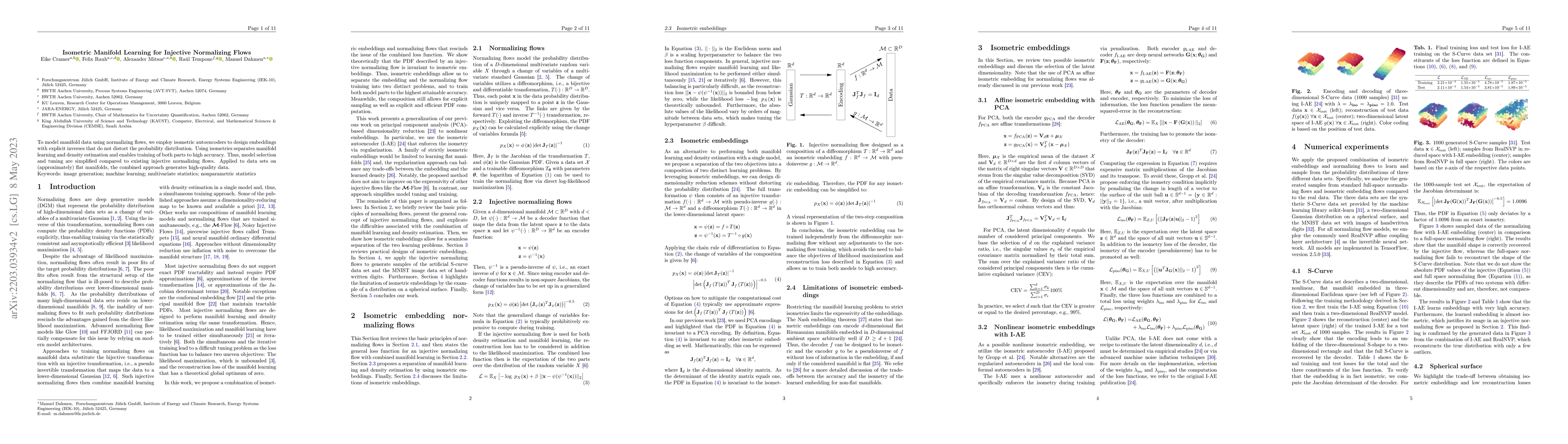

To model manifold data using normalizing flows, we employ isometric autoencoders to design embeddings with explicit inverses that do not distort the probability distribution. Using isometries separa...

Estimating the expectations of functionals applied to sums of random variables (RVs) is a well-known problem encountered in many challenging applications. Generally, closed-form expressions of these...

Calculating the expected information gain in optimal Bayesian experimental design typically relies on nested Monte Carlo sampling. When the model also contains nuisance parameters, which are paramet...

When approximating the expectations of a functional of a solution to a stochastic differential equation, the numerical performance of deterministic quadrature methods, such as sparse grid quadrature...

We explore efficient estimation of statistical quantities, particularly rare event probabilities, for stochastic reaction networks. Consequently, we propose an importance sampling (IS) approach to i...

In this study, we demonstrate that the norm test and inner product/orthogonality test presented in \cite{Bol18} are equivalent in terms of the convergence rates associated with Stochastic Gradient D...

This paper presents the machine learning-based ensemble conditional mean filter (ML-EnCMF) -- a filtering method based on the conditional mean filter (CMF) previously introduced in the literature. T...

In this work we combine ideas from multi-index Monte Carlo and ensemble Kalman filtering (EnKF) to produce a highly efficient filtering method called multi-index EnKF (MIEnKF). MIEnKF is based ...

We investigate the use of spatial interpolation methods for reconstructing the horizontal near-surface wind field given a sparse set of measurements. In particular, random Fourier features is compar...

