Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we will present a new flexible distribution for three-dimensional angular data, or data on the three-dimensional torus. Our trivariate wrapped Cauchy copula has the following benefits...

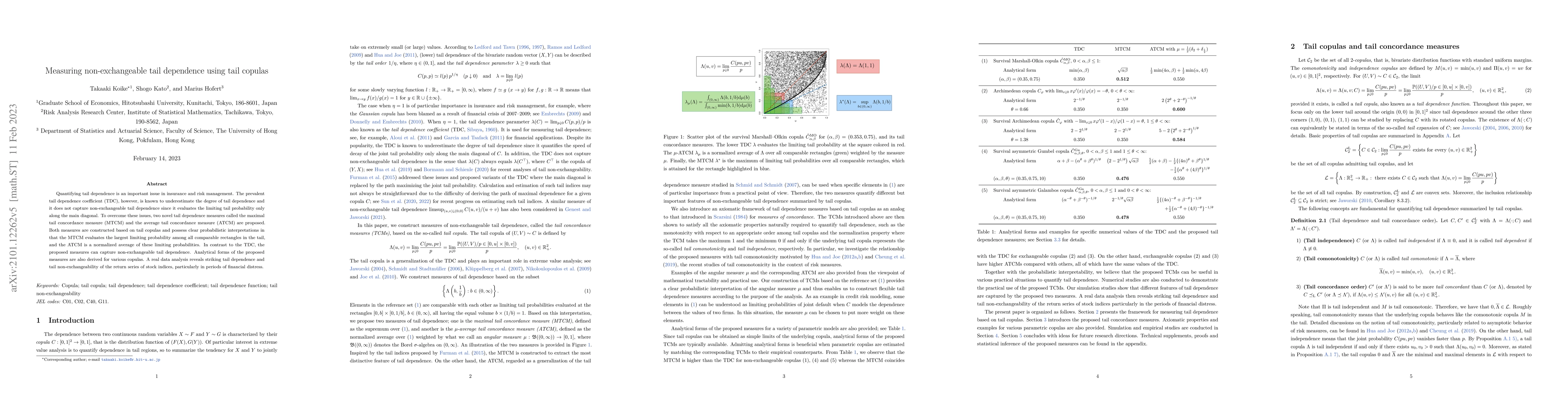

Quantifying tail dependence is an important issue in insurance and risk management. The prevalent tail dependence coefficient (TDC), however, is known to underestimate the degree of tail dependence ...

We propose a copula-based measure of asymmetry between the lower and upper tail probabilities of bivariate distributions. The proposed measure has a simple form and possesses some desirable properti...

In meta-analysis, the random-effects models are standard tools to address between-study heterogeneity in evidence synthesis analyses. For the random-effects distribution models, the normal distribut...

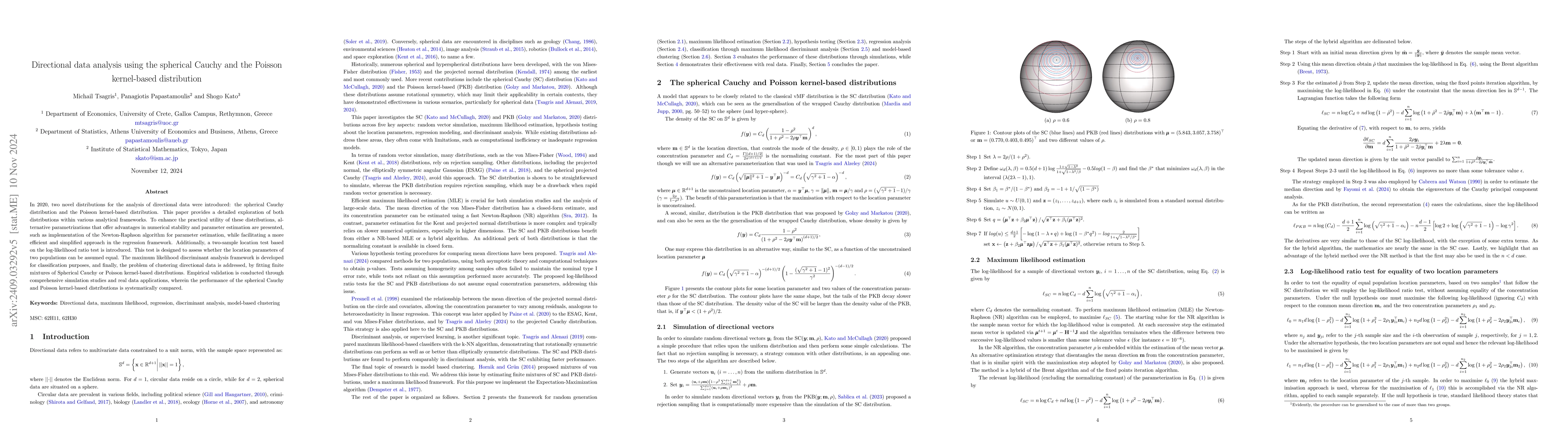

In 2020, two novel distributions for the analysis of directional data were introduced: the spherical Cauchy distribution and the Poisson kernel-based distribution. This paper provides a detailed explo...

We call two copulas tail equivalent if their first-order approximations in the tail coincide. As a special case, a copula is called tail symmetric if it is tail equivalent to the associated survival c...

This paper introduces a robust estimation framework based solely on the copula function. We begin by introducing a family of divergence measures tailored for copulas, including the \(\alpha\)-, \(\bet...

This paper introduces two families of probability distributions for Bayesian analysis of hypertoroidal data. The first family consists of symmetric distributions derived from the projection of multiva...

We propose a regression model in which the responses are spherical variables and the covariates include linear and/or spherical variables. A novel link function is introduced by extending the M\"obius...

In this paper, we propose a new flexible family of distributions for data that consist of three angles, two angles and one linear component, or one angle and two linear components. To achieve this, we...

In biomedical studies, paired survival data arise naturally when two event times are observed within the same subject. Existing statistical models seldom accommodate both cure fractions and complex de...