Academic Profile

Statistics

Similar Authors

Papers on arXiv

For vanilla derivatives that constitute the bulk of investment banks' hedging portfolios, central clearing through central counterparties (CCPs) has become hegemonic. A key mandate of a CCP is to pr...

In this work, we study the extremal functions of the log-Sobolev functional on compact metric measure spaces satisfying the $\mathrm{RCD}^*(K,N)$ condition for $K$ in $\mathbb{R}$ and $N$ in $(2,\in...

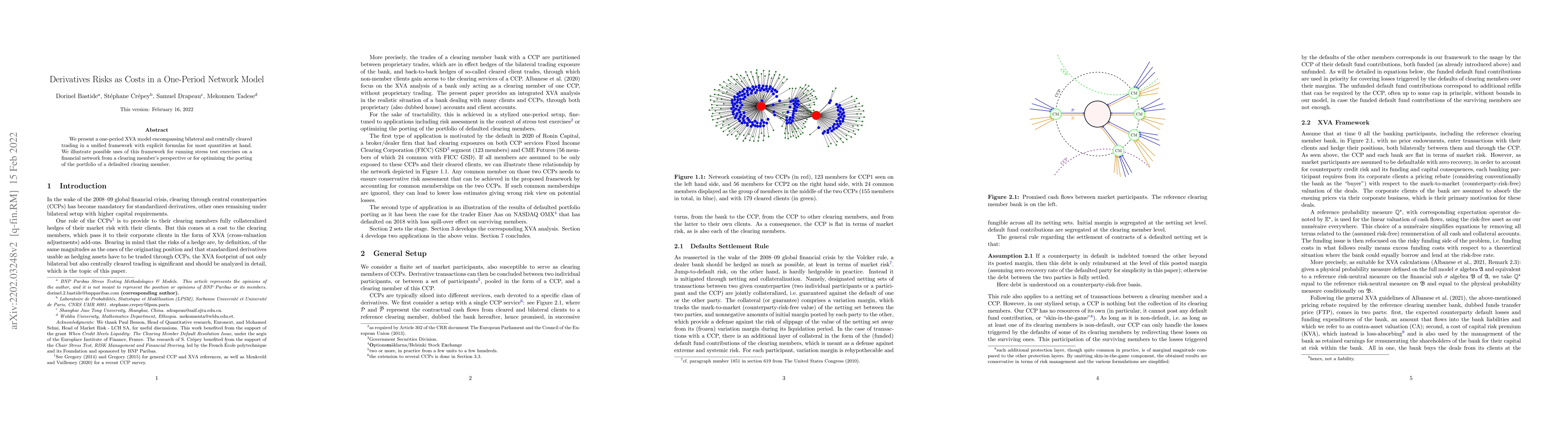

We present a one-period XVA model encompassing bilateral and centrally cleared trading in a unified framework with explicit formulas for most quantities at hand. We illustrate possible uses of this ...

We provide $q$-moment estimates on annuli for weak solutions of the singular $p$-Laplace equation where $p$ and $q$ are conjugates. We derive $q$-uniform integrability for some critical parameter ra...

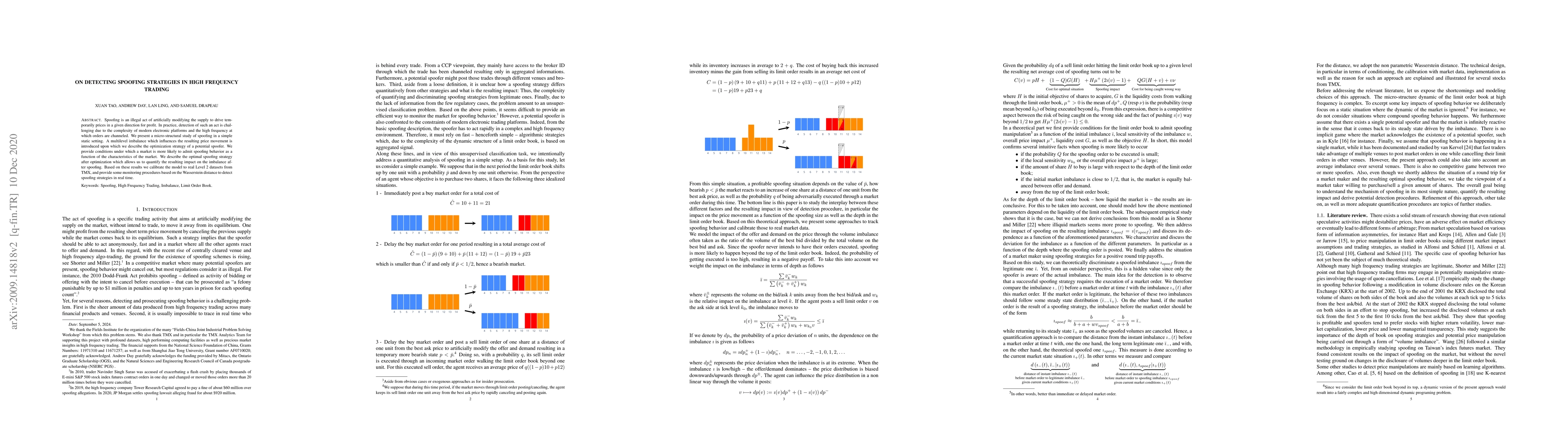

Spoofing is an illegal act of artificially modifying the supply to drive temporarily prices in a given direction for profit. In practice, detection of such an act is challenging due to the complexit...

