Academic Profile

Statistics

Similar Authors

Papers on arXiv

The forecast accuracy of deep-learning-based weather prediction models is improving rapidly, leading many to speak of a "second revolution in weather forecasting". With numerous methods being develo...

Extremal graphical models encode the conditional independence structure of multivariate extremes and provide a powerful tool for quantifying the risk of rare events. Prior work on learning these gra...

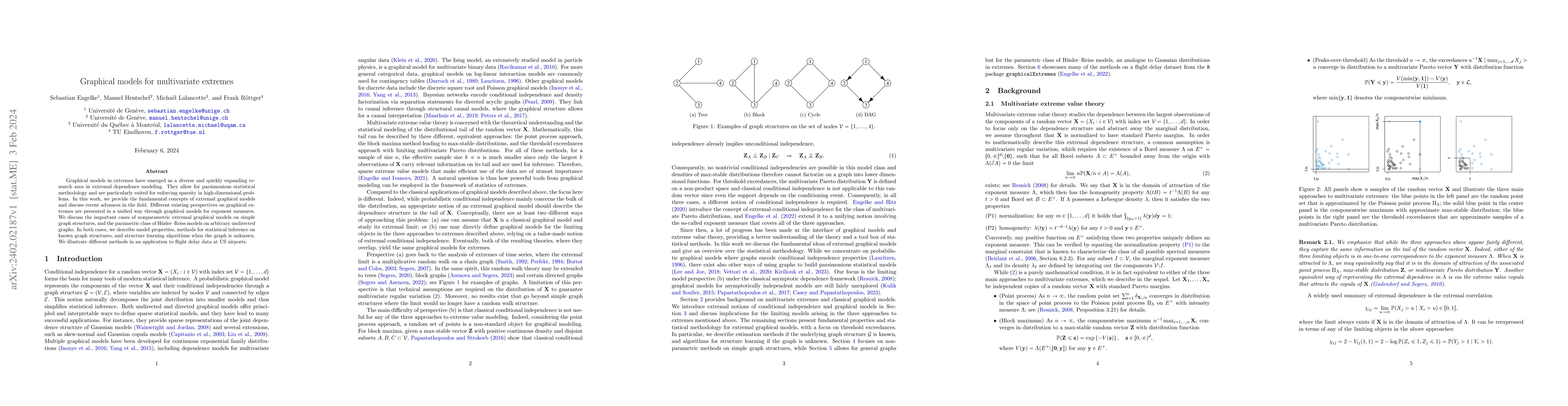

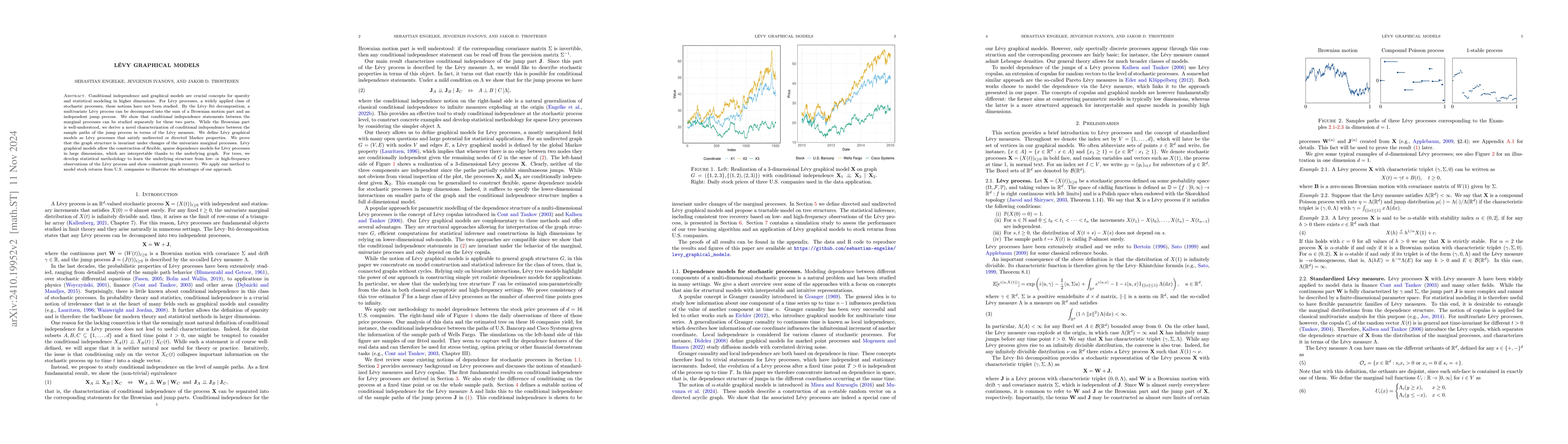

