Publication

Metrics

Paper Preview

Abstract

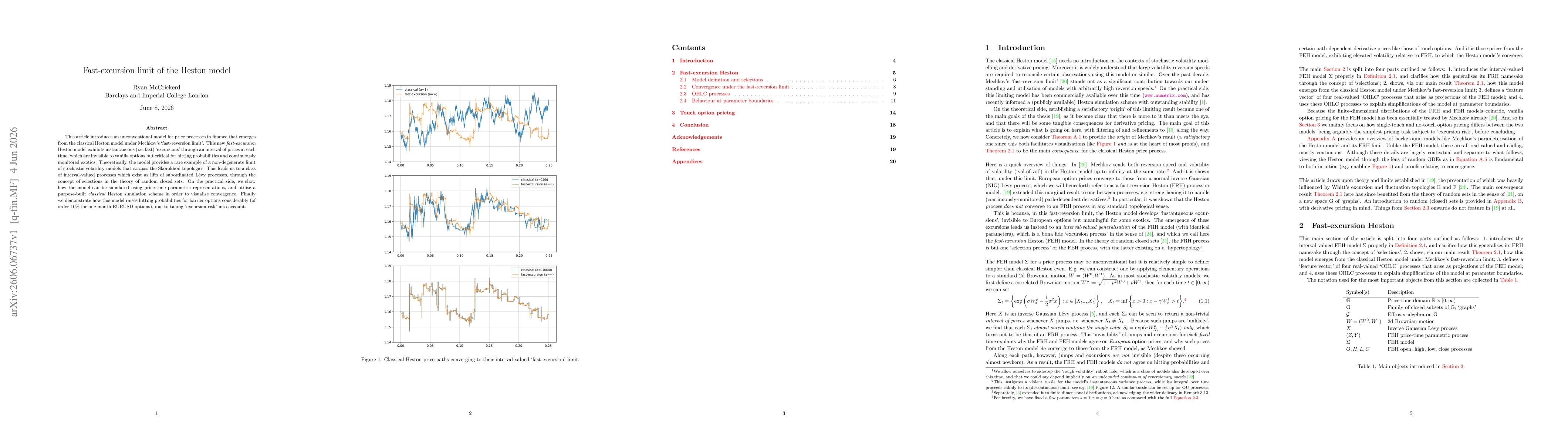

This article introduces an unconventional model for price processes in finance that emerges from the classical Heston model under Mechkov's fast-reversion limit. This new fast-excursion Heston model exhibits instantaneous (i.e. fast) excursions through an interval of prices at each time, which are invisible to vanilla options but critical for hitting probabilities and continuously monitored exotics. Theoretically, the model provides a rare example of a non-degenerate limit of stochastic volatility models that escapes the Skorokhod topologies. This leads us to a class of interval-valued processes which exist as lifts of subordinated Levy processes, through the concept of selections in the theory of random closed sets. On the practical side, we show how the model can be simulated using price-time parametric representations, and utilise a purpose-built classical Heston simulation scheme in order to visualise convergence. Finally we demonstrate how this model raises hitting probabilities for barrier options considerably (of order 10% for one-month EURUSD options), due to taking excursion risk into account.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0