Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we develop two families of sequential monitoring procedure to (timely) detect changes in a GARCH(1,1) model. Whilst our methodologies can be applied for the general analysis of change...

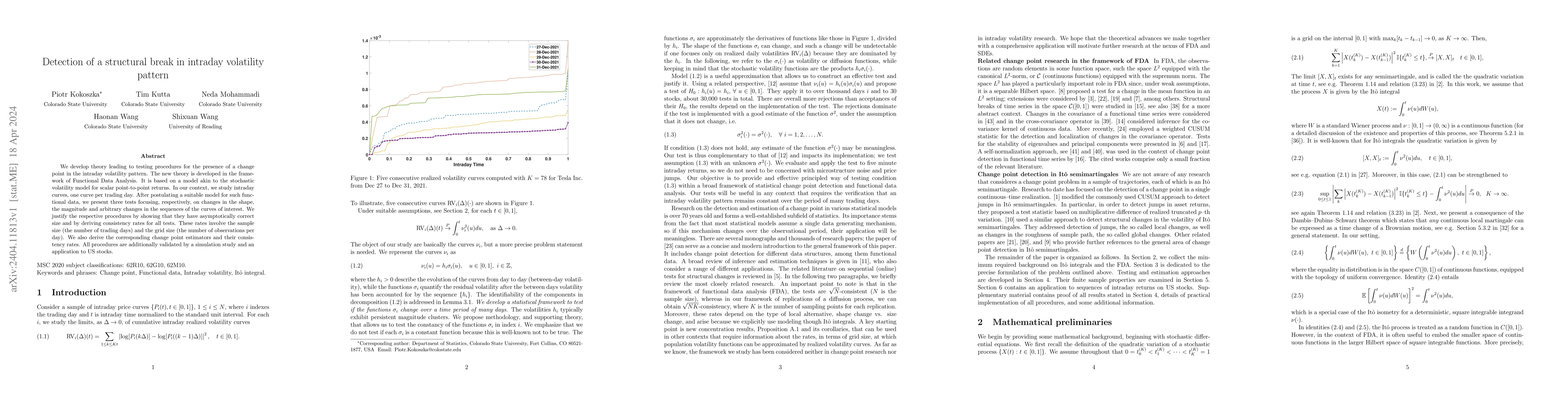

We develop theory leading to testing procedures for the presence of a change point in the intraday volatility pattern. The new theory is developed in the framework of Functional Data Analysis. It is...

We propose a stochastic volatility model for time series of curves. It is motivated by dynamics of intraday price curves that exhibit both between days dependence and intraday price evolution. The c...

This paper studies the seminormal bases $\{f_{\mathfrak{s}\mathfrak{t}}\}$ and the dual seminormal bases $\{g_{\mathfrak{s}\mathfrak{t}}\}$ of the non-degenerate and the degenerate cyclotomic Hecke ...

The cyclotomic Hecke algebra $H_{r,p,n}$ of type $G(r,p,n)$ (where $r=pd$) can be realized as the $\sigma$-fixed point subalgebra of certain cyclotomic Hecke algebra $H_{r,n}$ of type $G(r,1,n)$ with ...

Incorporating historical or real-world data into analyses of treatment effects for rare diseases has become increasingly popular. A major challenge, however, lies in determining the appropriate degree...

We study the problem of detecting and localizing multiple changes in the mean parameter of a Banach space-valued time series. The goal is to construct a collection of narrow confidence intervals, each...