Graphical models in extremes have emerged as a diverse and quickly expanding research area in extremal dependence modeling. They allow for parsimonious statistical methodology and are particularly s...

Modern machine learning methods and the availability of large-scale data opened the door to accurately predict target quantities from large sets of covariates. However, existing prediction methods c...

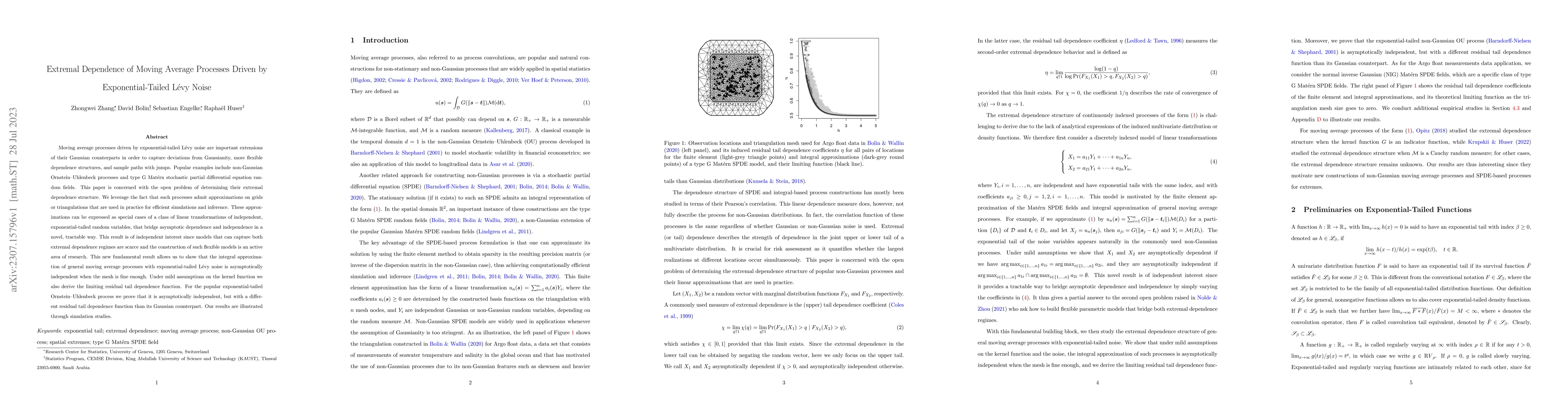

Moving average processes driven by exponential-tailed L\'evy noise are important extensions of their Gaussian counterparts in order to capture deviations from Gaussianity, more flexible dependence s...