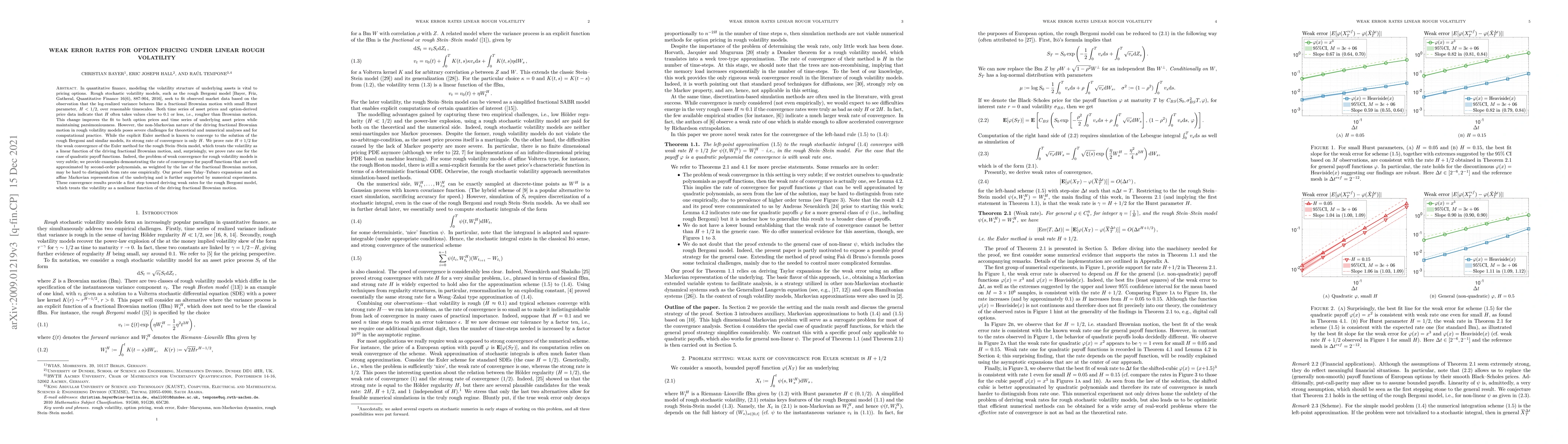

In quantitative finance, modeling the volatility structure of underlying assets is vital to pricing options. Rough stochastic volatility models, such as the rough Bergomi model [Bayer, Friz, Gathera...

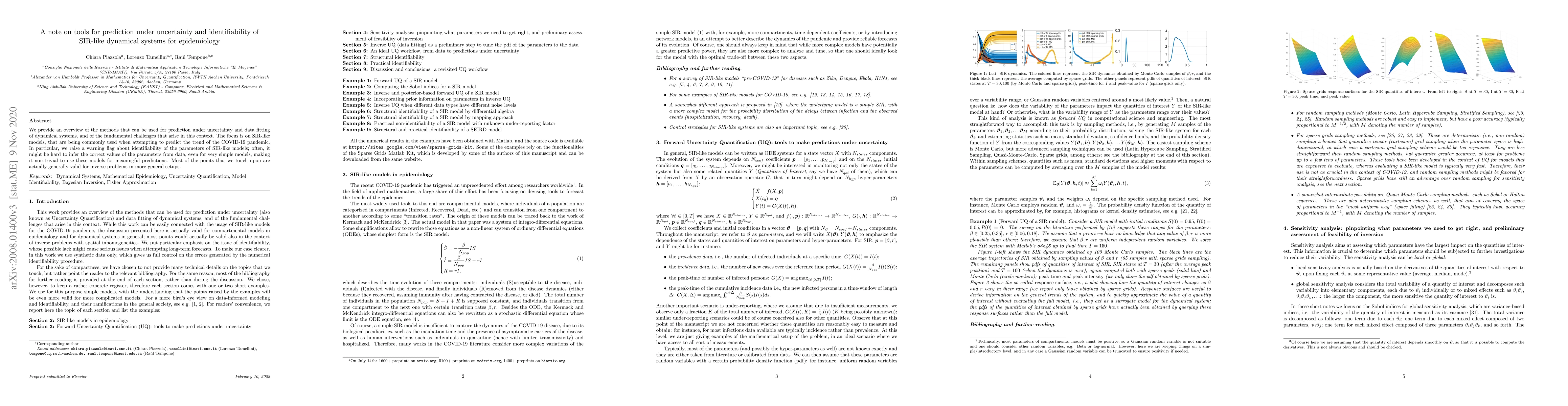

We provide an overview of the methods that can be used for prediction under uncertainty and data fitting of dynamical systems, and of the fundamental challenges that arise in this context. The focus...

