Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we propose a novel $K$-nearest neighbor resampling procedure for estimating the performance of a policy from historical data containing realized episodes of a decision process generat...

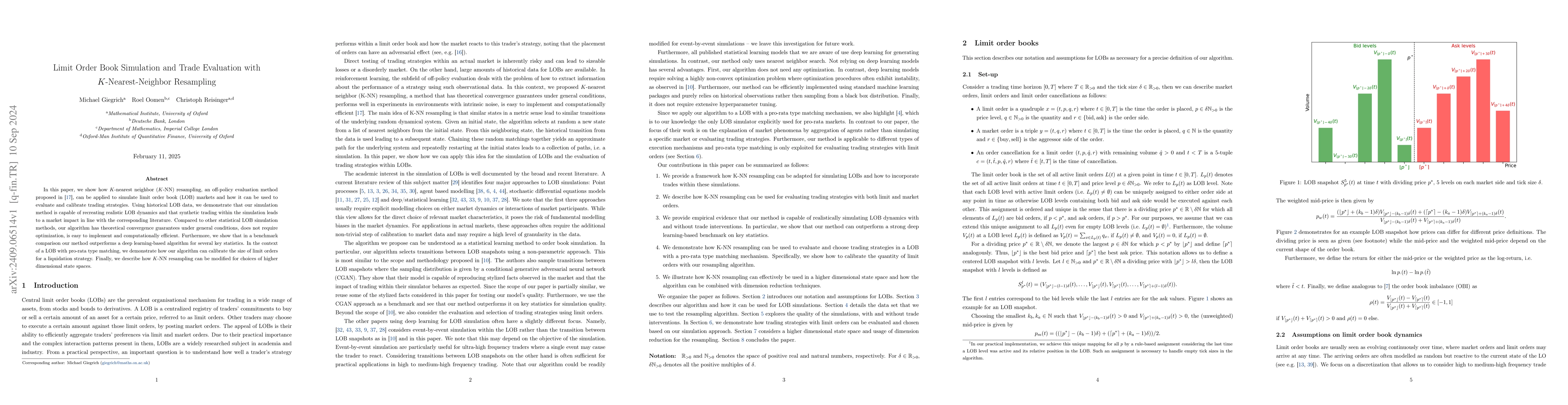

In this paper, we show how $K$-nearest neighbor ($K$-NN) resampling, an off-policy evaluation method proposed in \cite{giegrich2023k}, can be applied to simulate limit order book (LOB) markets and how...

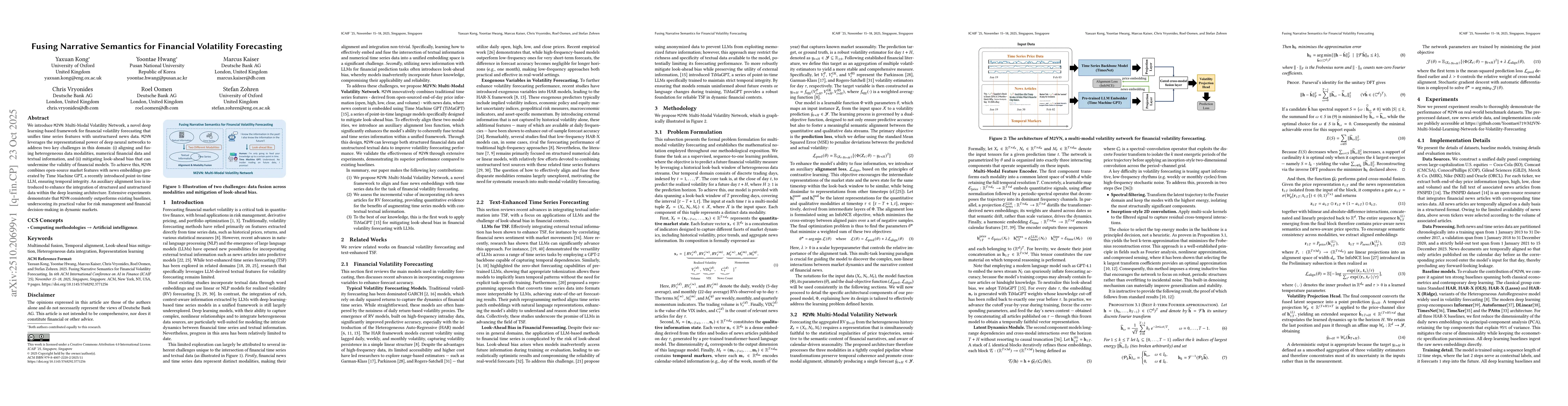

We introduce M2VN: Multi-Modal Volatility Network, a novel deep learning-based framework for financial volatility forecasting that unifies time series features with unstructured news data. M2VN levera...

In this paper, we propose a new jump robust quantile-based realised variance measure of ex-post return variation that can be computed using potentially noisy data. The estimator is consistent for the ...