Academic Profile

Statistics

Similar Authors

Papers on arXiv

The rough Bergomi model, introduced by Bayer, Friz and Gatheral [Quant. Finance 16(6), 887-904, 2016], is one of the recent rough volatility models that are consistent with the stylised fact of impl...

This article consolidates and extends past work on derivative pricing adjustments, including XVA, by providing an encapsulating representation of the adjustment between any two derivative pricing func...

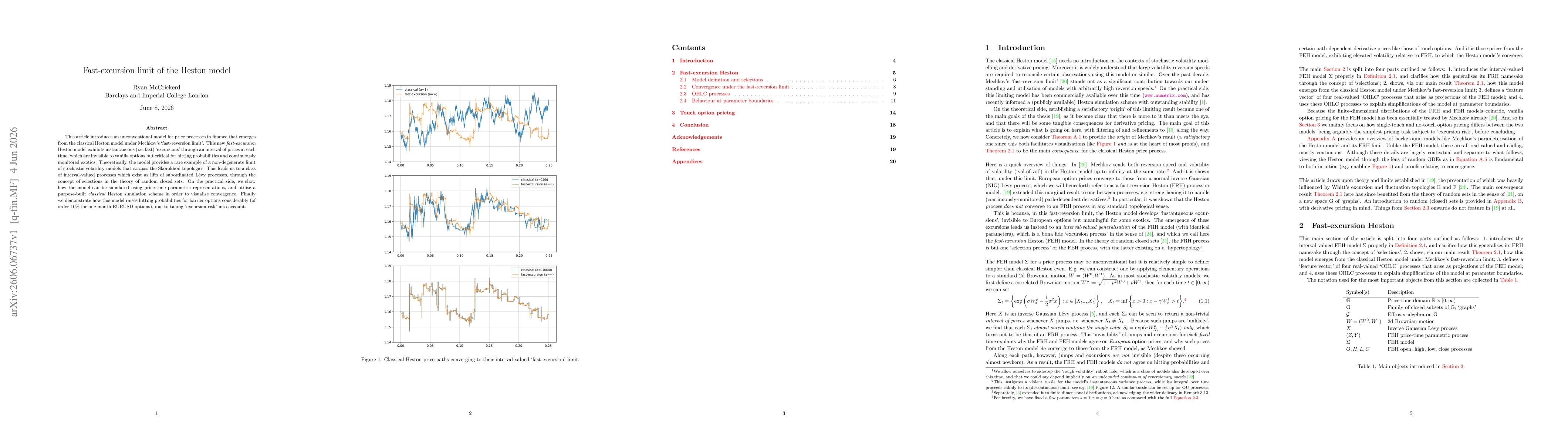

This article introduces an unconventional model for price processes in finance that emerges from the classical Heston model under Mechkov's fast-reversion limit. This new fast-excursion Heston model e...