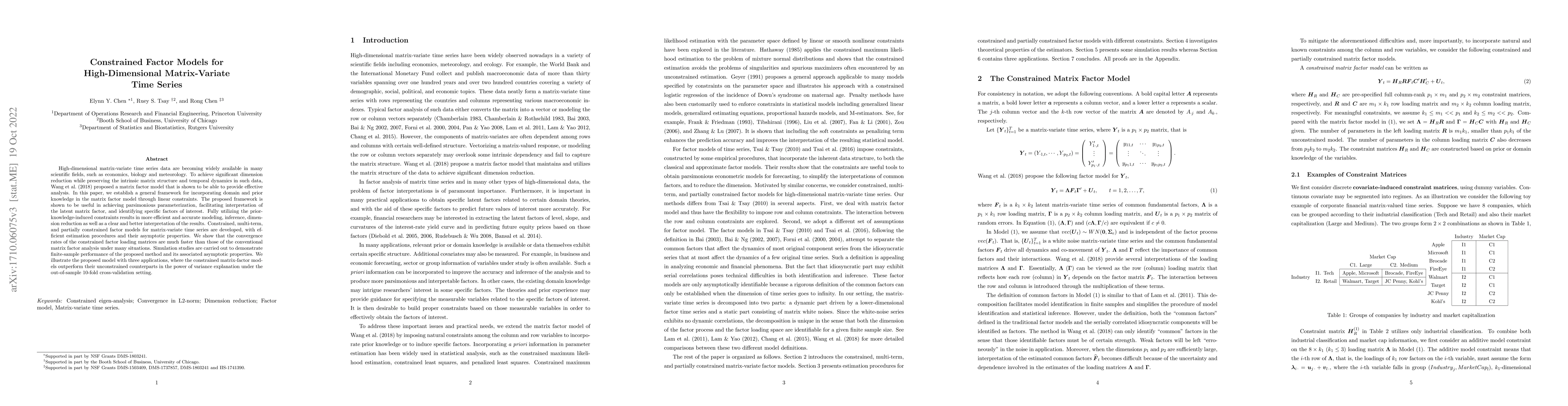

Constrained Factor Models for High-Dimensional Matrix-Variate Time Series

Publication

Metrics

AI Quick Summary

This paper proposes a framework for incorporating domain knowledge into matrix factor models for high-dimensional matrix-variate time series through linear constraints, achieving faster convergence rates and better interpretation. Simulation studies and applications demonstrate the improved performance of the constrained models over their unconstrained counterparts.

Paper Preview

Abstract

High-dimensional matrix-variate time series data are becoming widely available in many scientific fields, such as economics, biology, and meteorology. To achieve significant dimension reduction while preserving the intrinsic matrix structure and temporal dynamics in such data, Wang et al. (2017) proposed a matrix factor model that is shown to provide effective analysis. In this paper, we establish a general framework for incorporating domain or prior knowledge in the matrix factor model through linear constraints. The proposed framework is shown to be useful in achieving parsimonious parameterization, facilitating interpretation of the latent matrix factor, and identifying specific factors of interest. Fully utilizing the prior-knowledge-induced constraints results in more efficient and accurate modeling, inference, dimension reduction as well as a clear and better interpretation of the results. In this paper, constrained, multi-term, and partially constrained factor models for matrix-variate time series are developed, with efficient estimation procedures and their asymptotic properties. We show that the convergence rates of the constrained factor loading matrices are much faster than those of the conventional matrix factor analysis under many situations. Simulation studies are carried out to demonstrate the finite-sample performance of the proposed method and its associated asymptotic properties. We illustrate the proposed model with three applications, where the constrained matrix-factor models outperform their unconstrained counterparts in the power of variance explanation under the out-of-sample 10-fold cross-validation setting.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0