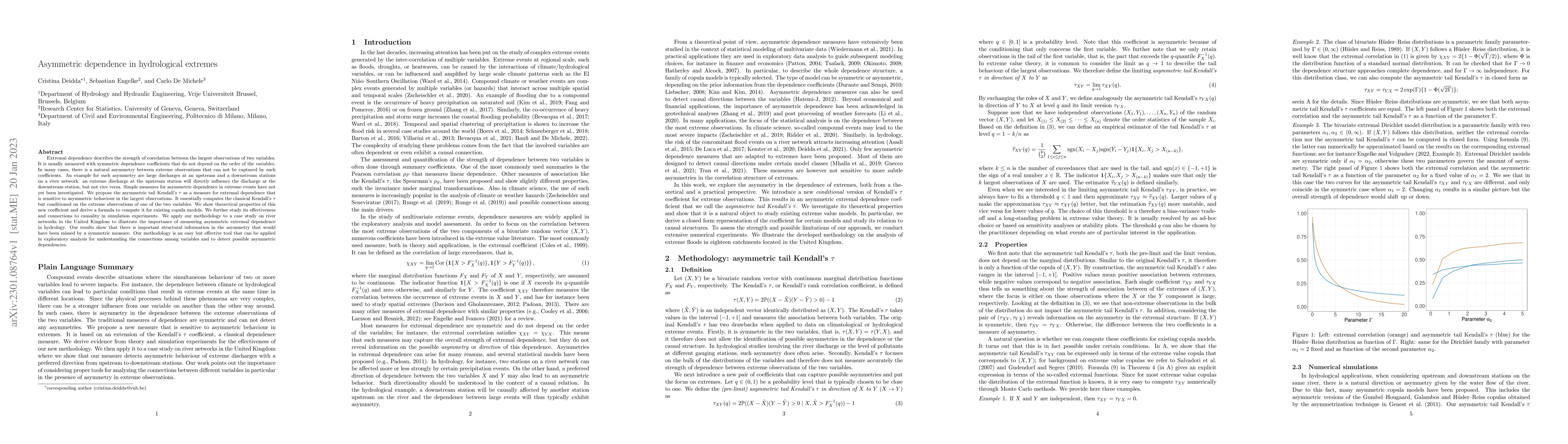

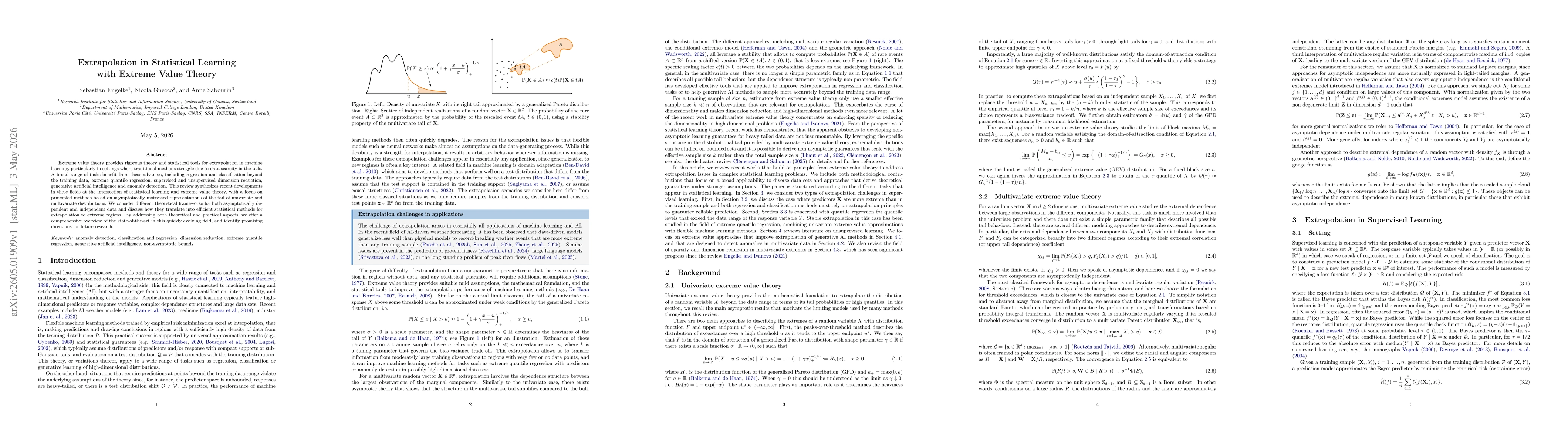

Extremal dependence describes the strength of correlation between the largest observations of two variables. It is usually measured with symmetric dependence coefficients that do not depend on the o...

