Academic Profile

Statistics

Similar Authors

Papers on arXiv

Over the past decade, characterizing the exact asymptotic risk of regularized estimators in high-dimensional regression has emerged as a popular line of work. This literature considers the proportio...

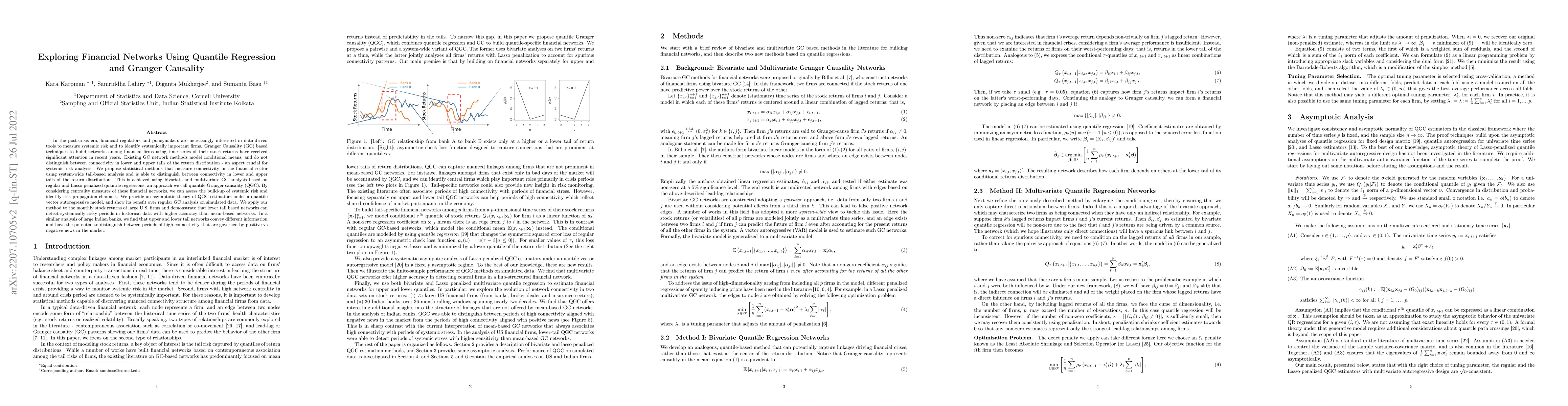

In the post-crisis era, financial regulators and policymakers are increasingly interested in data-driven tools to measure systemic risk and to identify systemically important firms. Granger Causalit...

In classical statistics, a well known paradigm consists in establishing asymptotic equivalence between an experiment of i.i.d. observations and a Gaussian shift experiment, with the aim of obtaining...

High-dimensional time series appear in many scientific setups, demanding a nuanced approach to model and analyze the underlying dependence structure. However, theoretical advancements so far often rel...

Stochastic network models play a central role across a wide range of scientific disciplines, and questions of statistical inference arise naturally in this context. In this paper we investigate goodne...