Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider the Fourier-Laplace transforms of a broad class of polynomial Ornstein-Uhlenbeck (OU) volatility models, including the well-known Stein-Stein, Sch\"obel-Zhu, one-factor Bergomi, and the ...

An extensive empirical study of the class of Volterra Bergomi models using SPX options data between 2011 and 2022 reveals the following fact-check on two fundamental claims echoed in the rough volat...

The quintic Ornstein-Uhlenbeck volatility model is a stochastic volatility model where the volatility process is a polynomial function of degree five of a single Ornstein-Uhlenbeck process with fast...

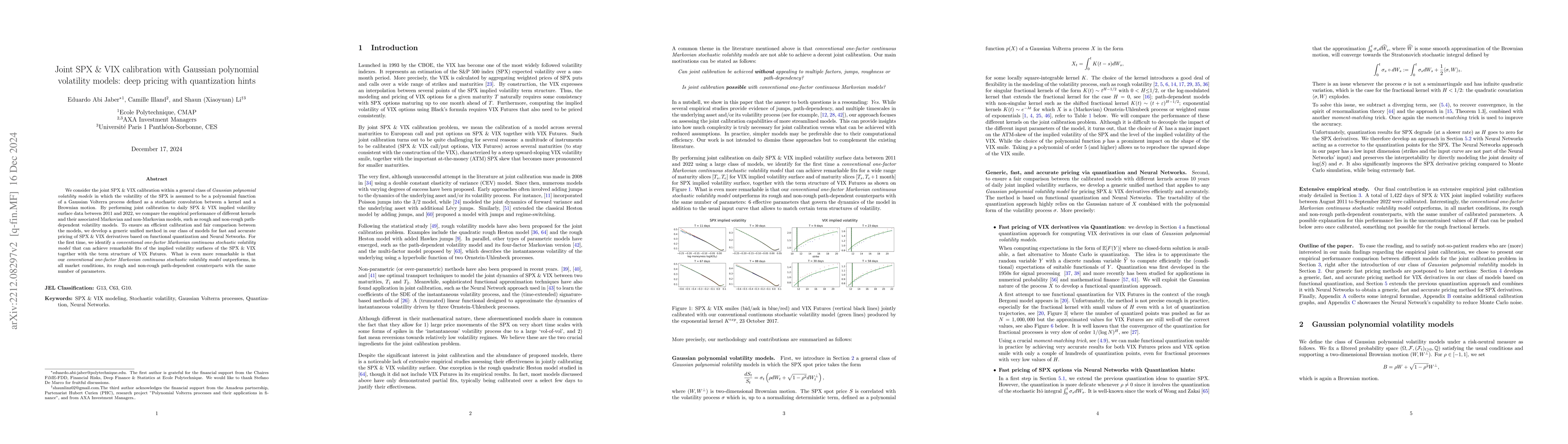

We consider the joint SPX-VIX calibration within a general class of Gaussian polynomial volatility models in which the volatility of the SPX is assumed to be a polynomial function of a Gaussian Volt...