1

arXiv Papers

Metrics

Statistics

1

arXiv Papers

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Prediction of financial time series using LSTM and data denoising

methods

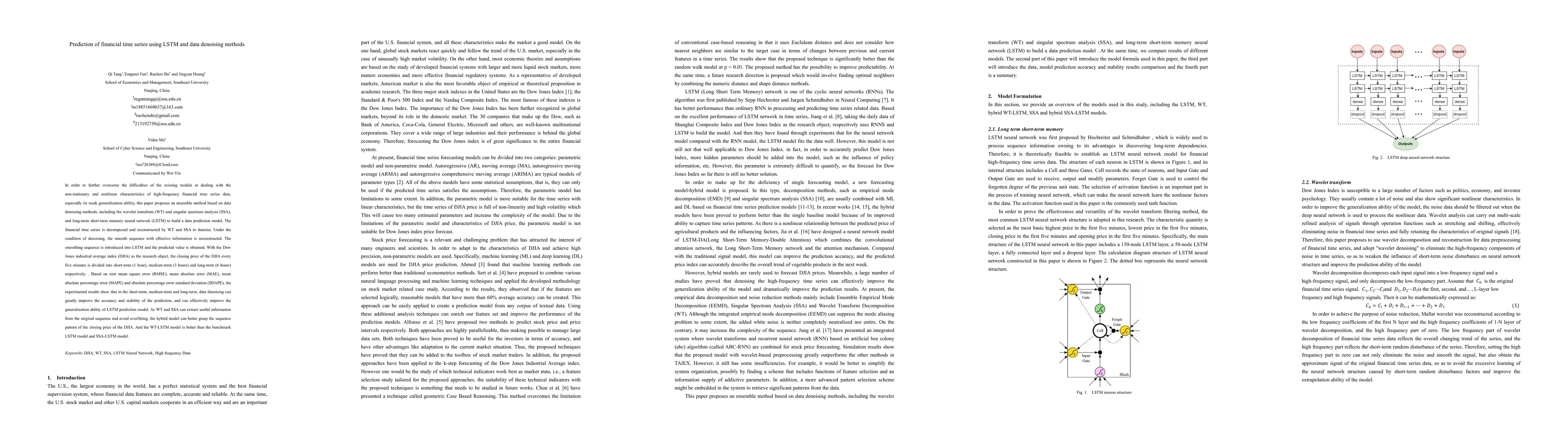

In order to further overcome the difficulties of the existing models in dealing with the non-stationary and nonlinear characteristics of high-frequency financial time series data, especially its wea...