Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce OFTER, a time series forecasting pipeline tailored for mid-sized multivariate time series. OFTER utilizes the non-parametric models of k-nearest neighbors and Generalized Regression Neu...

We investigate the use of the normalized imbalance between option volumes corresponding to positive and negative market views, as a predictor for directional price movements in the spot market. Via ...

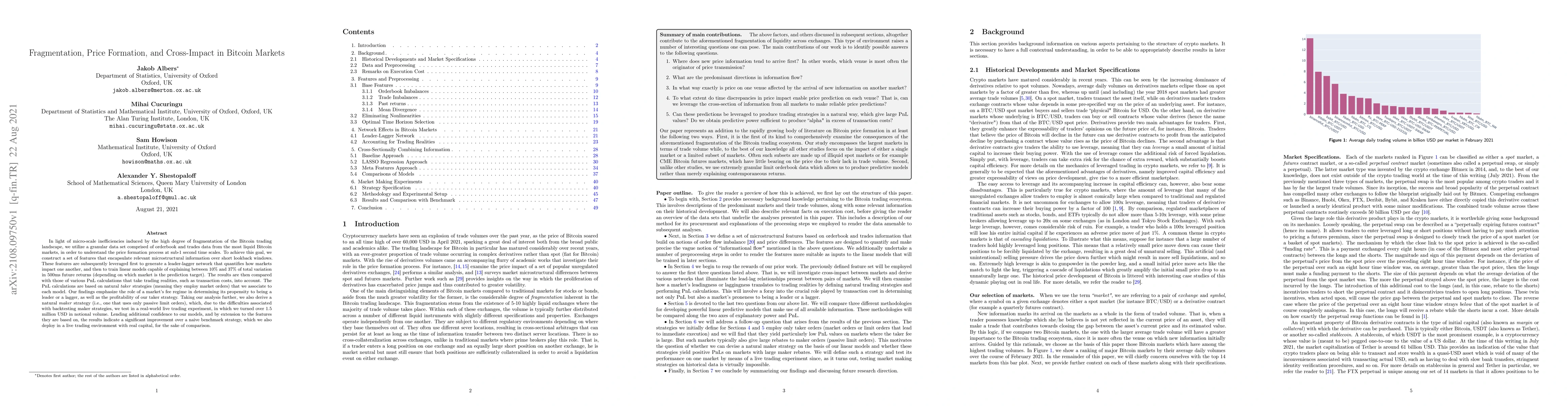

In light of micro-scale inefficiencies induced by the high degree of fragmentation of the Bitcoin trading landscape, we utilize a granular data set comprised of orderbook and trades data from the mo...

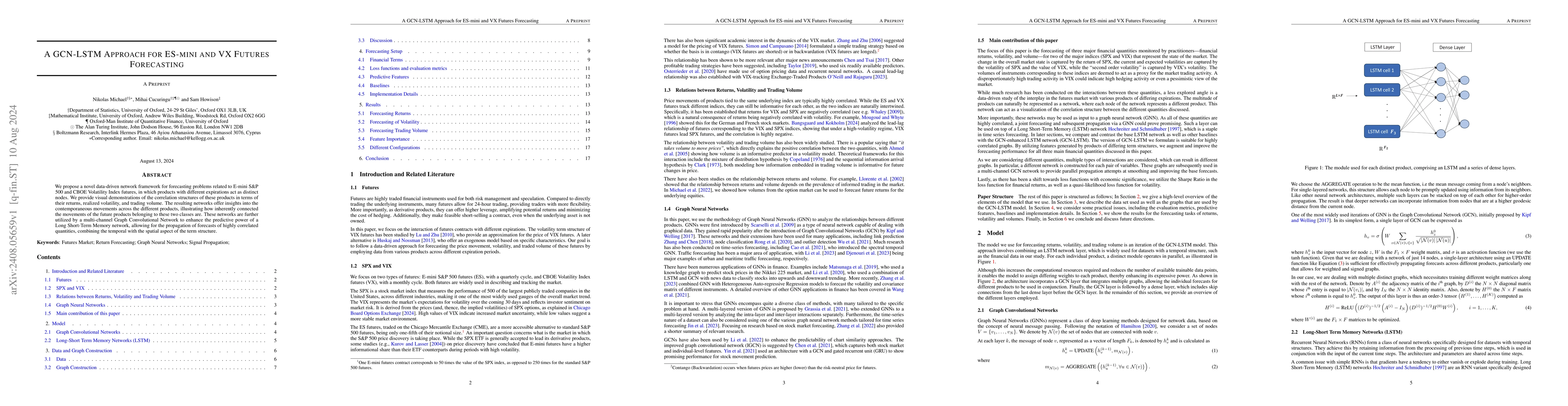

We propose a novel data-driven network framework for forecasting problems related to E-mini S\&P 500 and CBOE Volatility Index futures, in which products with different expirations act as distinct nod...

Working at a very granular level, using data from a live trading experiment on the Binance linear Bitcoin perpetual-the most liquid crypto market worldwide-we examine the effects of (i) basic order bo...