Causal inference for extreme events has many potential applications in fields

such as climate science, medicine and economics. We study the extremal quantile

treatment effect of a binary treatment on a continuous, heavy-tailed outcome.

Existing methods are limited to the case where the quantile of interest is

within the range of the observations. For applications in risk assessment,

however, the most relevant cases relate to extremal quantiles that go beyond

the data range. We introduce an estimator of the extremal quantile treatment

effect that relies on asymptotic tail approximation, and use a new causal Hill

estimator for the extreme value indices of potential outcome distributions. We

establish asymptotic normality of the estimators and propose a consistent

variance estimator to achieve valid statistical inference. We illustrate the

performance of our method in simulation studies, and apply it to a real data

set to estimate the extremal quantile treatment effect of college education on

wage.

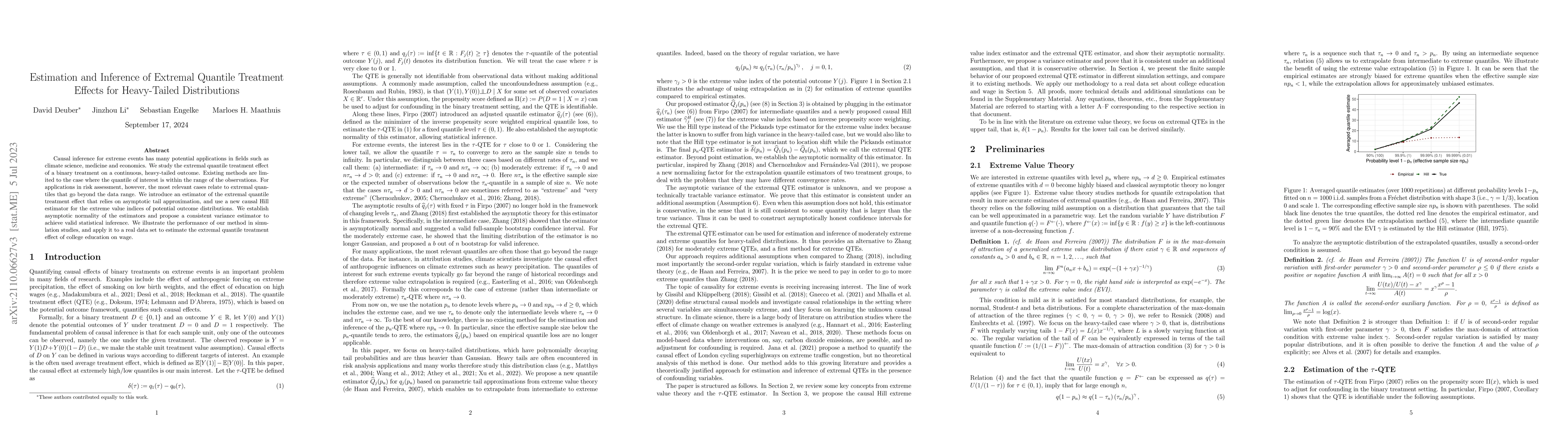

Discussion 0