Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper mainly investigates the strong convergence and stability of the truncated Euler-Maruyama (EM) method for stochastic differential delay equations with variable delay whose coefficients can...

In this paper, we consider the generalized Ait-Sahaliz interest rate model with Poisson jumps in finance. The analytical properties including the positivity, boundedness and pathwise asymptotic esti...

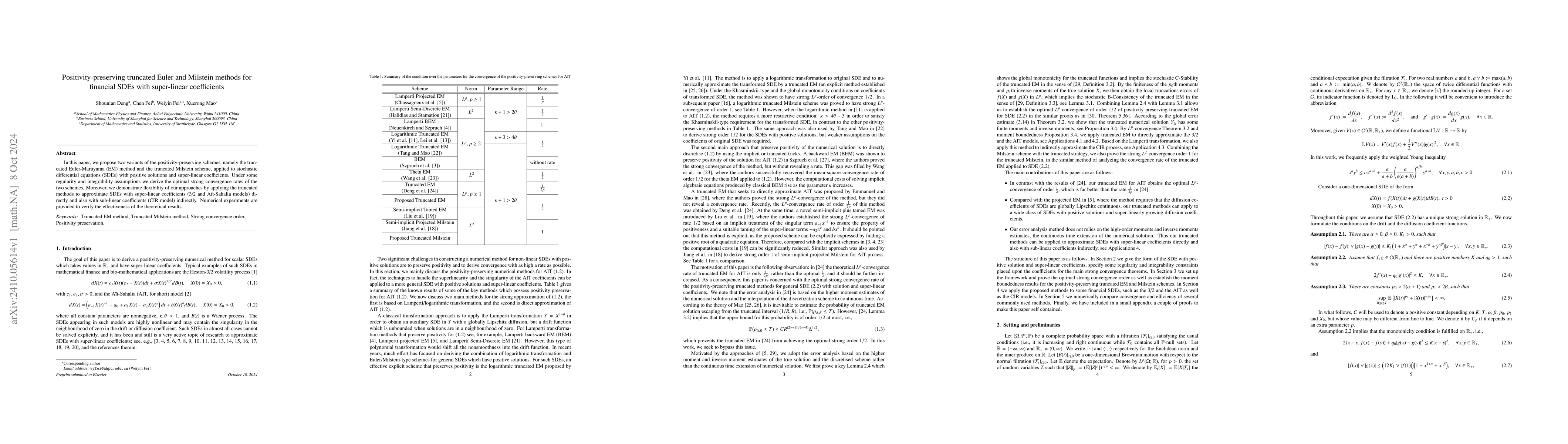

In this paper, we propose two variants of the positivity-preserving schemes, namely the truncated Euler-Maruyama (EM) method and the truncated Milstein scheme, applied to stochastic differential equat...

Most existing literature focuses on pointwise convergence (i.e., convergence at a fixed time point) of numerical solutions for Stochastic functional differential equations (SFDEs). In contrast, this p...