Academic Profile

Statistics

Similar Authors

Papers on arXiv

Vector AutoRegressive Moving Average (VARMA) models form a powerful and general model class for analyzing dynamics among multiple time series. While VARMA models encompass the Vector AutoRegressive ...

We propose a novel approach for time series forecasting with many predictors, referred to as the GO-sdPCA, in this paper. The approach employs a variable selection method known as the group orthogon...

Ridge regression is an indispensable tool in big data econometrics but suffers from bias issues affecting both statistical efficiency and scalability. We introduce an iterative strategy to correct t...

This paper proposes a novel dynamic forecasting method using a new supervised Principal Component Analysis (PCA) when a large number of predictors are available. The new supervised PCA provides an e...

Feature-distributed data, referred to data partitioned by features and stored across multiple computing nodes, are increasingly common in applications with a large number of features. This paper pro...

This paper proposes a new approach to identifying the effective cointegration rank in high-dimensional unit-root (HDUR) time series from a prediction perspective using reduced-rank regression. For a...

High-dimensional time series data appear in many scientific areas in the current data-rich environment. Analysis of such data poses new challenges to data analysts because of not only the complicate...

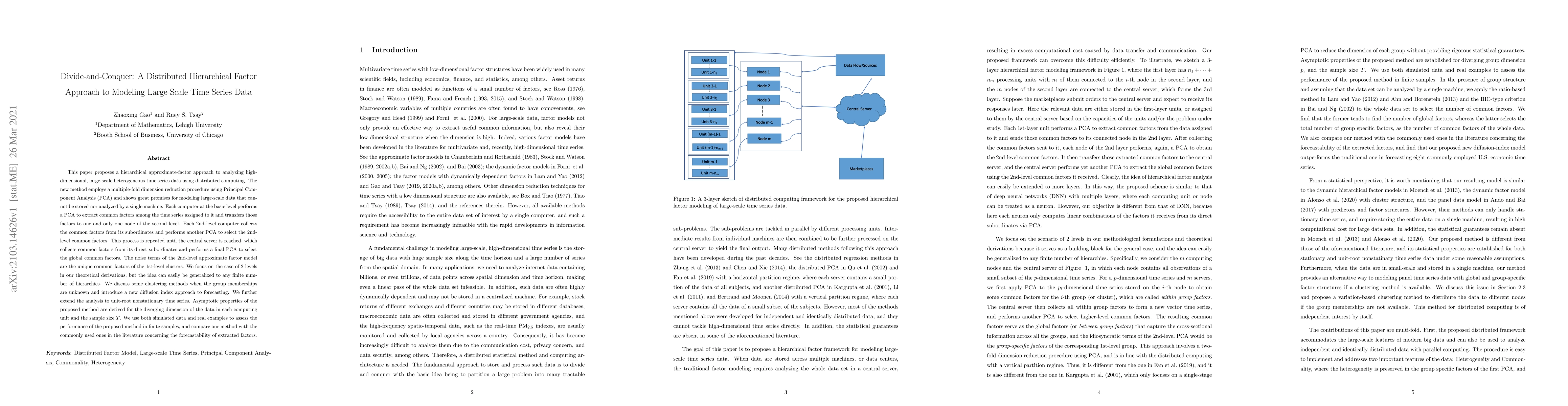

This paper proposes a hierarchical approximate-factor approach to analyzing high-dimensional, large-scale heterogeneous time series data using distributed computing. The new method employs a multipl...

We propose a new framework for modeling high-dimensional matrix-variate time series by a two-way transformation, where the transformed data consist of a matrix-variate factor process, which is dynam...

This paper proposes a new procedure to build factor models for high-dimensional unit-root time series by postulating that a $p$-dimensional unit-root process is a nonsingular linear transformation o...

It is of utmost importance to have a clear understanding of the status of air pollution and to provide forecasts and insights about the air quality to the general public and researchers in environme...

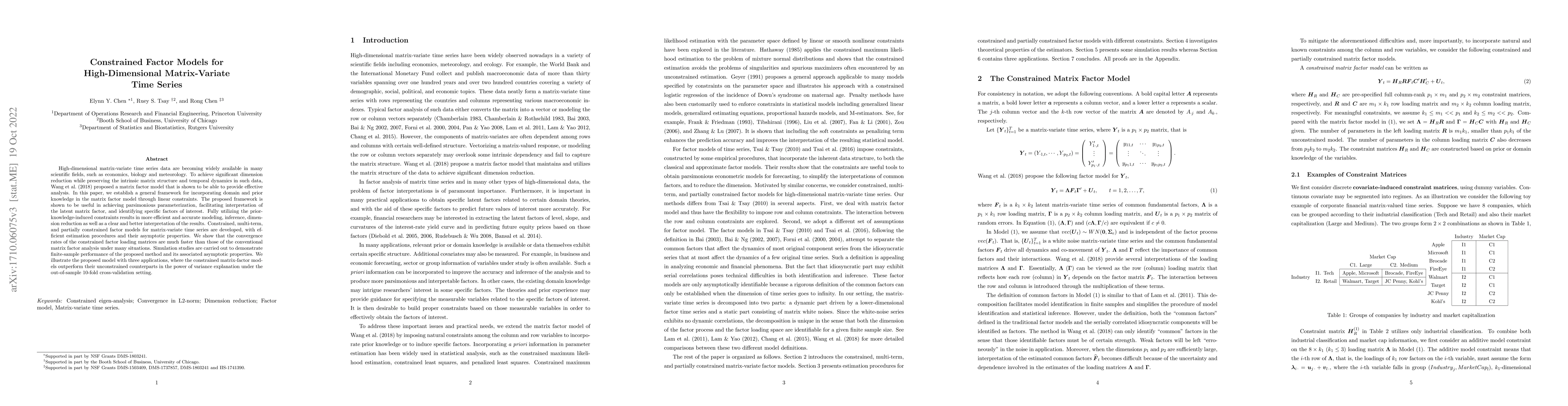

High-dimensional matrix-variate time series data are becoming widely available in many scientific fields, such as economics, biology, and meteorology. To achieve significant dimension reduction whil...

Recent research has focused on $\ell_1$ penalized least squares (Lasso) estimators for high-dimensional linear regressions in which the number of covariates $p$ is considerably larger than the sampl...

This article considers a novel and widely applicable approach to modeling high-dimensional dependent data when a large number of explanatory variables are available and the signal-to-noise ratio is lo...

Missing data often significantly hamper standard time series analysis, yet in practice they are frequently encountered. In this paper, we introduce temporal Wasserstein imputation, a novel method for ...

Anomaly detection (AD) is a fundamental task for time-series analytics with important implications for the downstream performance of many applications. In contrast to other domains where AD mainly foc...

This paper studies model selection for general unit-root time series, including the case with many exogenous predictors. We propose FHTD, a new model selection algorithm that leverages forward stepwis...

We investigate forward variable selection for ultra-high dimensional linear regression using a Gram-Schmidt orthogonalization procedure. Unlike the commonly used Forward Regression (FR) method, which ...

This paper extends the mean shift algorithm from vector-valued data to functional data, enabling effective clustering in infinite-dimensional settings. To address the computational challenges posed by...

This paper investigates estimation and inference of a Spatial Arbitrage Pricing Theory (SAPT) model that integrates spatial interactions with multi-factor analysis, accommodating both observable and l...