1

arXiv Papers

13

Total Publications

Profile

Academic Profile

Metrics

Statistics

1

arXiv Papers

13

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

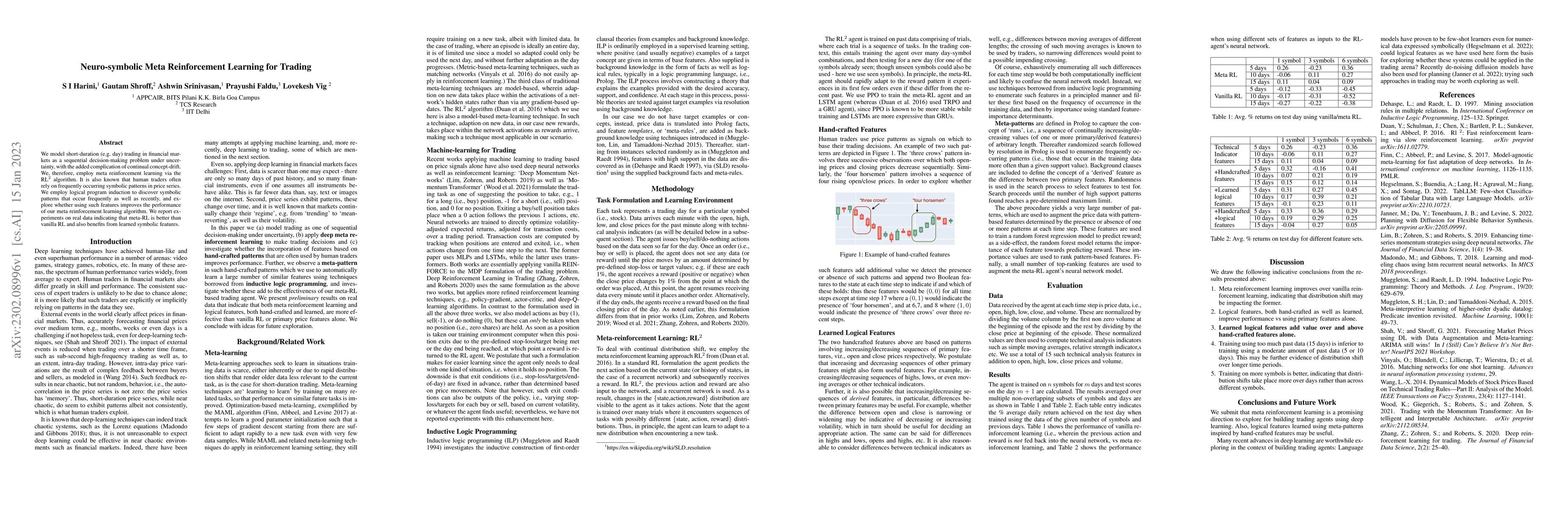

Neuro-symbolic Meta Reinforcement Learning for Trading

We model short-duration (e.g. day) trading in financial markets as a sequential decision-making problem under uncertainty, with the added complication of continual concept-drift. We, therefore, empl...