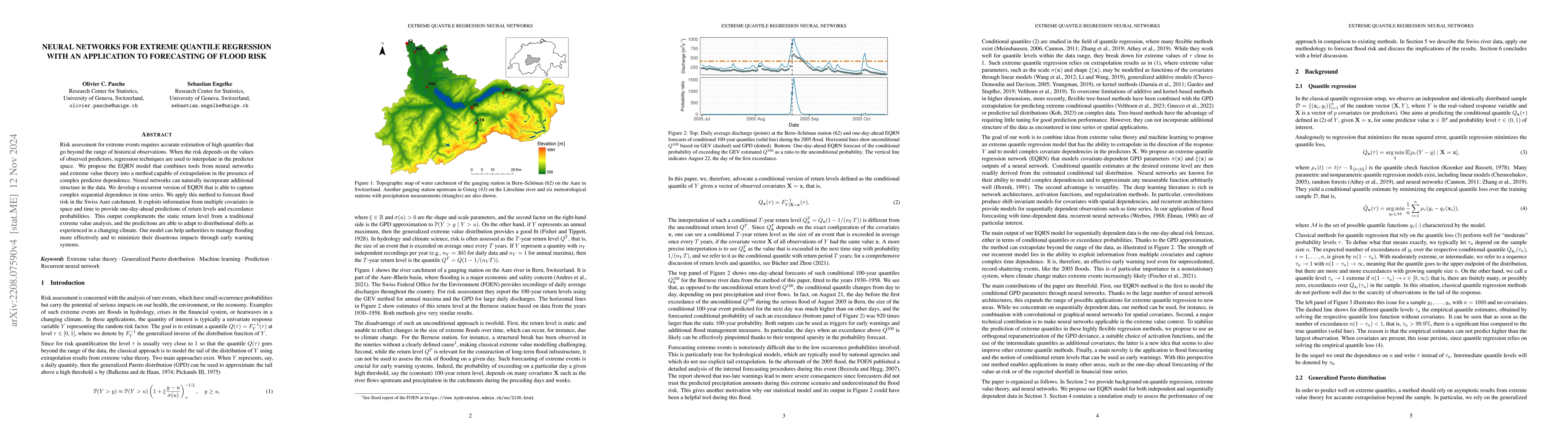

Risk assessment for extreme events requires accurate estimation of high quantiles that go beyond the range of historical observations. When the risk depends on the values of observed predictors, reg...

Extreme value applications commonly employ regression techniques to capture cross-sectional heterogeneity or time-variation in the data. Estimation of the parameters of an extreme value regression m...

