Academic Profile

Statistics

Similar Authors

Papers on arXiv

The scope for the accurate calculation of the Loss Given Default (LGD) parameter is comprehensive in terms of financial data. In this research, we aim to explore methods for improving the approximatio...

This study focuses on building an algorithmic investment strategy employing a hybrid approach that combines LSTM and ARIMA models referred to as LSTM-ARIMA. This unique algorithm uses LSTM to produc...

The study seeks to develop an effective strategy based on the novel framework of statistical arbitrage based on graph clustering algorithms. Amalgamation of quantitative and machine learning methods...

This paper proposes a novel approach to hedging portfolios of risky assets when financial markets are affected by financial turmoils. We introduce a completely novel approach to diversification acti...

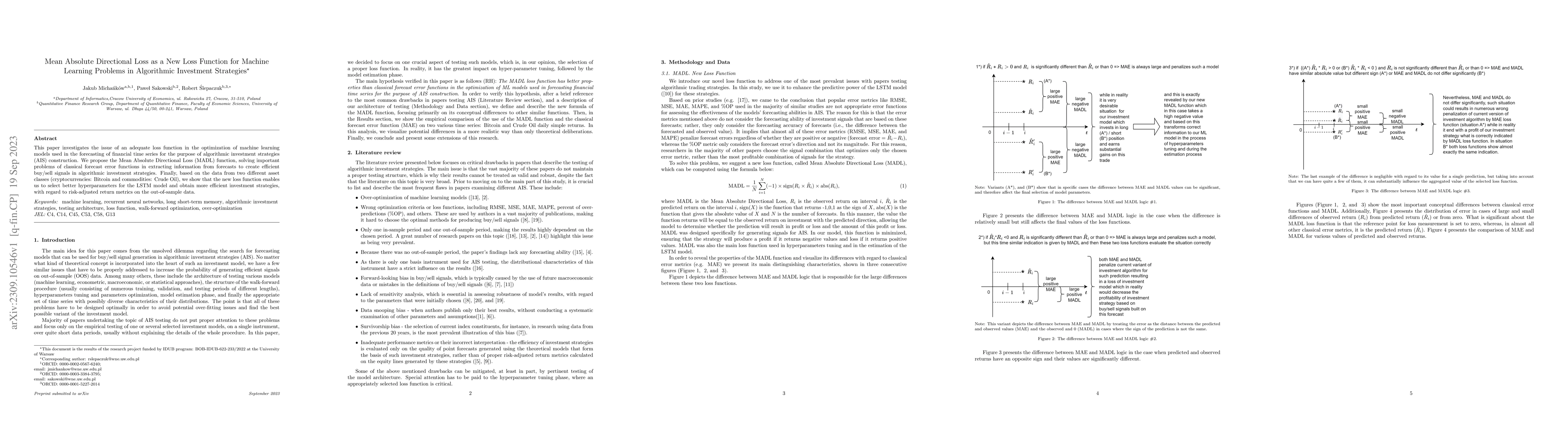

This paper investigates the issue of an adequate loss function in the optimization of machine learning models used in the forecasting of financial time series for the purpose of algorithmic investme...

We propose a new measure of systemic risk to analyze the impact of the major financial market turmoils in the stock markets from 2000 to 2023 in the USA, Europe, Brazil, and Japan. Our Implied Volat...

Predicting the S&P 500 index volatility is crucial for investors and financial analysts as it helps assess market risk and make informed investment decisions. Volatility represents the level of uncert...

This study utilizes machine learning algorithms to analyze and organize knowledge in the field of algorithmic trading. By filtering a dataset of 136 million research papers, we identified 14,342 relev...

This paper investigates the enhancement of financial time series forecasting with the use of neural networks through supervised autoencoders (SAE), to improve investment strategy performance. Using th...

This research presents a comprehensive evaluation of systematic index option-writing strategies, focusing on S&P500 index options. We compare the performance of hedging strategies using the Black-Scho...

Regardless of the selected asset class and the level of model complexity (Transformer versus LSTM versus Perceptron/RNN), the GMADL loss function produces superior results than standard MSE-type loss ...

The article investigates the usage of Informer architecture for building automated trading strategies for high frequency Bitcoin data. Three strategies using Informer model with different loss functio...

This research systematically develops and evaluates various hybrid modeling approaches by combining traditional econometric models (ARIMA and ARFIMA models) with machine learning and deep learning tec...

The proper design and architecture of testing of machine learning models, especially in their application to quantitative finance problems, is crucial. The most important in this process is selecting ...

Accurately forecasting daily exchange rate returns represents a longstanding challenge in international finance, as the exchange rate returns are driven by a multitude of correlated market factors and...

Accurate volatility forecasting is essential in banking, investment, and risk management, because expectations about future market movements directly influence current decisions. This study proposes a...

We document stable cross-asset patterns in cryptocurrency limit-order-book microstructure: the same engineered order book and trade features exhibit remarkably similar predictive importance and SHAP d...

This study introduces a novel approach to walk-forward optimization by parameterizing the lengths of training and testing windows. We demonstrate that the performance of a trading strategy using the E...

This paper investigates whether short-term market overreactions can be systematically predicted and monetized as momentum signals using high-frequency emotional information and modern machine learning...

This study develops and evaluates a deep reinforcement learning framework for dynamic portfolio allocation across global equity markets. The Soft Actor-Critic algorithm is used to learn continuous por...

This paper investigates whether machine learning forecasts of hourly BTC-USDT returns can be converted into economically meaningful trading performance after transaction costs. Using approximately 70,...

This study aims to determine whether the application of Deep Reinforcement Learning (DRL) as a specialized execution overlay can enhance pair trading in highly volatile cryptocurrency markets. Althoug...

This study investigates whether regime-dependent volatility forecasting and machine-learning-based return prediction can be jointly integrated to improve both statistical forecasting performance and e...