Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper we provide an exhaustive survey of the current state of the mathematics of filtration enlargement and an interpretation of the key results of the literature from the viewpoint of mathe...

The purpose of this paper is to test the time-invariance of the beta coefficients estimated by the Adaptive Multi-Factor (AMF) model. The AMF model is implied by the generalized arbitrage pricing th...

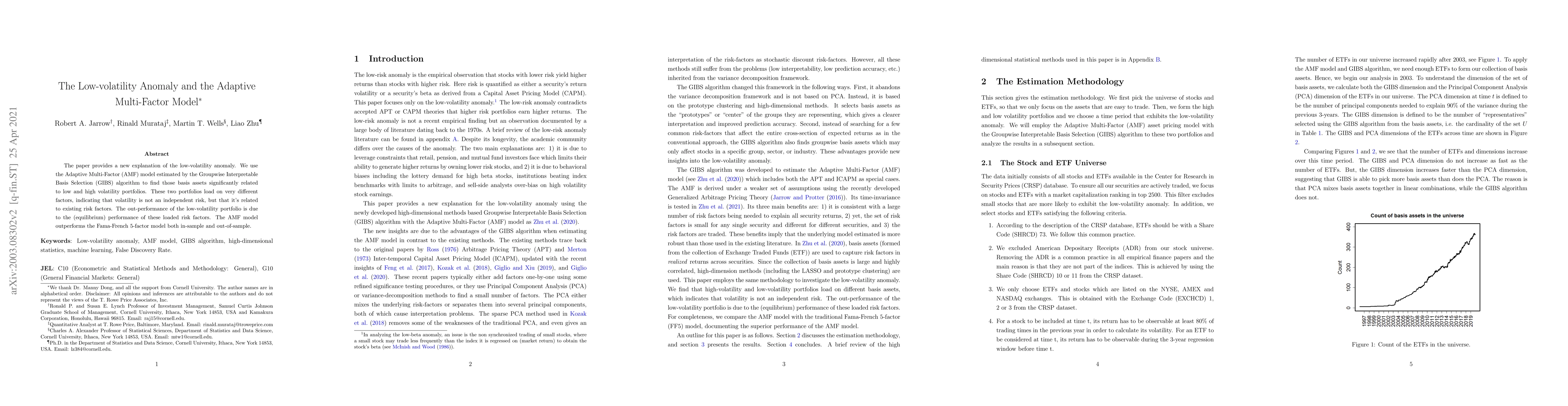

The paper provides a new explanation of the low-volatility anomaly. We use the Adaptive Multi-Factor (AMF) model estimated by the Groupwise Interpretable Basis Selection (GIBS) algorithm to find tho...

The paper proposes a new algorithm for the high-dimensional financial data -- the Groupwise Interpretable Basis Selection (GIBS) algorithm, to estimate a new Adaptive Multi-Factor (AMF) asset pricin...

We develop a unified modeling framework that connects two distinct types of bubbles defined in the literature: the rational bubbles (aka P-bubbles), and the local martingale bubbles (aka Q-bubbles). W...