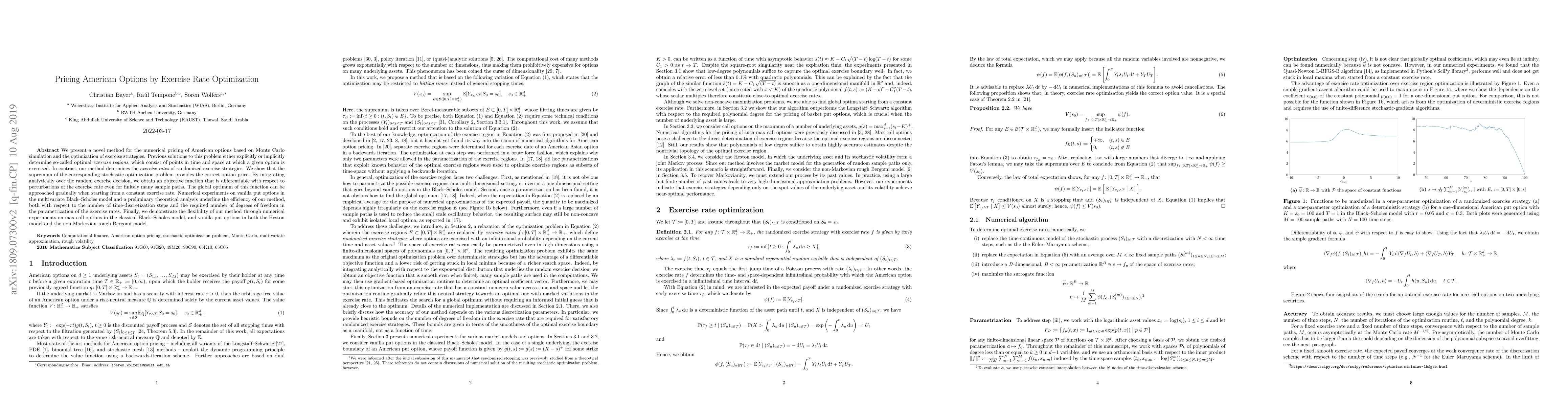

We present a novel method for the numerical pricing of American options based on Monte Carlo simulation and the optimization of exercise strategies. Previous solutions to this problem either explici...

This paper presents an enhanced adaptive random Fourier features (ARFF) training algorithm for shallow neural networks, building upon the work introduced in "Adaptive Random Fourier Features with Metr...

Nested integration problems arise in various scientific and engineering applications, including Bayesian experimental design, financial risk assessment, and uncertainty quantification. These nested in...

This work develops a particle system addressing the approximation of McKean-Vlasov stochastic differential equations (SDEs). The novelty of the approach lies in involving low discrepancy sequences non...

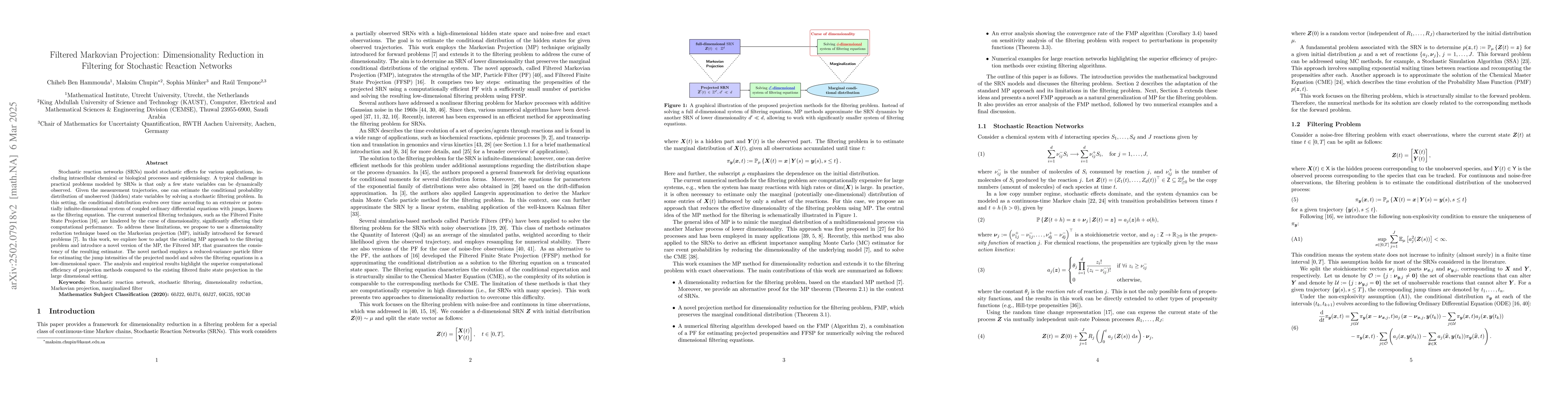

Stochastic reaction networks (SRNs) model stochastic effects for various applications, including intracellular chemical or biological processes and epidemiology. A typical challenge in practical probl...

