Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider the problem of predicting the covariance of a zero mean Gaussian vector, based on another feature vector. We describe a covariance predictor that has the form of a generalized linear mod...

We consider the problem of forecasting multiple values of the future of a vector time series, using some past values. This problem, and related ones such as one-step-ahead prediction, have a very lo...

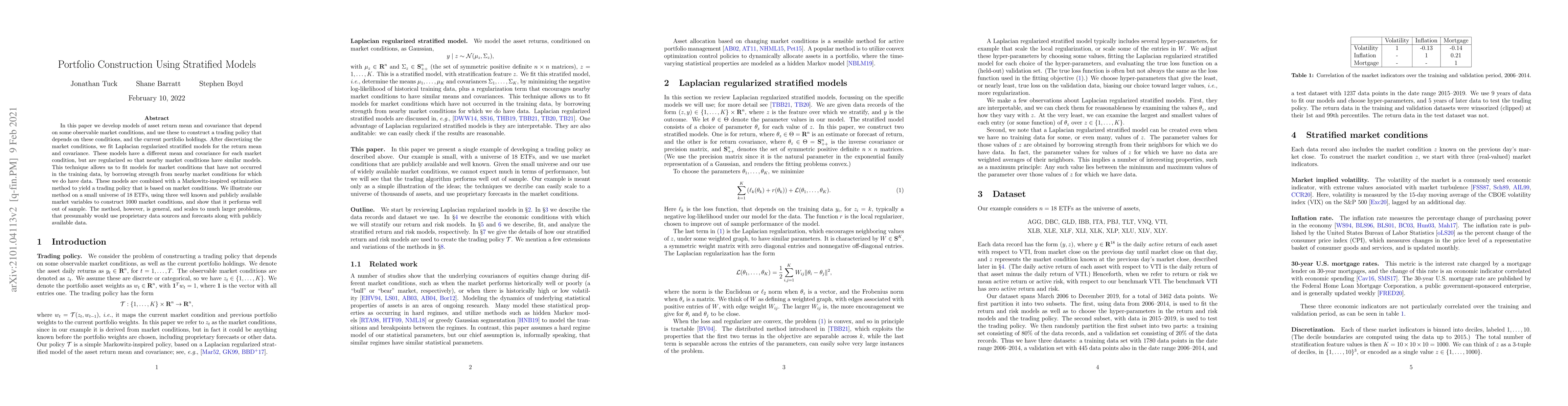

In this paper we develop models of asset return mean and covariance that depend on some observable market conditions, and use these to construct a trading policy that depends on these conditions, an...

A convex optimization model predicts an output from an input by solving a convex optimization problem. The class of convex optimization models is large, and includes as special cases many well-known...

We consider the problem of determining a sequence of payments among a set of entities that clear (if possible) the liabilities among them. We formulate this as an optimal control problem, which is c...

We consider the problem of assigning weights to a set of samples or data records, with the goal of achieving a representative weighting, which happens when certain sample averages of the data are cl...

We consider a collection of derivatives that depend on the price of an underlying asset at expiration or maturity. The absence of arbitrage is equivalent to the existence of a risk-neutral probabili...

Given an infeasible, unbounded, or pathological convex optimization problem, a natural question to ask is: what is the smallest change we can make to the problem's parameters such that the problem b...

We consider the problem of learning a linear control policy for a linear dynamical system, from demonstrations of an expert regulating the system. The standard approach to this problem is policy fit...

Many control policies used in various applications determine the input or action by solving a convex optimization problem that depends on the current state and some parameters. Common examples of su...

Recent work has shown how to embed differentiable optimization problems (that is, problems whose solutions can be backpropagated through) as layers within deep learning architectures. This method pr...

We consider the problem of minimizing a sum of clipped convex functions; applications include clipped empirical risk minimization and clipped control. While the problem of minimizing the sum of clip...

This paper considers the problem of fitting the parameters of a Kalman smoother to data. We formulate the Kalman smoothing problem with missing measurements as a constrained least squares problem an...

Stratified models are models that depend in an arbitrary way on a set of selected categorical features, and depend linearly on the other features. In a basic and traditional formulation a separate m...

We consider the problem of efficiently computing the derivative of the solution map of a convex cone program, when it exists. We do this by implicitly differentiating the residual map for its homoge...

In this paper, we provide conditions under which one can take derivatives of the solution to convex optimization problems with respect to problem data. These conditions are (roughly) that Slater's c...