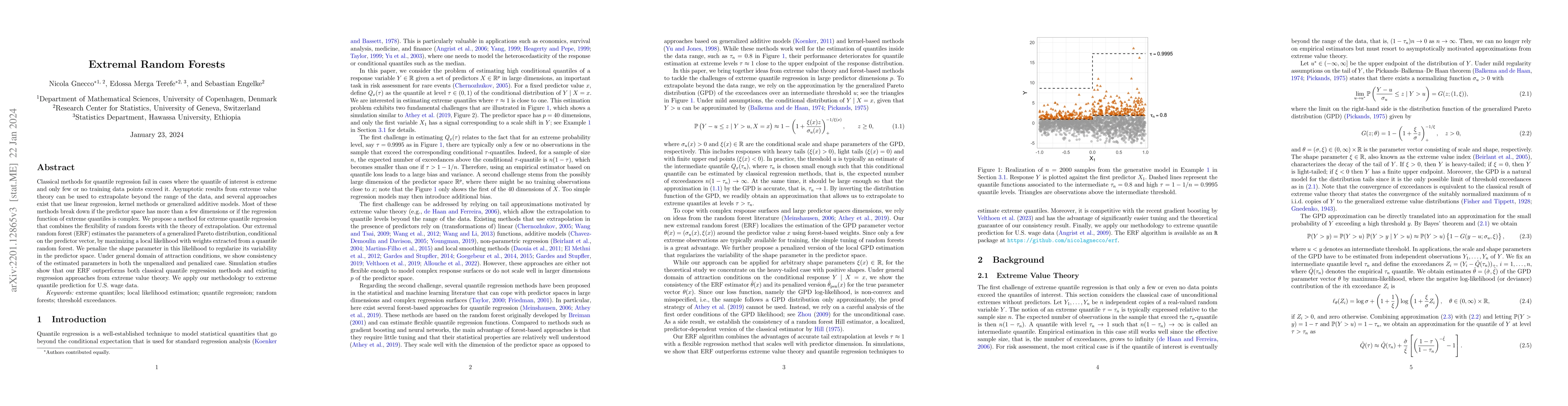

Classical methods for quantile regression fail in cases where the quantile of interest is extreme and only few or no training data points exceed it. Asymptotic results from extreme value theory can ...

Positive dependence is present in many real world data sets and has appealing stochastic properties that can be exploited in statistical modeling and in estimation. In particular, the notion of mult...

Extremal graphical models encode the conditional independence structure of multivariate extremes. For the popular class of H\"usler--Reiss models, we propose a majority voting algorithm for learning...

Modelling dependencies between climate extremes is important for climate risk assessment, for instance when allocating emergency management funds. In statistics, multivariate extreme value theory is...

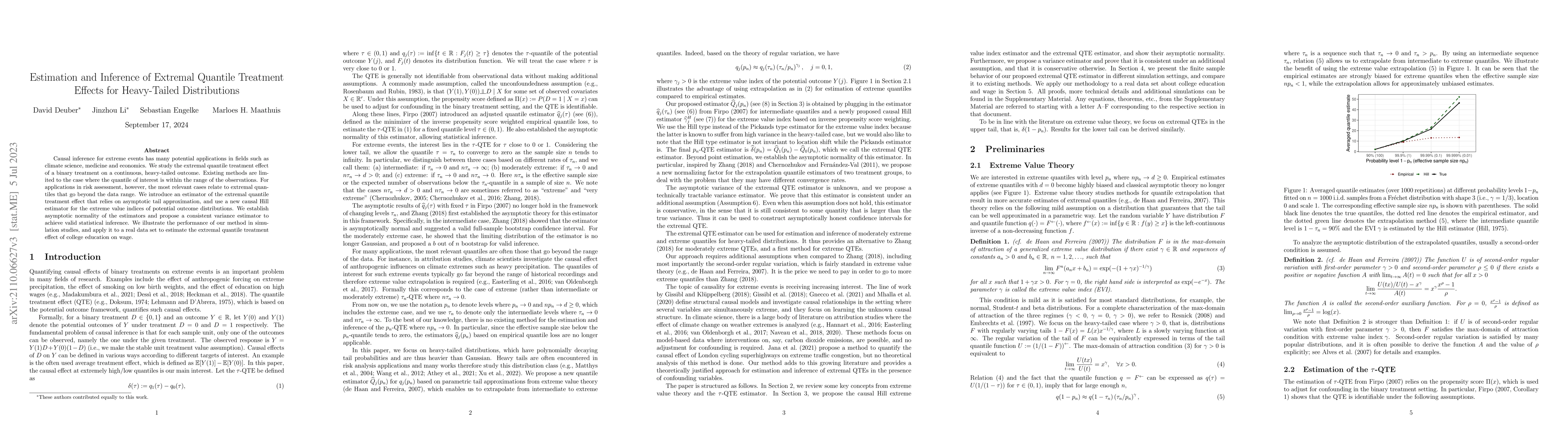

Causal inference for extreme events has many potential applications in fields such as climate science, medicine and economics. We study the extremal quantile treatment effect of a binary treatment o...