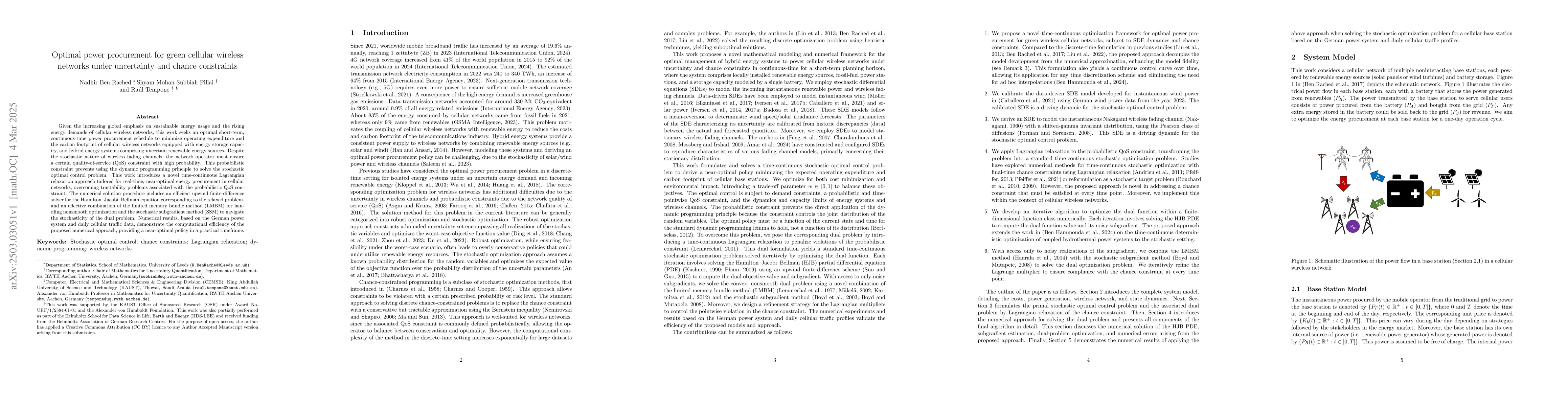

Given the increasing global emphasis on sustainable energy usage and the rising energy demands of cellular wireless networks, this work seeks an optimal short-term, continuous-time power procurement s...

