Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we present an artificial neural network framework for portfolio compression of a large portfolio of European options with varying maturities (target portfolio) by a significantly smal...

This paper presents a Monte-Carlo-based artificial neural network framework for pricing Bermudan options, offering several notable advantages. These advantages encompass the efficient static hedging...

An extension of the Hawkes process, the Marked Hawkes process distinguishes itself by featuring variable jump size across each event, in contrast to the constant jump size observed in a Hawkes proce...

We consider the hedging of European options when the price of the underlying asset follows a single-factor Markovian framework. By working in such a setting, Carr and Wu \cite{carr2014static} derive...

In this paper, we perform a comprehensive study of different covariance and precision matrix estimation methods in the context of minimum variance portfolio allocation. The set of models studied by ...

This paper introduces the Neural Network for Nonlinear Hawkes processes (NNNH), a non-parametric method based on neural networks to fit nonlinear Hawkes processes. Our method is suitable for analyzi...

This paper presents a data-driven interpretable machine learning algorithm for semi-static hedging of Exchange Traded options, considering transaction costs with efficient run-time. Further, we prov...

We present a semi-static hedging algorithm for callable interest rate derivatives under an affine, multi-factor term-structure model. With a traditional dynamic hedge, the replication portfolio need...

In this paper, we present a computationally efficient technique based on the \emph{Method of Lines} (MOL) for the approximation of the Bermudan option values via the associated partial differential ...

Multi-dimensional Hawkes process (MHP) is a class of self and mutually exciting point processes that find wide range of applications -- from prediction of earthquakes to modelling of order books in ...

We present here a regress later based Monte Carlo approach that uses neural networks for pricing high-dimensional contingent claims. The choice of specific architecture of the neural networks used i...

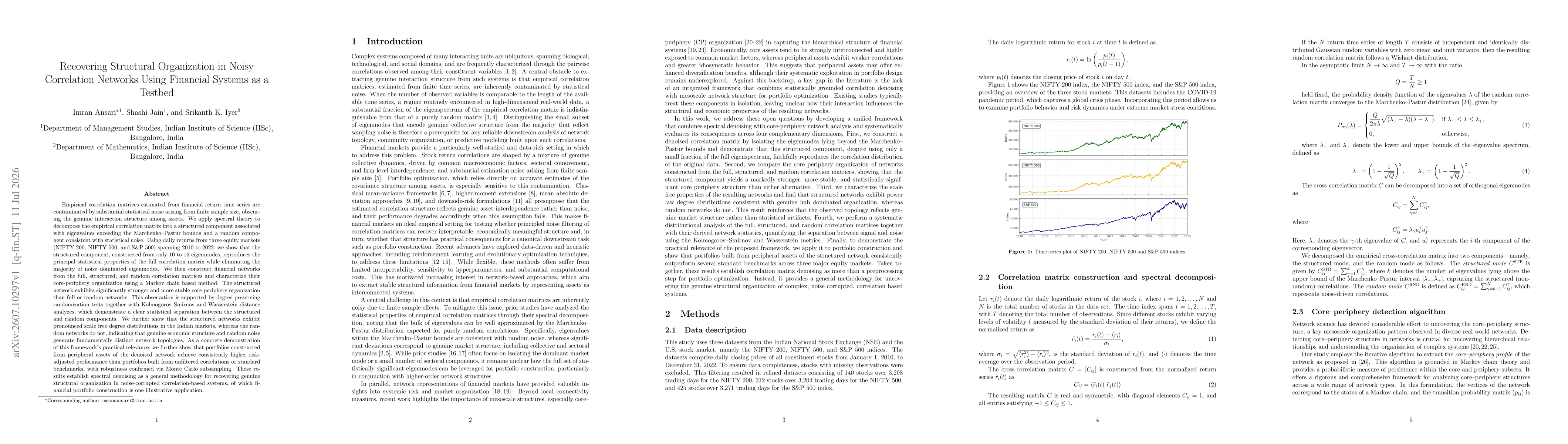

Market information events are generated intermittently and disseminated at high speeds in real-time. Market participants consume this high-frequency data to build limit order books, representing the c...

Quoting algorithms are fundamental to electronic trading systems, enabling participants to post limit orders in a systematic and adaptive manner. In multi-asset or multi-contract settings, selecting t...

With the advent of electronic capital markets and algorithmic trading agents, the number of events in tick-by-tick market data has exploded. A large fraction of these orders is transient. Their epheme...

We consider an investor who wants to hedge a path-dependent option with maturity $T$ using a static hedging portfolio using cash, the underlying, and vanilla put/call options on the same underlying wi...

Empirical correlation matrices estimated from financial return time series are contaminated by statistical noise arising from finite sample size, obscuring genuine interactions among assets. We apply ...