In this work, we provide robust bounds on the tail probabilities and the tail index of heavy-tailed distributions in the context of model misspecification. They are defined as the optimal value when...

Extreme quantile regression provides estimates of conditional quantiles outside the range of the data. Classical quantile regression performs poorly in such cases since data in the tail region are t...

Extremal graphical models are sparse statistical models for multivariate extreme events. The underlying graph encodes conditional independencies and enables a visual interpretation of the complex ex...

Multivariate extreme value theory is concerned with modeling the joint tail behavior of several random variables. Existing work mostly focuses on asymptotic dependence, where the probability of obse...

Extreme value statistics provides accurate estimates for the small occurrence probabilities of rare events. While theory and statistical tools for univariate extremes are well-developed, methods for...

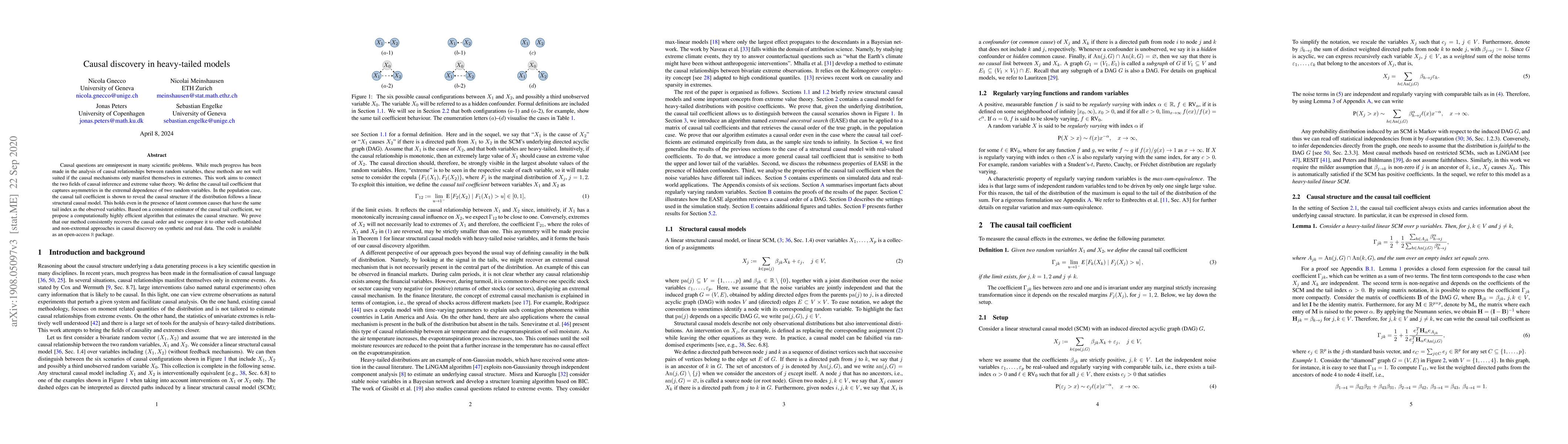

Causal questions are omnipresent in many scientific problems. While much progress has been made in the analysis of causal relationships between random variables, these methods are not well suited if...

Conditional independence, graphical models and sparsity are key notions for parsimonious statistical models and for understanding the structural relationships in the data. The theory of multivariate...