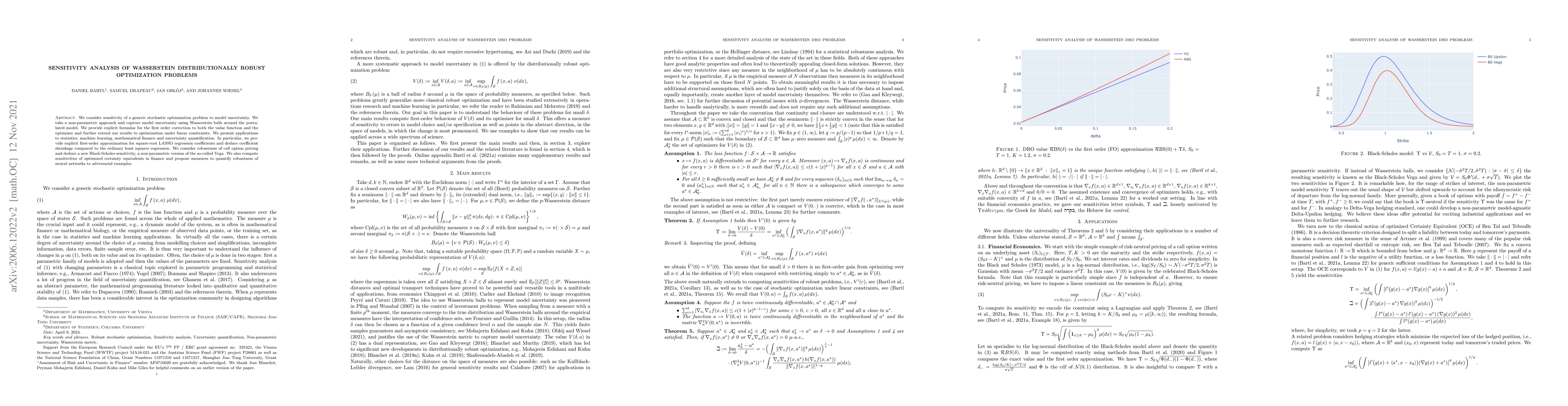

We consider sensitivity of a generic stochastic optimization problem to model uncertainty. We take a non-parametric approach and capture model uncertainty using Wasserstein balls around the postulat...

We analyze a market impact game between $n$ risk averse agents who compete for liquidity in a market impact model with permanent price impact and additional slippage. Most market parameters, includi...

The expectile can be considered as a generalization of quantile. While expected shortfall is a quantile based risk measure, we study its counterpart -- the expectile based expected shortfall -- wher...

We establish a Fenchel-Moreau type theorem for proper convex functions $f\colon X\to \bar{L}^0$, where $(X, Y, \langle \cdot,\cdot \rangle)$ is a dual pair of Banach spaces and $\bar L^0$ is the spa...

Carbon pricing has become a central pillar of modern climate policy, with carbon taxes and emissions trading systems (ETS) serving as the two dominant approaches. Although economic theory suggests the...

Generative Flow Network (GFlowNet) objectives implicitly fix an equal mixing of forward and backward policies, potentially constraining the exploration-exploitation trade-off during training. By furth...

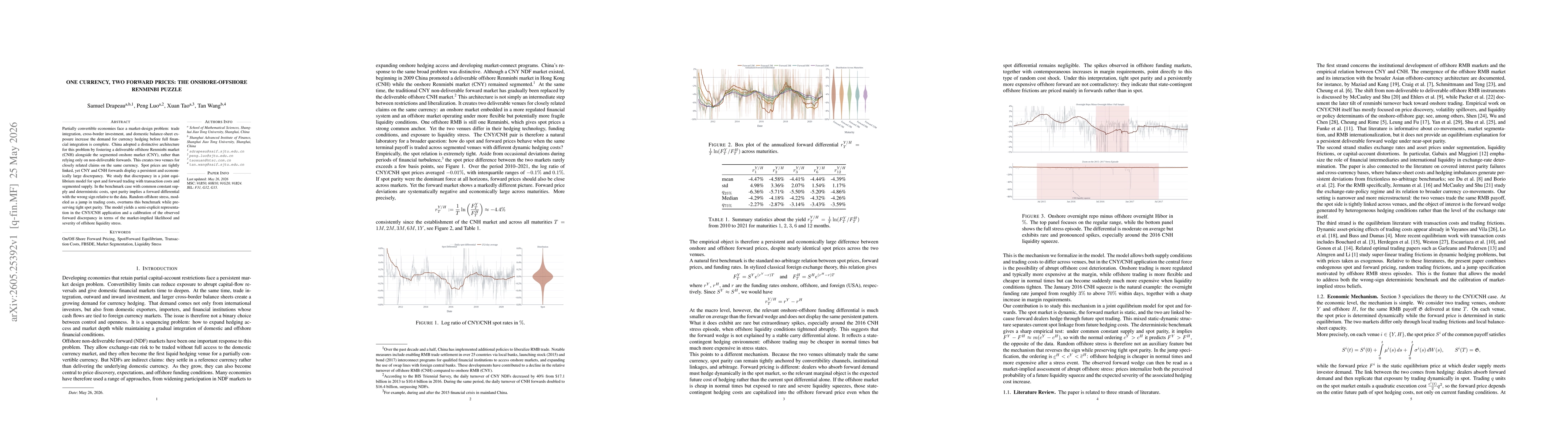

Partially convertible economies face a market-design problem: trade integration, cross-border investment, and domestic balance-sheet exposure increase the demand for currency hedging before full finan...