Academic Profile

Statistics

Similar Authors

Papers on arXiv

We present a natural extension of the SABR model to price both backward and forward-looking RFR caplets in a post-Libor world. Forward-looking RFR caplets can be priced using the market standard app...

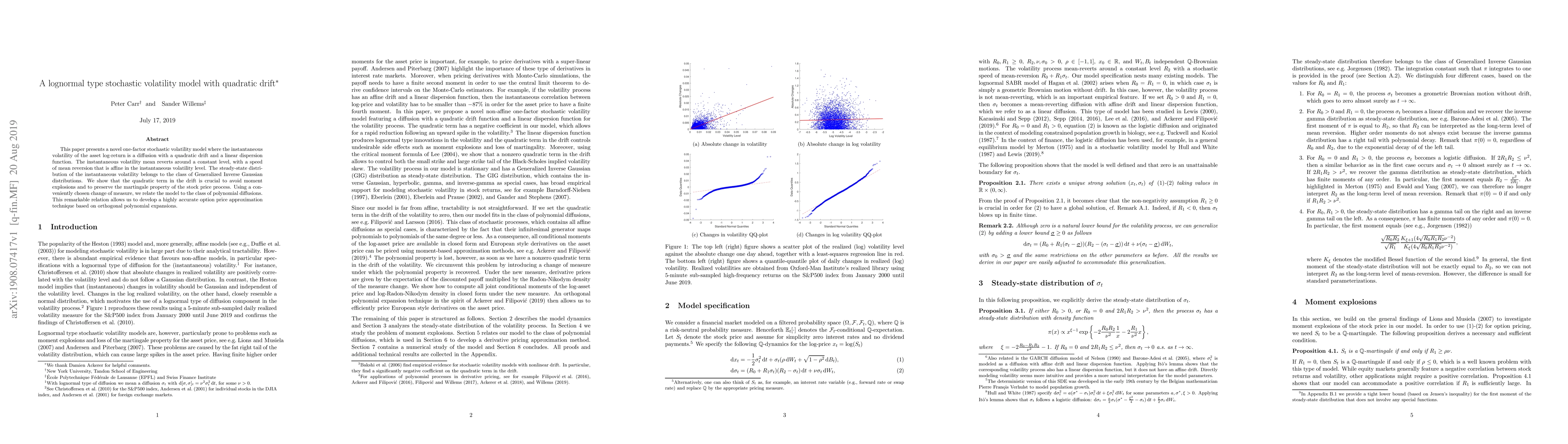

This paper presents a novel one-factor stochastic volatility model where the instantaneous volatility of the asset log-return is a diffusion with a quadratic drift and a linear dispersion function. ...

In this paper we propose a new model for pricing stock and dividend derivatives. We jointly specify dynamics for the stock price and the dividend rate such that the stock price is positive and the d...

Over the last decade, dividends have become a standalone asset class instead of a mere side product of an equity investment. We introduce a framework based on polynomial jump-diffusions to jointly p...