Academic Profile

Statistics

Similar Authors

Papers on arXiv

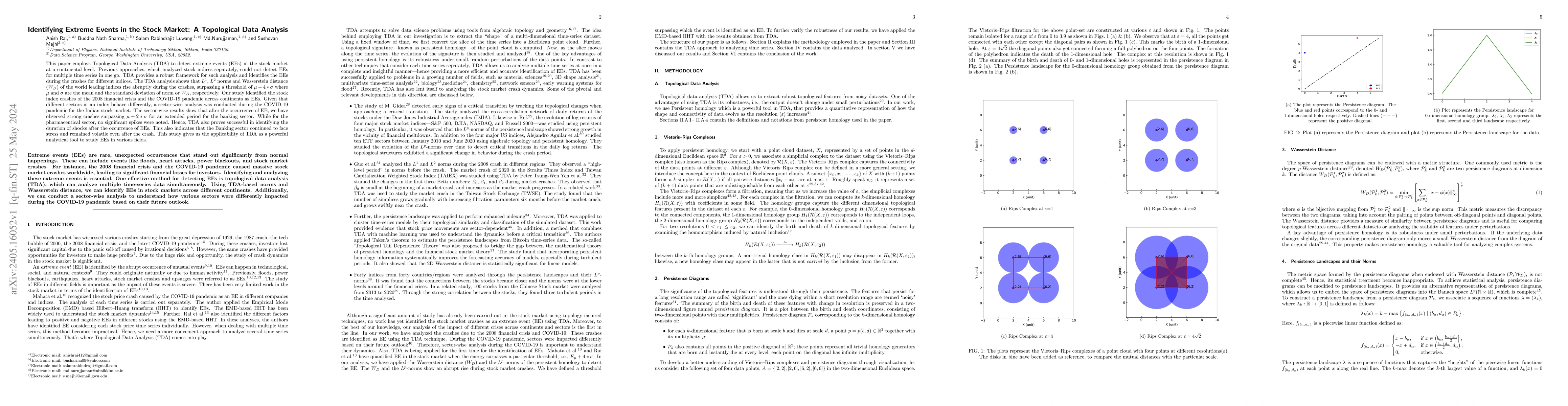

This paper employs Topological Data Analysis (TDA) to detect extreme events (EEs) in the stock market at a continental level. Previous approaches, which analyzed stock indices separately, could not ...

Statistical analysis of high-frequency stock market order transaction data is conducted to understand order transition dynamics. We employ a first-order time-homogeneous discrete-time Markov chain m...

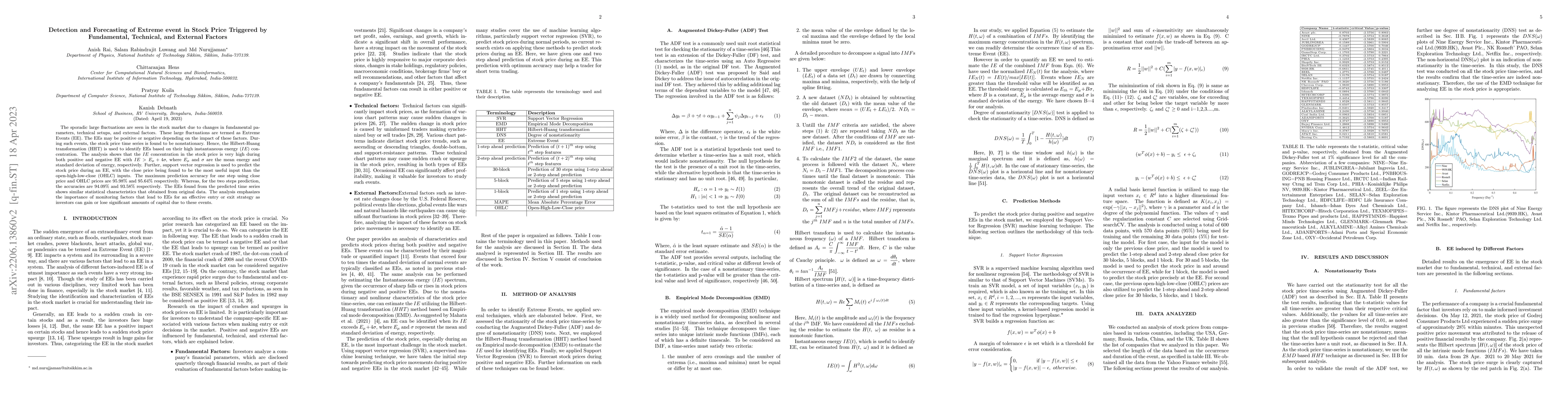

The sporadic large fluctuations are seen in the stock market due to changes in fundamental parameters, technical setups, and external factors. These large fluctuations are termed as Extreme Events (...

We study how the 2024 U.S. presidential election, viewed as a major political risk event, affected cryptocurrency markets by distinguishing human-driven peer-to-peer stablecoin transactions from autom...

Quantitative understanding of stochastic dynamics in limit order price changes is essential for execution strategy design. We analyze intraday transition dynamics of ask and bid orders across market c...

Financial markets alternate between tranquil periods and episodes of stress, and return dynamics can change substantially across these regimes. We study regime-dependent dynamics in developed and deve...

Persistent homology (PH) -- the conventional method in topological data analysis -- is computationally expensive, requires further vectorization of its signatures before machine learning (ML) can be a...