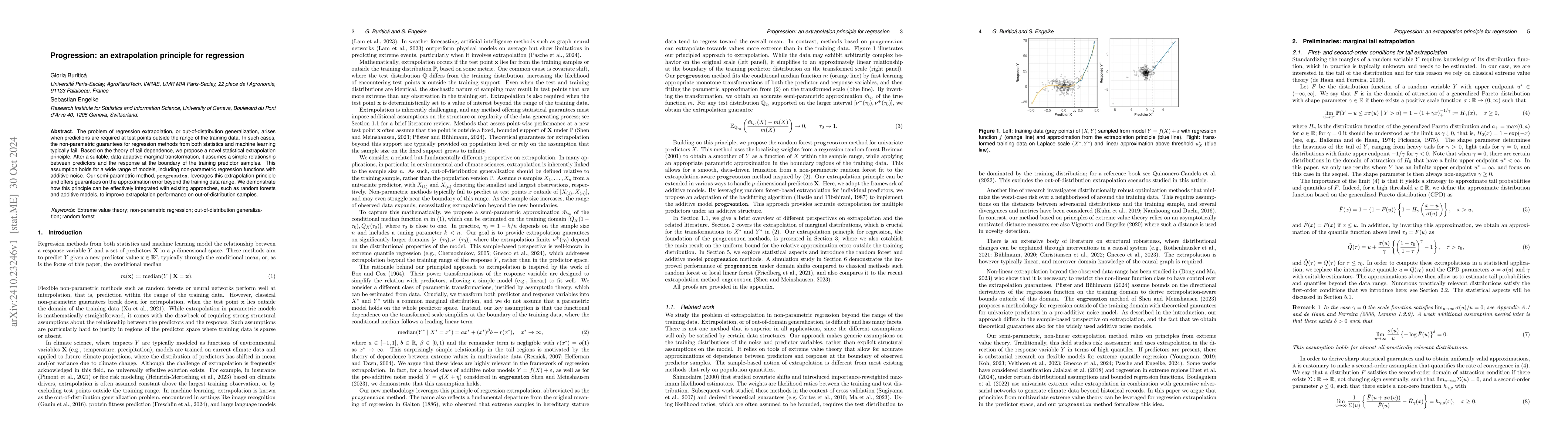

The problem of regression extrapolation, or out-of-distribution generalization, arises when predictions are required at test points outside the range of the training data. In such cases, the non-param...

Conditional independence and graphical models are crucial concepts for sparsity and statistical modeling in higher dimensions. For L\'evy processes, a widely applied class of stochastic processes, the...

The behavior of extreme observations is well-understood for time series or spatial data, but little is known if the data generating process is a structural causal model (SCM). We study the behavior of...

Conformal prediction is a popular method to construct prediction intervals for black-box machine learning models with marginal coverage guarantees. In applications with potentially high-impact events,...

