Academic Profile

Statistics

Similar Authors

Papers on arXiv

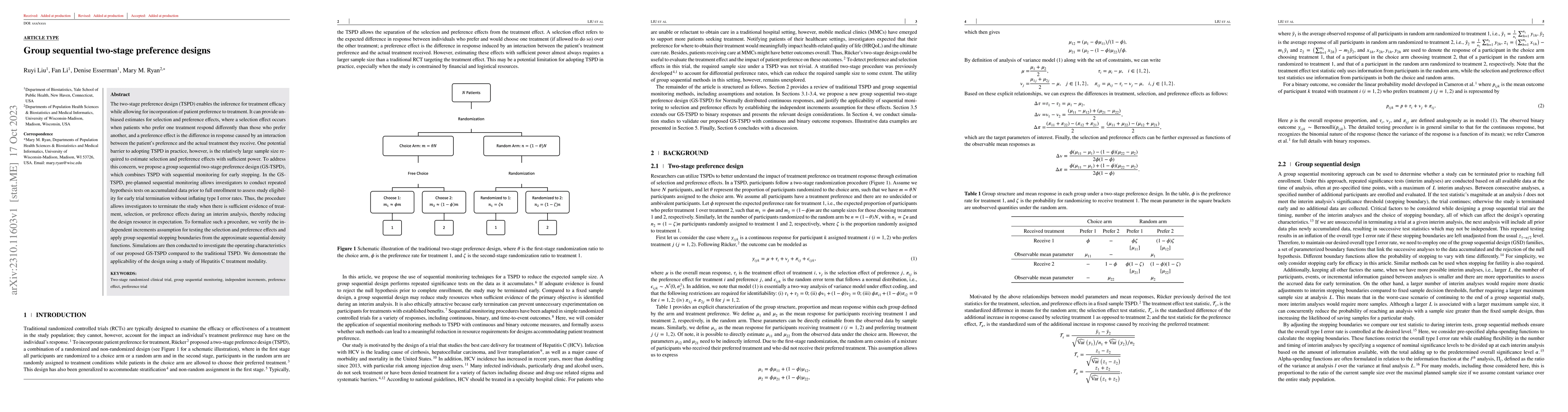

The two-stage preference design (TSPD) enables the inference for treatment efficacy while allowing for incorporation of patient preference to treatment. It can provide unbiased estimates for selecti...

The focus of this paper is on identifying the most effective selling strategy for pairs trading of stocks. In pairs trading, a long position is held in one stock while a short position is held in an...

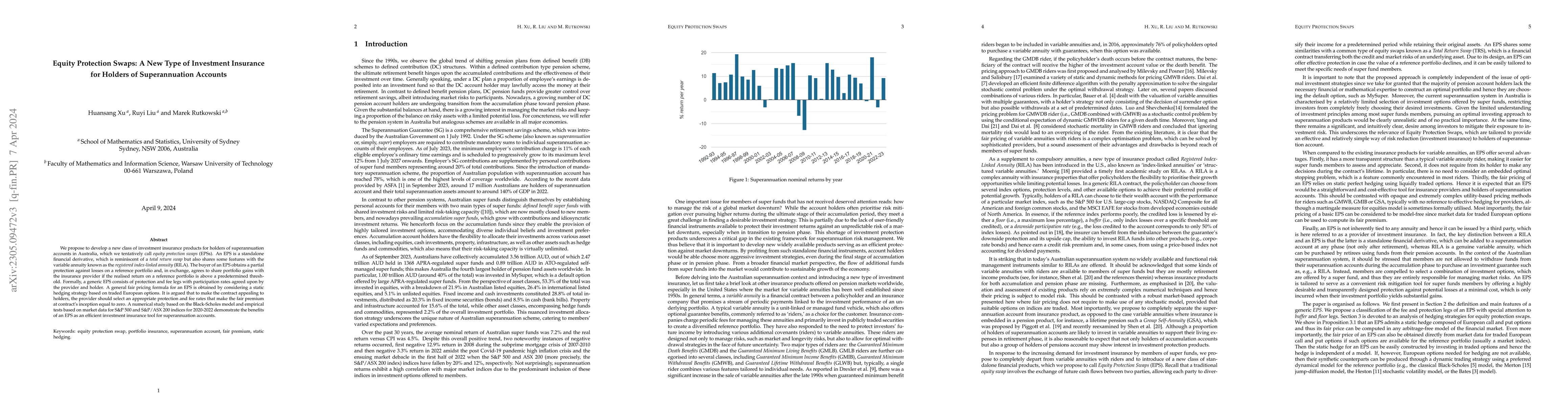

We propose to develop a new class of investment insurance products for holders of superannuation accounts in Australia, which we tentatively call equity protection swaps (EPSs). An EPS is a standalo...

We study the upper and lower bounds for prices of European and American style options with the possibility of an external termination, meaning that the contract may be terminated at some random time...

The paper is directly motivated by the pricing of vulnerable European and American options in a general hazard process setup and a related study of the corresponding pre-default backward stochastic ...

In this paper, we investigate two families of fully coupled linear Forward-Backward Stochastic Differential Equations (FBSDE). Within these families, one could get the same well-posedness of FBSDEs ...

In this paper, we consider a continuous-time mean-variance portfolio selection with regime-switching and random horizon. Unlike previous works, the dynamic of assets are described by non-Markovian r...