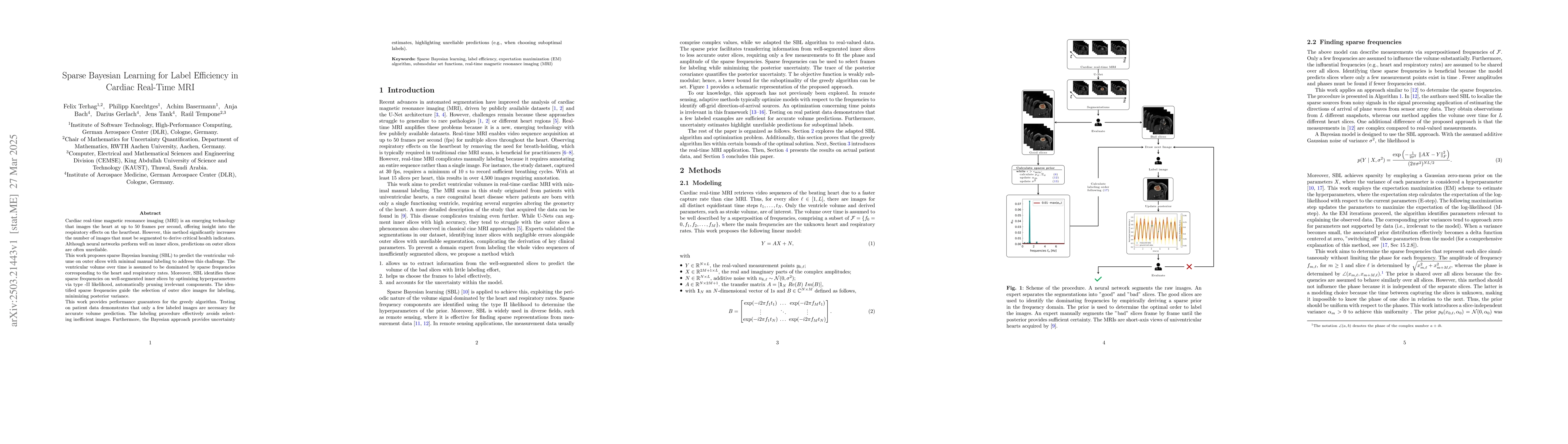

Cardiac real-time magnetic resonance imaging (MRI) is an emerging technology that images the heart at up to 50 frames per second, offering insight into the respiratory effects on the heartbeat. Howeve...

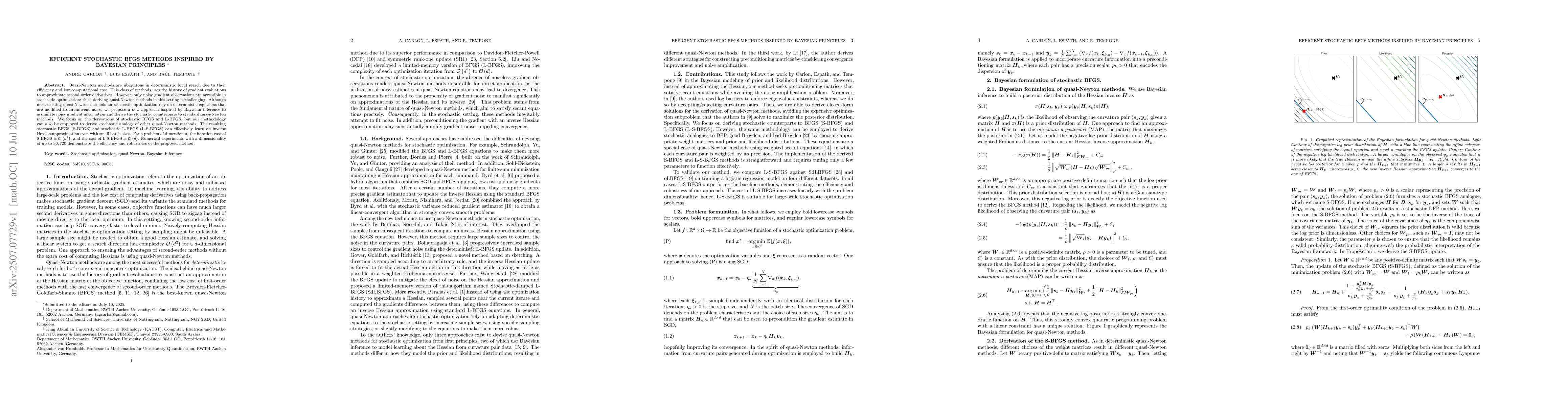

Quasi-Newton methods are ubiquitous in deterministic local search due to their efficiency and low computational cost. This class of methods uses the history of gradient evaluations to approximate seco...

This work proposes a training algorithm based on adaptive random Fourier features (ARFF) with Metropolis sampling and resampling \cite{kammonen2024adaptiverandomfourierfeatures} for learning drift and...

The efficient approximation of quantity of interest derived from PDEs with lognormal diffusivity is a central challenge in uncertainty quantification. In this study, we propose a multilevel quasi-Mont...

The machine learning random Fourier feature method for data in high dimension is computationally and theoretically attractive since the optimization is based on a convex standard least squares problem...

We propose a novel deterministic purification method to improve adversarial robustness by mapping a potentially adversarial sample toward a nearby sample that lies close to a mode of the data distribu...

This paper proposes a new randomized design of digital nets in which the generating matrices are chosen to be random Hankel matrices. Compared with previous randomized designs of digital nets, this ap...

The rapid growth of weather-dependent renewable generation increases price volatility and imbalance penalty risk in power markets, creating the need for advanced quantitative trading strategies. We de...

We present a Pontryagin-based numerical solver for deterministic optimal control problems in Bolza form. The solver regularizes the generally nonsmooth Hamiltonian using a log-sum-exp smoothing of a c...