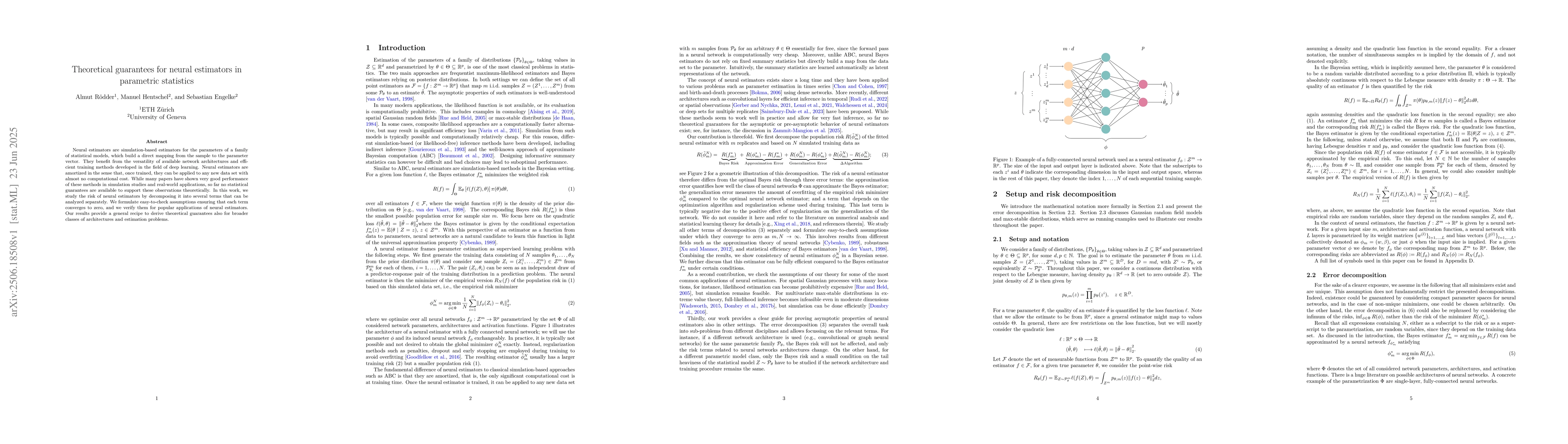

Neural estimators are simulation-based estimators for the parameters of a family of statistical models, which build a direct mapping from the sample to the parameter vector. They benefit from the vers...

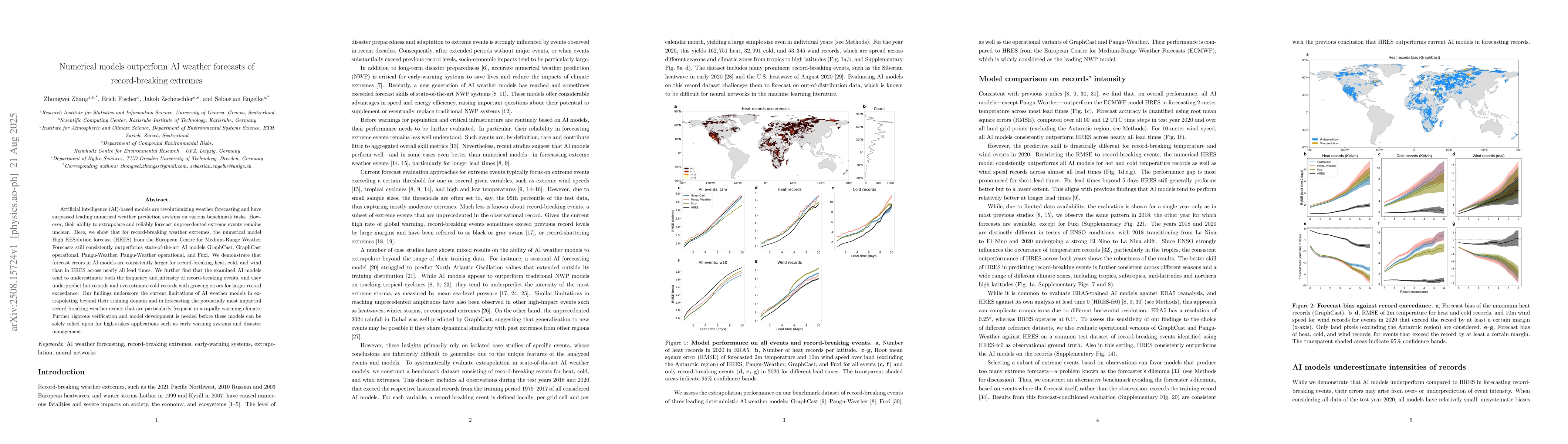

Artificial intelligence (AI)-based models are revolutionizing weather forecasting and have surpassed leading numerical weather prediction systems on various benchmark tasks. However, their ability to ...

Intrinsic Gaussian fields are used in many areas of statistics as models for spatial or spatio-temporal dependence, or as priors for latent variables. However, there are two major gaps in the literatu...

We introduce Ising-Hüsler-Reiss processes, a new class of multivariate Lévy processes that allows for sparse modeling of the path-wise conditional independence structure between marginal stable proces...

Testing whether two multivariate samples exhibit the same extremal behavior is an important problem in various fields including environmental and climate sciences. While several ad-hoc approaches exis...

Extreme value theory provides rigorous theory and statistical tools for extrapolation in machine learning, particularly in settings where traditional methods struggle due to data scarcity in the tails...

Multivariate generalized Pareto distributions arise as limits of threshold exceedances and form a central model class for multivariate extremes. Existing inference methods based on the extremal variog...