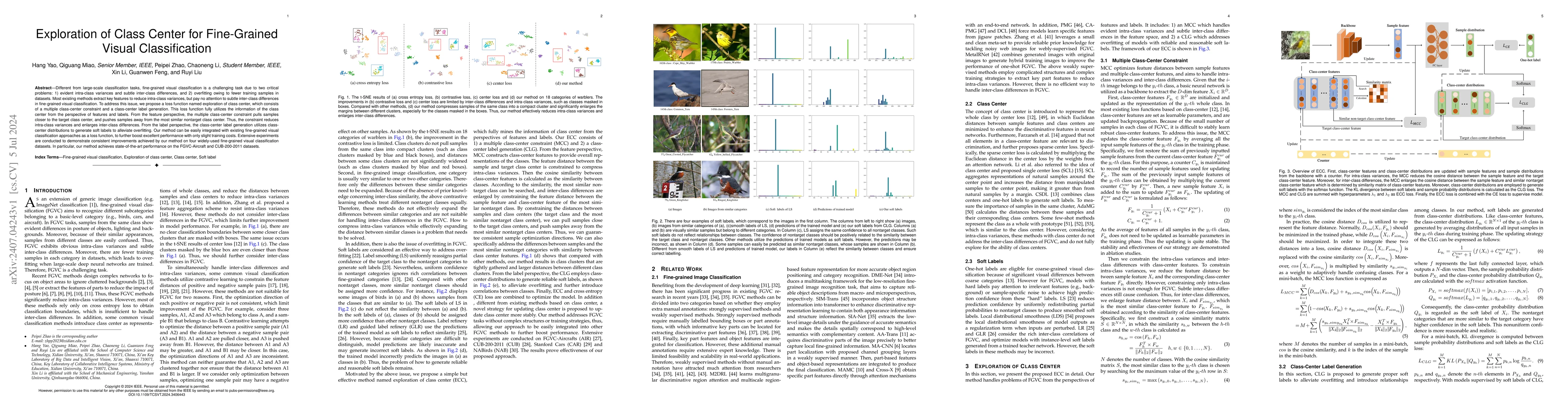

Different from large-scale classification tasks, fine-grained visual classification is a challenging task due to two critical problems: 1) evident intra-class variances and subtle inter-class differen...

The financial industry has undergone a significant transition from the London Interbank Offered Rate (LIBOR) to Risk Free Rates (RFR) such as, e.g., the Secured Overnight Financing Rate (SOFR) in the ...

Hybrid type 2 studies are gaining popularity for their ability to assess both implementation and health outcomes as co-primary endpoints. Often conducted as cluster-randomized trials (CRTs), five desi...

In cluster-randomized trials (CRTs), entire clusters of individuals are randomized to treatment, and outcomes within a cluster are typically correlated. While frequentist approaches are standard pract...

Text-to-image diffusion models can generate diverse content with flexible prompts, which makes them well-suited for customization through fine-tuning with a small amount of user-provided data. However...

The role of collateral in derivative pricing has evolved beyond credit risk mitigation, particularly following the global financial crisis, when funding costs and basis spreads became central to valua...

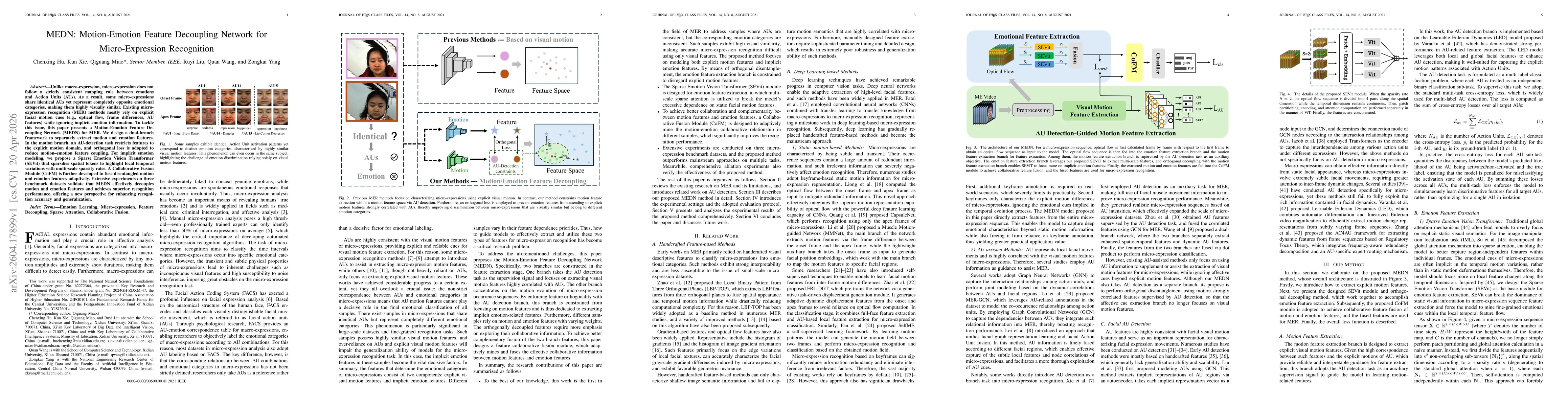

Unlike macro-expression, micro-expression does not follow a strictly consistent mapping rule between emotions and Action Units (AUs). As a result, some micro-expressions share identical AUs yet repres...

The accurate modeling of reflection coefficients is pivotal for developing reliable channel models in emerging terahertz (THz) communications. This study establishes a 300$\sim$400 GHz channel measure...